Ethan Allen Interiors: Navigating Raw Material Shocks and Real Estate Challenges to Sustain Brand Strength and Financial Resilience

Ethan Allen’s recent earnings beat reflects operational discipline amid inflation and real estate risks.

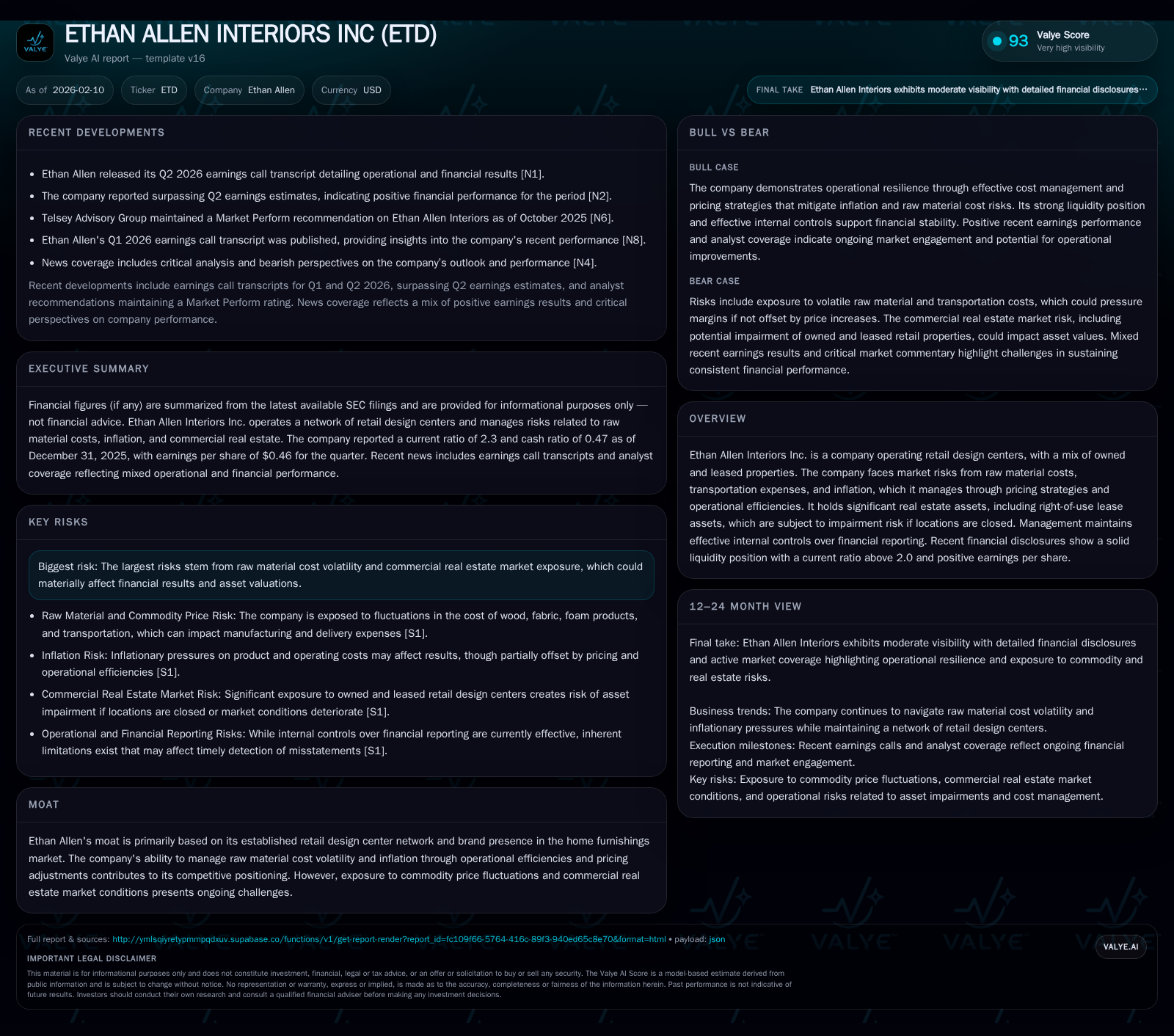

Ethan Allen Interiors Inc. delivered a Q2 2026 earnings performance exceeding expectations, underscoring effective cost management despite ongoing raw material price volatility and inflationary pressures. The company’s expansive network of owned and leased retail design centers forms a strategic asset base but also introduces impairment risks amid shifting commercial real estate conditions. Balanced liquidity and robust internal controls provide a cushion for navigating uncertainties while preserving Ethan Allen's competitive presence in home furnishings.

Earnings Beat Signals Underlying Operational Strength

Ethan Allen Interiors surprised the market with its Q2 2026 earnings results that not only topped analyst expectations but also reflected disciplined operational execution under challenging conditions [N1][N2]. The company reported positive earnings per share alongside a robust liquidity position marked by a current ratio well above 2.0 as of December 2025 [F1]. This financial footing demonstrates Ethan Allen's capacity to sustain growth from within despite external headwinds such as input cost inflation and rising transportation expenses.

The outperformance is rooted in careful cost control, which complements the company’s ability to adjust retail pricing effectively without dampening demand. Net income of approximately $9.6 million for the most recent quarter underscores an underlying operational strength that tangibly flows through the income statement, bolstered by sound working capital management.

Raw Material Volatility: Managing Costs in a Turbulent Commodity Environment

Raw materials remain a primary source of uncertainty for Ethan Allen, given their direct impact on cost of goods sold. Key inputs include petroleum-based foam products, sensitively linked to fluctuating oil prices, as well as wood and fabric components [S1]. These elements are subject to commodity market dynamics beyond management’s control.

To address these challenges, the company employs tactical pricing decisions aimed at maintaining margin integrity while remaining competitive. Simultaneously, procurement strategies seek to identify lower-cost alternatives or substitute raw materials without compromising product quality or aesthetic appeal. Such maneuvering is critical in cushioning margins when commodity costs surge.

Transportation expenses also represent a notable component of input costs, exposed to volatility in shipping container availability and fuel price fluctuations [S1]. Ethan Allen evaluates whether price increases are warranted periodically, mindful of consumer sensitivity but supported by competitors facing similar headwinds.

Inflation's Double-Edged Sword: Pricing Power Versus Input Pressures

Inflation has manifested not only through raw material hikes but also via broader manufacturing overheads including labor and logistics. Ethan Allen has partially mitigated these via operational efficiencies incorporating workforce optimization measures like reduced headcount [S1]. These internal levers help offset incremental inflationary burdens without solely relying on price increases.

On the revenue side, the company exercises measured pricing adjustments to preserve margin health while balancing consumer acceptance in a competitive retail furniture market. This delicate act underscores Ethan Allen’s nuanced understanding of demand elasticity amid economic cycles.

Strategic Footing in Retail Real Estate: Owned Versus Leased Locations

The company's physical retail presence encompasses 142 design centers spread across various markets [valye_report_excerpt][S1]. Among these locations, ownership versus leasing manifests strategically: 48 stores are owned outright while 94 operate under leases. This mix provides Ethan Allen both capital investment benefits in owned sites and operational flexibility afforded by leases.

Owning stores allows greater control over location branding and long-term asset appreciation potential, yet requires higher upfront capital deployment and exposes the balance sheet to real estate market whims. Conversely, leased locations minimize capital intensity but carry obligations reflected as right-of-use assets on the balance sheet.

This balanced footprint allows the company adaptability responsive to local market conditions while enabling consistent delivery of the Ethan Allen experience through branded design centers.

Impairment Risks in a Shifting Commercial Property Market

The commercial real estate environment injects uncertainty into asset valuations affecting both owned properties and leased store rights-of-use [S1][valye_report_excerpt]. The unamortized right-of-use lease assets stood at around $109 million as of June 30, 2025—a significant figure that could result in impairment charges if site closures occur amid weakening rental markets.

Should economic or consumer trends necessitate closing design centers, liquidating owned properties or winding down leases during less favorable periods risks write-downs affecting income statements. These potential impairments represent notable contingent liabilities embedded within Ethan Allen's financial profile.

Internal Controls and Governance: Pillars of Financial Integrity

Management underscores its commitment to financial reporting integrity through comprehensive internal control systems [S1]. These accounting frameworks aim to ensure accuracy, compliance with GAAP standards, and safeguard assets against irregularities or misstatements.

The Board’s audit committee—composed solely of independent directors—exercises robust oversight over these processes. Their mandate spans routine assessments of internal controls, audits coordination with external accounting firms like CohnReznick LLP who conducted recent attestations for fiscal years ending June 2025 [S1].

This governance layering reinforces investor confidence by upholding transparency and accountability across financial disclosures.

Liquidity Profile and Balance Sheet Health Amid Market Uncertainties

Liquidity metrics reveal Ethan Allen is well-positioned for near-term resilience amidst macroeconomic volatility. At December 31, 2025, current assets totaled $312 million against current liabilities near $136 million yielding a strong current ratio approximately equal to 2.3 [F1]. Cash and cash equivalents alone stood at $64 million—a substantial liquidity reserve supporting operational continuity or opportunistic investments.

Positive net income results further enhance self-financing capacity without excessive reliance on external debt markets or equity issuance. Such balance sheet robustness affords strategic maneuvering room necessary for confronting input cost fluctuations or potential real estate repositioning.

Assessing Ethan Allen’s Competitive Moat Within Home Furnishings

Ethan Allen benefits from entrenched brand recognition paired with an extensive retail design center network nationally recognized among consumers targeting premium home furnishings [valye_report_excerpt]. This physical footprint reinforces personalized design service capabilities distinguishing it from purely e-commerce competitors.

Moreover, adeptness in managing raw material pricing variability—through operational discipline combined with selective retail price authority—creates barriers against margin erosion typical in commoditized offerings. Although exposed materially to common headwinds affecting peers (commodity inflation), Ethan Allen’s integration across design, manufacturing input sourcing, and merchandising supports durable competitive differentiation.

Outlook: Balancing Growth Ambitions with Structural Risks

No material changes have been reported recently regarding risk factor profiles as per Q2 filings through February 2026 [S2], suggesting stable risk awareness though vigilance remains essential given prevailing uncertainties.

Continued inflation monitoring alongside commodity cost trends will dictate future pricing strategies required to preserve profitability without impairing demand momentum [N1]. Concurrently, active evaluation of retail footprint rationalization or expansion plans must weigh impairment risks tied to volatile commercial real estate conditions carefully.

Management’s ability to navigate these intertwined challenges will determine how effectively Ethan Allen sustains both top-line growth ambitions and asset base quality moving forward.

This analysis synthesizes institutional disclosures including SEC filings ([S1], [S2]) and recent earnings call insights ([N1], [N2]) alongside companyfact data ([F1]). It avoids speculative assertions beyond documented information while providing contextually grounded commentary on industry nuances affecting Ethan Allen Interiors Inc.’s operating environment and financial posture.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments