Agios Pharmaceuticals: Strategic Focus and Financial Fortitude Amid Rare Disease Market Challenges

Agios navigates commercialization milestones and regulatory pressures while preserving innovation in rare hematology therapies.

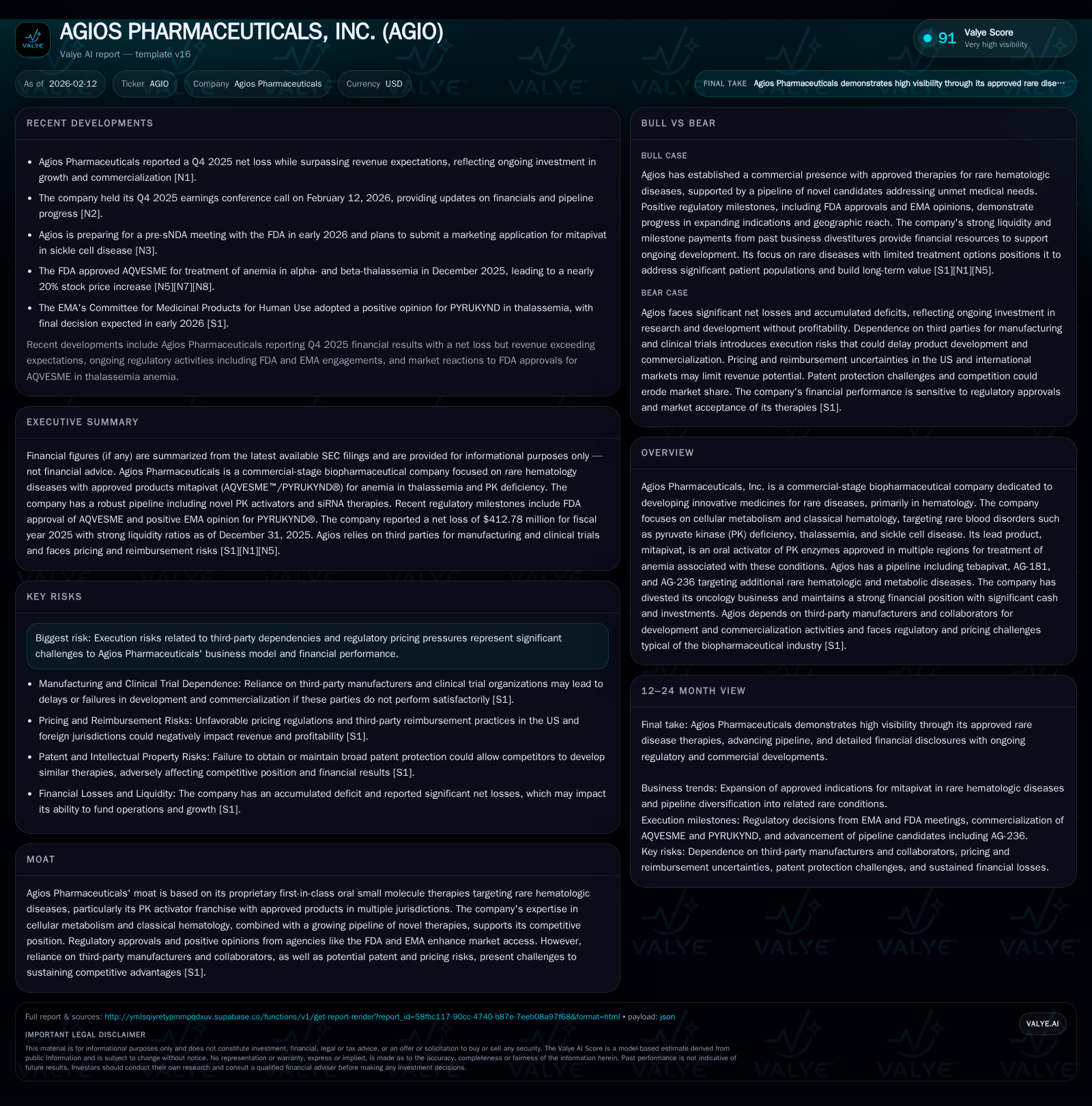

Agios Pharmaceuticals has transitioned into a commercial-stage biopharmaceutical company with its lead product mitapivat approved for rare hematologic conditions, marking a significant milestone in its mission. Despite operational and regulatory headwinds, including reliance on third-party partnerships and pricing challenges, the company maintains a solid balance sheet and is advancing a pipeline aimed at expanding its therapeutic reach. Critical scrutiny reveals that Agios’ strategic divestment from oncology sharpens focus but underscores execution risks inherent in specialty pharmaceuticals.

From Innovation to Commercialization: Agios’ Launch and Lead Products

Agios Pharmaceuticals stands at an inflection point, shifting from its pioneering role in cellular metabolism research toward real-world delivery of therapeutic solutions for rare hematologic diseases. Central to this transformation is mitapivat, an oral activator of pyruvate kinase (PK) enzymes—a first-in-class therapy now approved under brand names such as PYRUKYND® in the United States, Saudi Arabia, the European Union, and Great Britain. These approvals cover treatment of anemia in conditions including PK deficiency and both non-transfusion-dependent and transfusion-dependent alpha- or beta-thalassemia [S1]. This successful commercialization leap signals Agios' ability to translate scientific innovation into tangible patient impact.

Yet this transition is not without inherent tensions: moving beyond clinical development to sustainable product sales demands robust infrastructure, market education, and regulatory navigation. The company's recent Q4 earnings underscore this delicate balance—achieving revenue beats while still absorbing considerable net losses [N1][F1]. It raises the question: can Agios effectively scale its commercial operations while preserving its innovative edge?

Navigating the Nuances of Rare Hematologic Disorders

The hematology diseases targeted by Agios—PK deficiency, thalassemia variants, sickle cell disease—each represent ultra-rare blood disorders characterized by complex pathophysiology and diverse clinical manifestations. Such rarity inherently constrains market size yet intensifies unmet needs due to limited existing therapies.

This duality shapes the commercial landscape. On one hand, small patient populations demand precision medicine approaches that justify premium pricing; on the other hand, fragmented patient identification, reimbursement hurdles, and healthcare system variabilities complicate access [S1]. The intricate science behind modulating cellular metabolism via PK activation further differentiates treatment modalities but also elevates educational demands among prescribers.

Understanding these subtleties is crucial to grasping Agios’ strategic positioning: their products are not mass-market blockbusters but highly specialized interventions aiming at profound clinical impact within niche segments.

Pipeline Progress: Expanding Beyond Mitapivat

Mitapivat’s validation offers a platform upon which Agios ambitiously extends its pipeline. Candidates such as tebapivat continue exploration in related metabolic pathways; AG-181 and AG-236 diversify into other rare hematologic or metabolic diseases [S1]. This multi-pronged approach may foster incremental growth vectors beyond the current franchise.

However, inherent in such developmental pipelines are high attrition risks. Clinical success depends on nuanced trial outcomes and regulatory reviews—not certainties even for well-studied mechanisms. Hence, although promising candidates hint at growth potential, they also embody execution risk profiles common in specialty pharma.

Future success thus hinges on adept management of scientific rigor alongside efficient resource allocation—a challenging equilibrium amid evolving competitive landscapes.

Financial Landscape: Interpreting the Recent Earnings and Balance Sheet Strength

Agios’ Q4 earnings reported revenue surpassing consensus amidst an expanding commercial footprint; however, they simultaneously disclosed substantial net losses totaling over $412 million for fiscal year 2025 [N1][F1]. The company holds cash and cash equivalents near $89 million with current assets exceeding liabilities by an approximate ratio of 11.46 [F1], indicating robust liquidity.

This financial portrait reflects a typical biopharma growth phase scenario—heavy investment in commercialization infrastructure and pipeline R&D dampens short-term earnings while positioning for future profitability. Sustaining this model requires judicious capital deployment to extend runway without eroding shareholder value excessively.

Amid these dynamics lies investor scrutiny on operational efficiency metrics moving forward: how quickly can top-line momentum translate into positive net income? Moreover, macroeconomic factors influencing funding environments could alter cost-of-capital assumptions.

Third-Party Dependencies: Risks and Mitigation Strategies

A salient vulnerability for Agios resides in extensive dependence on external partners for manufacturing, clinical trials, and commercialization activities [S1]. Third-party manufacturers safeguard supply continuity for key products like PYRUKYND® and AQVESME™, yet any disruption—from quality failures to capacity constraints—could derail critical timelines or damage reputation.

Similarly, outsourcing of clinical trial conduct exposes Agios to variability in data integrity, regulatory compliance adherence, or timeline management. Collaboration agreements further compound complexity since strategic misalignments or contract disputes restrict agility.

To mitigate these risks requires not only strong contractual oversight but also contingency planning—diversifying suppliers where feasible and fostering transparent communication channels across partners. How well Agios navigates this intertwined ecosystem will influence both operational resilience and competitive positioning.

Regulatory and Pricing Pressures: External Forces Shaping Growth

Pricing and reimbursement landscapes represent formidable external frameworks shaping Agios' growth prospects. Both U.S. legislation reforms targeting drug pricing transparency and international policies imposing cost containment challenge ability to realize premium pricing despite product novelty [S1].

Furthermore, reimbursement decision-making processes vary widely across jurisdictions affecting patient access patterns. Even favorable clinical data may encounter hurdles through health technology assessments or insurer coverage criteria.

These realities impose cautionary boundaries around revenue visibility forecasts. While innovative status affords some leverage, increasing government scrutiny continues eroding broad pricing power—a structural theme confronting many specialty pharma entities today.

Competitive Moat Analysis: Proprietary Technology and Market Access

Agios builds a defensible moat through patented small molecule activators of PK enzymes—the first therapeutic class addressing underlying enzymatic deficiencies causing hemolytic anemias [S1]. Regulatory endorsements from authorities like FDA and EMA validate clinical efficacy facilitating multiregional market entry.

However, patent protection timelines require vigilant management; expiration or narrow patent claims might invite biosimilar entrants threatening market share erosion over time. Additionally, the niche nature of indications offers limited economies of scale restraining cost advantages compared with larger biopharma competitors.

Therefore, sustaining competitiveness depends on continuous innovation cycles—either refining existing therapies or discovering new targets—and preserving regulatory exclusivities.

Strategic Divestments: Oncology Exit and Implications

Recently divesting its oncology segment signals Agios’ commitment to concentrate resources fully on rare hematologic diseases [S1]. This move potentially simplifies operational complexity allowing focused capital allocation towards pipeline advancement within core competencies.

From a valuation perspective, shedding non-core assets might enhance clarity around growth drivers enhancing investor appeal. Concurrently it underscores an acceptance that oncology investments did not yield anticipated strategic synergies or returns.

Can this sharper strategic lens accelerate milestones realization? Time will elucidate whether this discipline enhances agility amid a competitive therapeutic category growing ever more crowded.

Investor Sentiment and Market Expectations Post-Q4 Earnings

Anticipation ahead of Q4 earnings was tilted towards optimism given prior trajectory of revenue growth; indeed actual results surpassed revenue estimates though marked by persistent losses [N3][N1]. Market reactions reflect measured enthusiasm balancing commercial progress against profitability hurdles.

Analysts emphasize scrutiny on upcoming quarterly data for clearer evidence of sustainable margin improvement or scalability gains [N2]. Meanwhile volatility persists as investors weigh execution risks intrinsic to third-party reliance alongside regulatory uncertainties.

The stock’s performance post-earnings release may oscillate accordingly—as speculative interest contends with fundamental reevaluation considering longer-term pathway feasibility.

Future Catalysts and Uncertainties Impacting Valuation

Looking ahead several pivotal events stand poised as valuation inflection points: pending regulatory decisions related to additional indications; late-stage clinical readouts signaling expansion potential beyond mitapivat; evolving drug pricing policies influencing revenue projections [S1][N1][N3].

Each catalyst carries asymmetric risk-reward implications—positive outcomes could validate growth narratives while delays or disappointments might pressurize multiples assigned by markets accustomed to milestone-driven biotech swings.

Navigating these uncertainties requires robust internal governance alongside adaptive strategy enabling rapid response to systemic changes within healthcare ecosystems.

The question remains whether Agios’ blend of scientific innovation blended with commercial maturation can yield durable value creation amidst a landscape rife with both opportunity and complexity.

This analysis is intended solely for informational purposes based on publicly available data as of February 2026. It does not constitute investment advice or a recommendation regarding any securities mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments