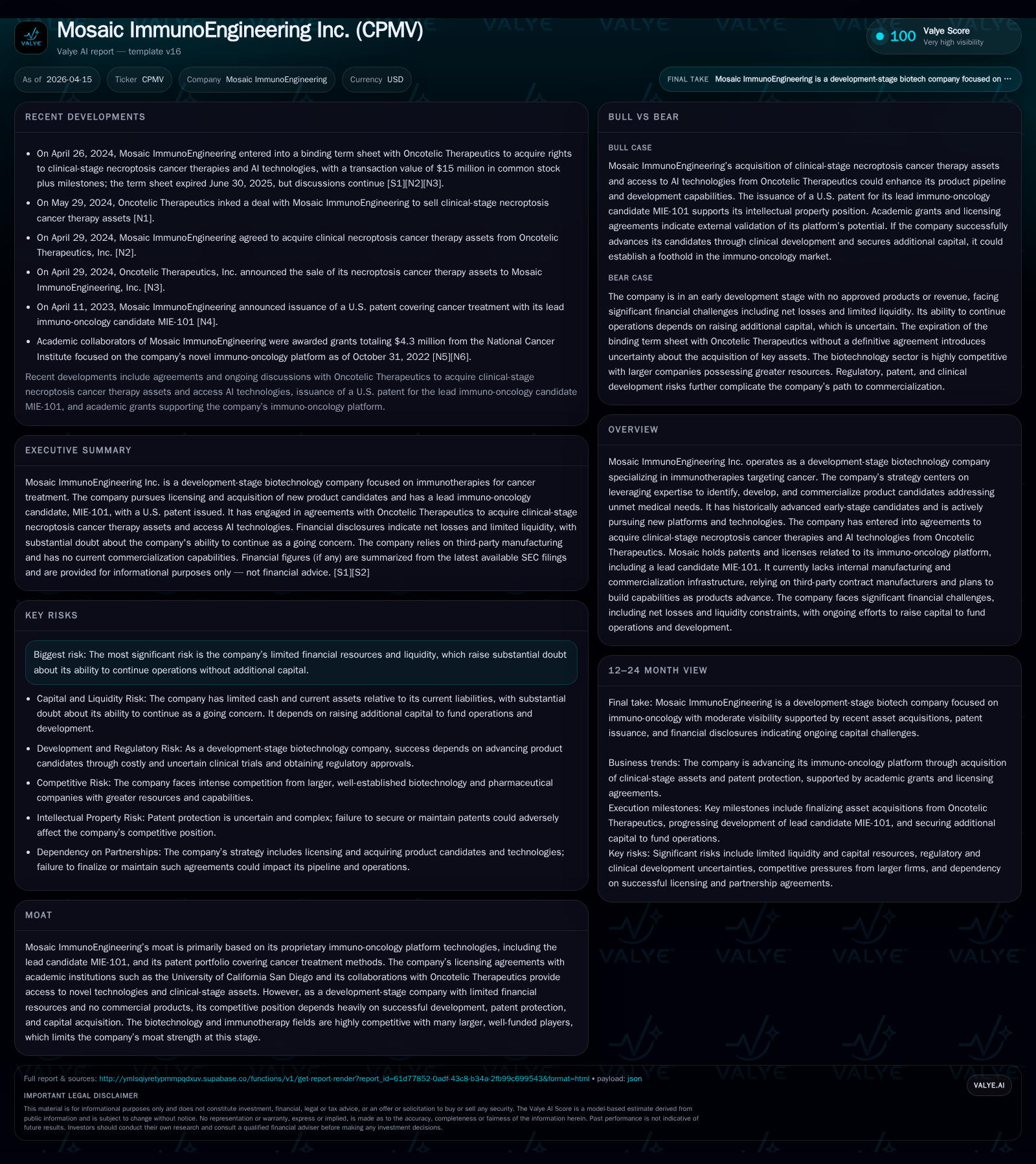

Mosaic ImmunoEngineering’s Strategic Shift: Building Immunotherapy Pipeline Under Capital Pressure

Development-stage biotech Mosaic ImmunoEngineering balances innovative immunotherapy acquisitions with acute funding challenges.

Mosaic ImmunoEngineering Inc. has advanced since its 2020 inception by leveraging proprietary CPMV-based immunotherapy technology and key reverse merger-driven structural changes. The company entered a binding term sheet to acquire clinical necroptosis therapies and AI tools from Oncotelic Therapeutics, aiming to diversify its pipeline amidst ongoing liquidity constraints. Persistent annual losses and a current ratio near zero highlight substantial financial strain, necessitating urgent capital raises to sustain R&D and operational viability. Success depends on executing acquisitions, expanding patent protections, and achieving regulatory milestones while navigating an extremely tight cash runway.

From Formation to Platform: Historical Growth and Key Development Milestones

Mosaic ImmunoEngineering originated as Private Mosaic in early 2020, focusing on the cowpea mosaic virus (CPMV) platform exclusively licensed from Case Western Reserve University (CWRU) by mid-2020 [S1]. This platform forms the basis of the company's lead therapeutic candidate targeting immuno-oncology indications. A critical corporate restructuring occurred via a reverse merger closed August 21, 2020, whereby Patriot Scientific acquired Private Mosaic's assets. Post-merger, Private Mosaic stockholders controlled approximately 90% of the combined entity on an as-converted basis. The transaction involved issuance of Series A and Series B convertible preferred stocks convertible into common shares with anti-dilution rights [S1].

Despite these foundational steps, Mosaic remains a development-stage biotech without commercialized therapeutics or revenues. Operating losses have persisted but demonstrated moderate improvement: operating income losses narrowed from -$2.63 million in FY2022 to -$616 thousand in FY2025, representing roughly a 30% year-over-year improvement between FY2024 and FY2025 [F1]. Net income deficits also declined by approximately 25.4% in FY2025 compared to FY2024, settling at -$688 thousand [F1]. These financial trends reflect scaled-back development consistent with constrained resources.

Historical performance (annual)

| FY | Net ($mm) | CFO ($) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -1 | -111397 | -1 | +25.4% |

| 2024 | -1 | -241159 | -1 | +8.6% |

| 2023 | -1 | -497467 | -1 | +57.7% |

| 2022 | -2 | -690129 | -3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 9.2 |

| 2024 | 13.6 |

| 2023 | 17.2 |

| 2022 | 48.7 |

Source: SEC companyfacts cache [F1].

Operating losses have moderated significantly but remain substantial.

Expanding the Pipeline: Acquisition Plans and New Technology Integration

On April 26, 2024, Mosaic entered into a binding term sheet with Oncotelic Therapeutics to acquire rights to clinical-stage necroptosis cancer therapies associated with vascular disruptive agents (VDAs). VDAs represent therapeutic approaches targeting tumor vasculature integrity to enhance immune-mediated tumor eradication—a novel mechanism within immuno-oncology. The acquisition also includes non-exclusive access to Oncotelic's proprietary Artificial Intelligence platforms for identifying synergistic immunotherapy combinations [S1][S2].

Financial terms included initial consideration valued at $15 million in common stock or a negotiated combination of stock classes upon definitive agreement execution. Additional milestone equity issuances up to $15 million are contingent on developmental progress. Although the Binding Term Sheet expired June 30, 2025, discussions continue toward definitive agreements and shareholder approval amid complex financing conditions requiring waivers from Convertible Note holders representing over 90% of principal outstanding due to transaction-triggered payment obligations [S1][S2][S22].

This strategic move signals Mosaic’s intent to diversify beyond the CPMV platform by integrating external innovation alongside internal expertise.

Capital Constraints and Liquidity Risk: Financial Health Overview

Liquidity metrics reveal acute financial stress threatening the company's operational viability. As of December 31, 2025, cash and cash equivalents stood at approximately $3,600 against current liabilities exceeding $6 million—yielding a current ratio effectively near zero [F1], indicating inability to cover short-term obligations.

The balance sheet is further burdened by multiple unsecured convertible promissory notes. Notably, a $200 thousand note issued November 18, 2024 bears interest at 5% per annum payable upon closing of a financing exceeding $10 million or convertible into common stock at investor discretion [S4][S5][S18]. Additionally, a $70 thousand loan from Oncotelic carried a steep interest rate of 16%, fully repaid by December 12, 2024 alongside accrued interest [S4][S18]. Annual interest expense related to these debts approximates $80 thousand reflecting meaningful cost burdens though largely non-cash in nature [S5][S6][S20].

Stretched accounts payable combined with minimal cash reserves limit capacity for essential R&D investment needed for pipeline advancement. Management discloses substantial doubt about continuing as a going concern absent immediate capital infusion through equity or debt financings—both challenged by market conditions for small-cap biotechs lacking commercial products [S7][S8][S13]. Consequently, the company faces difficult trade-offs between survival funding and meaningful product development.

Outlook: Growth Prospects and Regulatory Challenges

Future growth depends heavily on consummating acquisition deals like Oncotelic’s assets and successfully licensing or internally developing new candidates beyond the CPMV platform. No marketed products mean all growth hinges on R&D milestones progressing through preclinical validation into clinical trials subject to FDA biologics license regulations under the Public Health Service Act and analogous foreign requirements [S3][S15][S16].

Clinical development challenges include stringent manufacturing controls necessary for biologics—heat sensitivity and microbial contamination risks require sterile processes—and lengthy regulatory timelines coupled with uncertain patent outcomes amid evolving global intellectual property landscapes [S3][S17]. Competitive pressures intensify as larger pharmaceutical companies dominate immuno-oncology markets with established checkpoint inhibitors and T-cell engager therapies limiting entry for novel modalities like necroptosis agents or CPMV-derived constructs [S15].

Capital raising is critical; however dilution risks are significant given existing debt structures with conversion triggers potentially accelerating dilution upon equity raises or business combinations [S4][S8][S13]. Shareholder consents required due to outstanding Convertible Notes complicate transaction execution risk further [S22][S25].

Manufacturing Strategy: Outsourcing with Future Internalization Plans

Currently lacking internal manufacturing infrastructure typical for biologics production requiring GMP-certified cleanroom facilities capable of sterile processing—Mosaic relies heavily on contract development and manufacturing organizations (CDMOs) for clinical material supply chains [S3]. This approach provides flexibility during early-phase trials but carries risks around quality consistency and scale-up complexities needed for pivotal studies or commercialization.

The plan anticipates gradual internal capability development contingent on capital availability allowing tighter control over manufacturing critical parameters unique to biologics’ sensitivity distinct from small molecule drugs. Such hybrid models balancing outsourcing with selective internal buildout represent standard cost-risk mitigation among emerging biotechs managing limited resources [S3].

Capital Allocation: Cash Flows and Financial Returns

Reflecting its developmental status without revenue streams or commercial products yet realized, Mosaic has consistently consumed cash from operations although outflows have lessened—from nearly $700K annually circa FY2022 down to about $111K in FY2025—indicating improving cash flow trends despite continued negative free cash flow given negligible capital expenditures recorded during this period [F1][S7][S20].

Approximate return on equity remains negative considering cumulative net losses outweighing equity contributions; shareholder equity stood near negative $7.48 million as of FY2025-end reflecting ongoing dilution effects absent revenue generation or asset monetization events [F1].

Capital deployment focuses primarily on payroll including scientific staff supporting platform advancement alongside general corporate expenses such as audit fees and patent prosecution costs protecting intellectual property central to the CPMV platform exclusivity plus AI-driven discovery rights acquired from Oncotelic [F1][S4][S18][S21].

Debt facilities incorporating conversion triggers imply potential dilution escalation after equity raises or transactions imposing operational constraints requiring careful financial management.

This overview synthesizes Mosaic ImmunoEngineering’s innovative strengths anchored in proprietary immunotherapy platforms alongside persistent financial fragility characteristic of early-stage biotechs lacking near-term revenues. Success critically depends on securing capital sufficient for licensing integration while managing significant liquidity risks that currently cast doubt on ongoing viability absent fresh funding sources. Investors should weigh these uncertainties carefully.

Disclaimer: This report references publicly available filings as of April 15, 2026. It does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments