Brown & Brown's Strategic Network and Healthcare Push Amid Evolving Brokerage Dynamics

Analyzing how Brown & Brown's acquisition-fueled growth and National Healthcare Practice position it within insurance brokerage challenges in 2026.

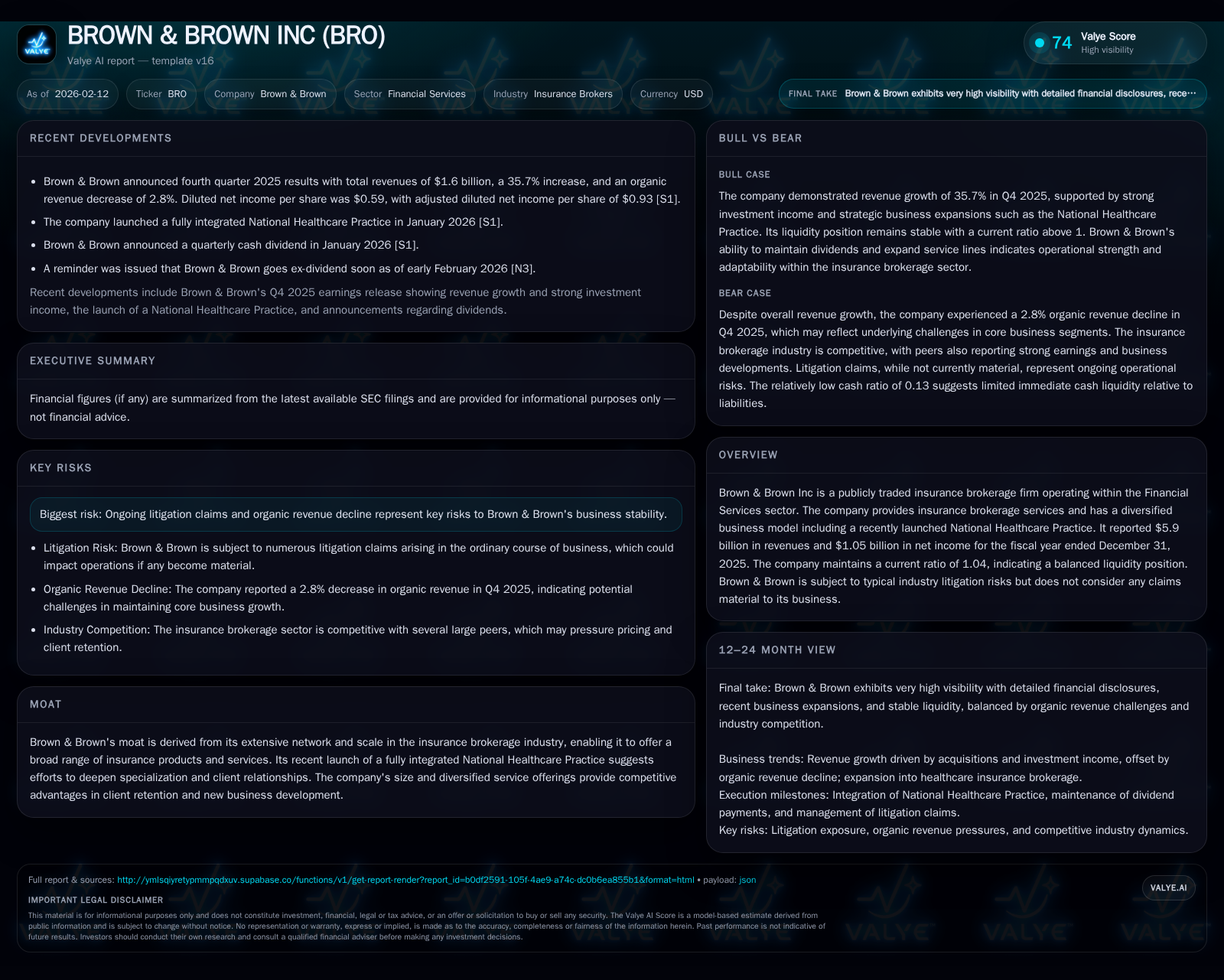

Brown & Brown Inc. recorded $5.9 billion in revenue for 2025, driven largely by acquisitions despite a slight organic revenue decline, underscoring the tension between growth sustainability and operational efficiency. Its expansive brokerage network and newly launched National Healthcare Practice deepen its competitive moat, enhancing client specialization in a competitive market. Litigation risks, typical in the industry, remain contained, while investment income has recently provided an unexpected boost to earnings. Going forward, balancing acquisition-driven growth with organic performance and navigating peer competition will be critical.

A Closer Look at Brown & Brown’s Financial Pulse

Brown & Brown Inc.’s fiscal year ended December 31, 2025, showcased notable scale with revenues reaching $5.9 billion and net income surpassing $1 billion [F1]. This sizeable revenue figure signifies a company leveraging its broad market presence effectively, though underlying metrics reveal nuanced performance dynamics. The company's liquidity position, indicated by a current ratio of approximately 1.04, paints a picture of balanced working capital—not overly ample nor constrained—reflecting prudent cash flow management that supports ongoing operations without risking tightness [F1].

The fourth quarter was especially telling; revenues rose by 35.7%, driven heavily by new business additions rather than internal organic demand growth [N13]. Net income also outpaced estimates, boosted partly by investment income—a somewhat atypical but noteworthy factor positioning earnings above conservative projections [N9]. Such gains indicate the firm's multifaceted approach to profit generation beyond core brokerage commissions.

Dissecting the Moat: Scale, Network, and National Healthcare Ambitions

Brown & Brown’s foundational moat rests on its sweeping insurance brokerage network that enables comprehensive product offerings and service diversity across markets [valye_report_excerpt]. The sheer scale functions as a competitive barrier, facilitating client retention through extensive access points and specialized coverage options.

Further sharpening its edge is the recent inauguration of the National Healthcare Practice—an integrated service line targeting healthcare sector clients with tailored insurance solutions [valye_report_excerpt]. This initiative represents more than market diversification; it signals a strategic deepening of expertise in a high-demand segment where specialized knowledge can translate to durable client relationships amid rising regulatory complexity and cost pressures.

The healthcare push appears well-timed as varied health risks and evolving employer demands heighten the need for bespoke coverage strategies within insurance brokerage circles [analysis]. The move potentially insulates Brown & Brown against commoditization trends impacting broader commercial lines.

Organic Revenue Headwinds and What They Mean

A paradox emerges when peeling back top-line gains: while total revenues surged substantially by acquisition contributions, the organic revenue base shrunk by 2.8% in Q4 alone [N13]. This contraction spotlights operational challenges in fueling same-store sales growth—a vital metric for assessing sustainable business momentum.

The reliance on external acquisitions to drive growth invites questions about integration efficacy, cost synergies realization, and whether overall profitability can weather stagnant or declining organic inflows [N14]. Market reaction included share price declines post-earnings announcement reflecting investor caution towards this imbalance between headline growth figures and core operational performance.

Does this hint at deeper structural pressures within Brown & Brown’s traditional segments or heightened competition eroding pricing power? It is an important focal point for stakeholders looking beyond headlines.

The Litigation Landscape: Risks in Balance

Insurance brokerage is inherently exposed to litigation risks stemming from contractual disputes or regulatory scrutiny [S1]. Brown & Brown candidly acknowledges ongoing claims but maintains these are immaterial to overall business health [valye_report_excerpt].

Within an industry accustomed to episodic legal challenges, this stance corresponds to typical risk profiles rather than exceptional threat levels. However, monitoring evolving legal environments remains essential since protracted or expanded claims could escalate into financial or reputational hazards.

For now, litigation factors do not obscure the firm's fundamental operating outlook but should be tracked as part of comprehensive risk management frameworks [S1].

How Brown & Brown Stands Among Insurance Brokerage Peers

Positioning within its peer group reveals both commonalities and distinctions. Industry players like Aon and Willis Towers Watson also report robust retention efforts counterbalancing some organic growth softness but have leaned heavily into expense efficiency measures for margin recovery [N2][N3][N4].

Gallagher exhibits similar patterns yet supplements them with dividend enhancements signaling confidence in cash flow stability [N4]. Compared to these peers, Brown & Brown’s embrace of investment income as an earnings tailwind distinguishes it somewhat—potentially affording temporary earnings leverage absent elsewhere.

However, this reliance raises questions on earnings quality purity relative to peers primarily driven by underwriting success or fee-based business expansion [analysis]. How BRO’s strategy evolves alongside peers under shifting economic conditions merits continuous observation.

Investment Income: A Surprising Earnings Catalyst

Quarterly reports disclosed that investment income played an outsized role in exceeding fourth-quarter earnings expectations [N9][N11]. This suggests effective asset deployment beyond baseline commission revenues—perhaps through portfolio adjustments benefiting from favorable capital market conditions.

Whether such gains represent recurring streams or opportunistic spikes impacts the interpretation of underlying profitability trends. As investment yields can fluctuate depending on interest rate cycles or market volatility, their contribution injects an element of variability into earnings forecasts.

Henceforth, stakeholders might probe Brown & Brown's strategic capital allocation policies governing investment assets vis-à-vis core operational reinvestment priorities [F1].

Liquidity and Balance Sheet Health Under the Microscope

From a balance sheet perspective, current assets approximate $8.61 billion against current liabilities near $8.29 billion at fiscal year-end 2025—yielding the modest current ratio of 1.04 documented earlier [F1]. This scenario affords just enough short-term liquidity to cover obligations without triggering solvency concerns.

Supplementary filings highlight manageable debt maturities distributed across senior notes due through 2052 [S2], affirming a structured capital framework designed for long-term stability while preserving operational flexibility.

Cash reserves exceed $1 billion—a comfortable buffer supporting working capital needs along with potential acquisition activity supplemental funding [F1]

This financial footing implies deliberate conservatism aimed at balancing growth ambitions against credit risk tolerance.

Future Outlook: Growth Drivers and Potential Pitfalls

Looking ahead, growth trajectories suggest continued acquisition activity supplemented by strategic expansions of specialized units like the National Healthcare Practice will remain pivotal [valye_report_excerpt][N13]. Yet success hinges critically on converting these into sustained organic momentum rather than transient top-line boosts.

Addressing the underlying 2.8% organic revenue decline demands targeted operational initiatives encompassing client engagement enhancements, cross-selling acceleration within healthcare verticals, and technology investments facilitating seamless underwriting processes.

Simultaneously, vigilant legal risk management must persist given ongoing albeit contained litigation exposures flagged by management [S1]. Moreover, peer moves warrant close scrutiny as competitors advance expense rationalization or customer retention campaigns that could jar market share distribution dynamics.

Ultimately, how adeptly Brown & Brown integrates acquired firms’ cultures and systems while scaling specialty offerings will shape its capacity to sustain competitive differentiation amidst intensifying industry headwinds.

This analysis is intended solely for informational purposes to provide insight into Brown & Brown Inc.’s recent performance and strategic positioning without offering any investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments