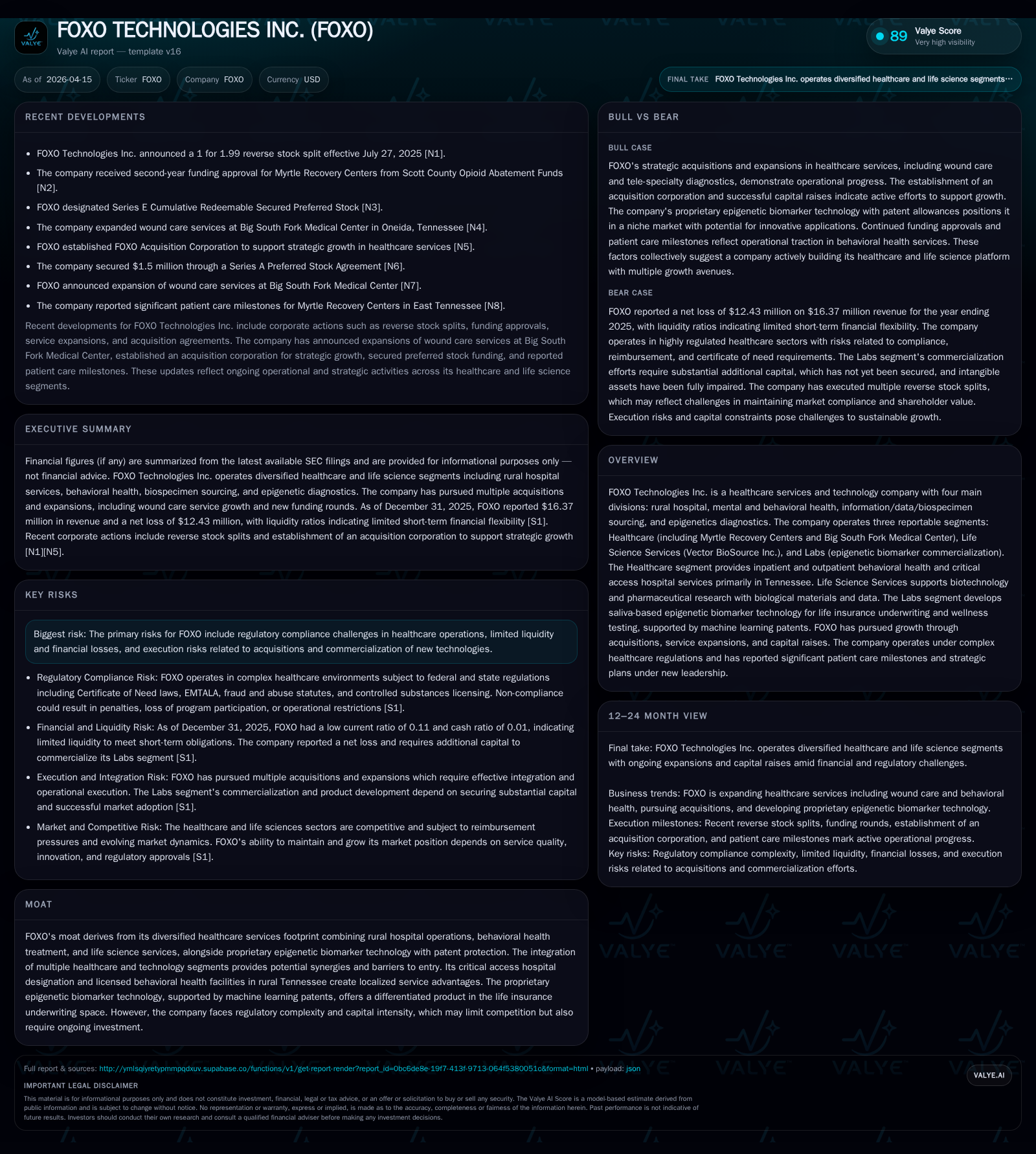

FOXO Technologies’ Diversified Healthcare Model Faces Capital Constraints Amid Regulatory Complexities

FOXO operates across rural hospital services, behavioral health, life science sourcing, and epigenetic diagnostics, with rapid revenue growth overshadowed by continued losses and liquidity challenges.

FOXO Technologies Inc. has grown through acquisitions to build a diversified healthcare and technology platform encompassing rural hospitals, behavioral health, biospecimen sourcing, and epigenetic diagnostics. The company’s revenue surged in 2025 following key acquisitions but persistent operating losses, negative cash flows, and tight liquidity raise concerns about its near-term financial viability. Regulatory compliance risks and integration challenges add complexity to its business model. FOXO’s future hinges on resolving capital structure issues, executing integration plans effectively, and advancing commercialization of its epigenetic testing technologies.

Company Overview

FOXO Technologies Inc. operates a diversified healthcare services and technology platform comprising four synergistic divisions: a rural hospital division operating Big South Fork Medical Center; a mental and behavioral health division including Myrtle Recovery Centers; an information, data and biospecimen sourcing division through Vector BioSource; and an epigenetics diagnostics division focused on saliva-based biomarker testing enhanced by machine learning patents [S1], [S11].

Originally formed as Delwinds Insurance Acquisition Corp., FOXO transformed via acquisitions: Myrtle Recovery Centers in June 2024, Rennova Community Health including Scott County Community Health in September 2024, and Vector BioSource in September 2025 [S1], [S11]. These acquisitions expanded FOXO’s footprint across healthcare delivery in underserved Tennessee regions alongside life science research services.

Historical Growth and Financial Performance

FOXO's financials reflect rapid top-line growth primarily from acquisitions but persistent unprofitability:

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 16 | -12 | -4 | -10 | +304.0% | -0.2% |

| 2024 | 4 | -12 | -3 | -8 | +2694.2% | +53.1% |

| 2023 | 0 | -26 | -7 | -22 | -71.6% | +72.2% |

| 2022 | 1 | -95 | -24 | -40 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -4 | -111.5 |

| 2024 | -233.0 | |

| 2023 | -7 | 187.6 |

| 2022 | -24 | -1420.0 |

Source: SEC companyfacts cache [F1].

Revenues rose approximately fourfold from $4.05 million in FY2024 to $16.37 million in FY2025 due to full-year contributions from prior acquisitions and the addition of Vector BioSource [F1]. Despite this growth in scale, operating losses remain elevated though reduced from prior years' extremes—from nearly $40 million loss in FY2022 to just over $10 million loss in FY2025—reflecting ongoing investment costs related to expansion and integration [F1].

Net losses have remained stable around $12 million for the last two years despite revenue increases indicating persistent operational challenges or one-time expenses [F1]. Operating cash flows were negative $3.9 million in FY2025 with minimal capital expenditures (~$62K), underscoring limited reinvestment capacity [F1].

Year-end liquidity was critically constrained with cash of only $207K against current liabilities approaching $28.7 million yielding a precarious current ratio of approximately 0.11 [F1]. The company acknowledges insufficient resources beyond December 2026 without additional financing [S5], [S10].

Business Segments

Healthcare: This segment includes Myrtle Recovery Centers offering inpatient/outpatient behavioral health treatments focused on substance use disorders along with Big South Fork Medical Center—a critical access hospital providing emergency care plus ancillary lab and diagnostic services. Recent expansions include tele-specialty services and cardiac diagnostics launched early 2026 aimed at rural Tennessee populations [S1], [S11].

Life Science Services: Operated through Vector BioSource since September 2025 acquisition; it provides biological specimen sourcing globally for biotechnology and pharmaceutical clients requiring specialized logistics for tissues and biofluids [S21].

Labs: Focuses on commercializing saliva-based epigenetic biomarker tests utilizing proprietary machine learning algorithms for wellness assessments and life insurance underwriting applications. The company holds multiple patents supporting these technologies that differentiate its offerings [S21], [S25].

Regulatory Environment

FOXO faces extensive regulatory risks common to healthcare providers compounded by its diverse operations:

- Compliance with Medicare/Medicaid billing rules alongside heightened enforcement under the False Claims Act creates exposure to civil penalties including qui tam lawsuits alleging improper claims submission [S4], [S18].

- HIPAA/HITECH regulations impose stringent data privacy standards on patient health data handled across clinical and digital platforms; violations could result in significant fines and reputational harm [S6], [S7], [S17].

- Clinical lab operations are subject to CLIA certification requirements; failure may disrupt epigenetic testing services impacting revenue streams from Labs segment [S19].

- Hospital operations under critical access designation face complex state-level regulations impacting reimbursement rates vital for financial performance.

- Ongoing healthcare reform efforts could further constrain reimbursement levels affecting profitability given government payers represent a significant portion of revenues [S9], [S12], [S13].

These overlapping regulatory factors require continued investment in compliance infrastructure amidst narrow operating margins.

Capital Structure & Liquidity Challenges

FOXO's financial condition remains fragile:

- The independent auditor issued a going concern explanatory paragraph citing sustained operating losses combined with limited liquidity raising doubts about the company's ability to continue without additional funding [S5], [S10], [S16].

- Cash resources are insufficient to cover operations beyond late 2026 absent successful new capital raises or improved cash flow generation.

- Access to existing equity lines of credit has been impeded due to low stock price levels and limited trading volume restricting drawdowns under agreements like the Strata Purchase Agreement [S10], [S16].

- Efforts to execute reverse stock splits aimed at improving share price metrics have faced regulatory hurdles linked partly to ownership concentration; a pending FINRA appeal is scheduled with material implications for capital structure flexibility [S8], [S26].

- Majority ownership by Rennova Health Inc. centralizes control but limits minority shareholder influence potentially affecting governance dynamics.

Growth Outlook & Key Milestones

Growth prospects depend on several factors:

- Expansion within Healthcare segment via outpatient service growth at Myrtle Recovery Centers plus telehealth initiatives at Big South Fork Medical Center may enhance revenue stability.

- Life Science Services could benefit from increasing demand for quality biospecimens supporting biotech research pipelines.

- Labs segment commercialization progress of epigenetic biomarker tests presents transformative potential if adoption grows among insurers and wellness markets.

- Successful integration of recent acquisitions remains critical given noted risks around management distraction and synergy capture.

- Resolution of regulatory approvals or reimbursement policies affecting genetic/epigenetic testing could materially influence revenue trends.

- Outcome of FINRA appeal related to reverse stock split will impact strategic options for capital raising vital for operational sustainability.

No formal external guidance was provided; monitoring quarterly operational updates alongside capital market developments is recommended.

Capital Allocation & Returns Profile

Financial returns metrics reflect developmental stage operations:

- Approximate return on equity stands near negative -111%, reflecting significant accumulated net losses relative to shareholder equity invested as of end-2025 ([F1]).

- Free cash flow remains negative near $3.9 million indicating ongoing operational outflows exceeding modest capex primarily related to sustaining current assets ([F1]).

- No dividends or share repurchases have been declared or indicated consistent with preservation-focused capital allocation amid liquidity constraints ([S8]).

- Management faces pressure to optimize working capital while balancing debt servicing obligations given sizeable current liabilities ([F1], [S23]).

Conclusion

FOXO Technologies combines traditional rural healthcare delivery with advanced epigenetic biomarker development aiming at differentiated market niches such as life insurance underwriting. While acquisitions have driven rapid revenue growth over the last two years,[F1] profitability remains elusive amid substantial operating losses.[F1] Liquidity constraints are acute with limited cash reserves against high current liabilities posing material short-term solvency concerns.[F1],[S5],[S10]

The company navigates complex regulatory landscapes spanning healthcare billing compliance,[S4],[S18] data privacy,[S6],[S7] lab certifications,[S19] and reimbursement pressures.[S9],[S12] Governance is tightly held by majority shareholder Rennova Health Inc., which may impact minority investor dynamics.[S1]

Upcoming catalysts include integration success of acquired businesses,[N/A] commercialization progress of Labs segment products,[N/A] resolution of regulatory uncertainties,[N/A] and crucially the FINRA appeal decision on the reverse stock split that may unlock much-needed capital flexibility.[S8]

Investors should closely monitor quarterly disclosures focusing on operational margin improvements alongside updates on capital markets access given their pivotal role in sustaining FOXO’s growth trajectory amid challenging financial conditions.

This analysis relies exclusively on publicly available SEC filings through April 15th, 2026 without forward-looking estimates or investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments