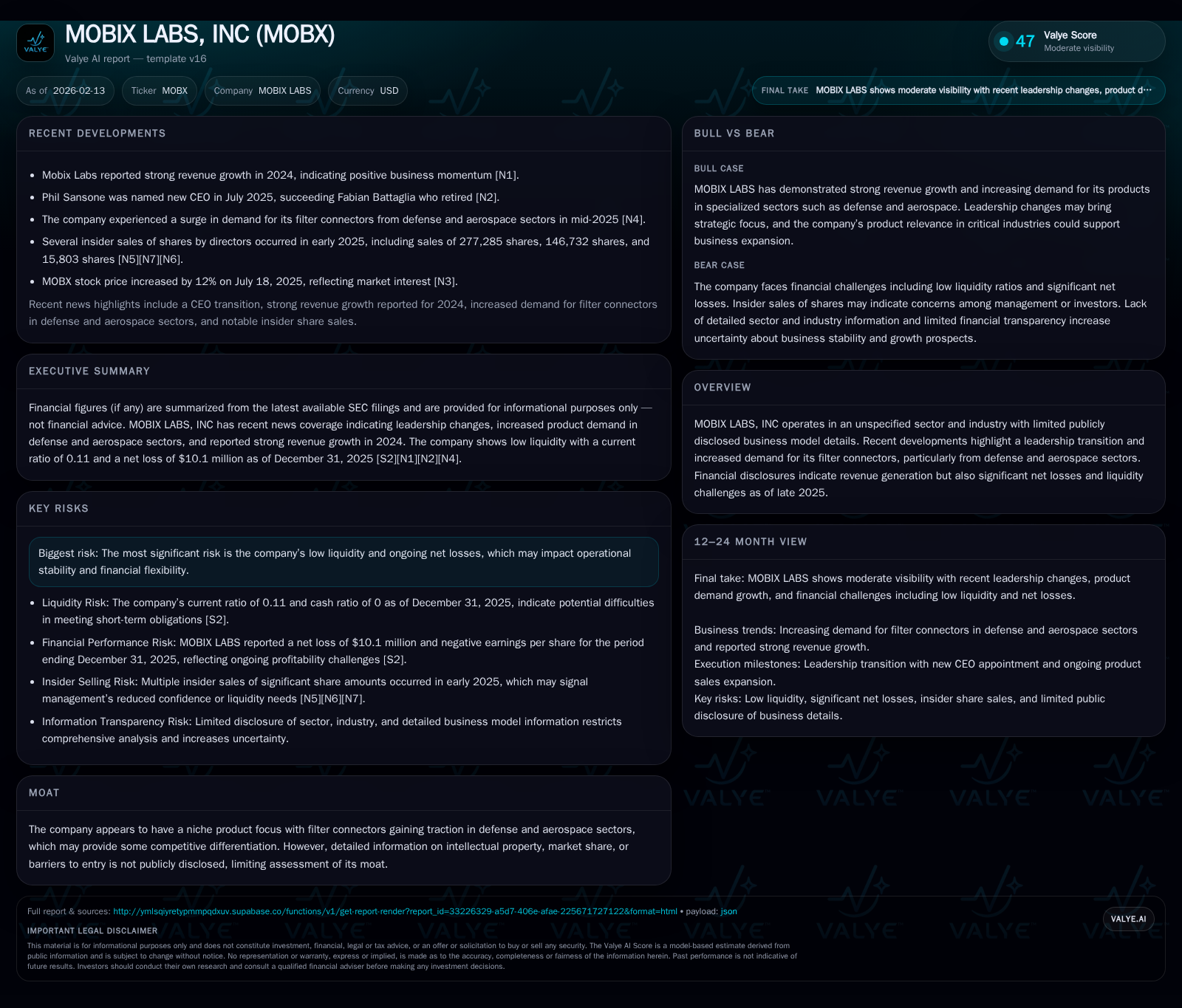

MOBIX LABS: Surging Defense Demand Meets Severe Liquidity Strain Amid Transition

MOBIX LABS exhibits robust niche revenue growth from filter connectors yet battles deep financial constraints and strategic uncertainty.

MOBIX LABS has recently captured encouraging market momentum with its specialized filter connectors gaining traction in defense and aerospace sectors. This growth contrasts sharply with its precarious liquidity position, highlighted by a current ratio near 0.11 and substantial net losses exceeding $10 million. A pending leadership transition marks a critical inflection point as the company attempts to convert short-term promise into sustainable operational stability amid mounting financial pressures.

From Innovation to Traction: MOBIX's Rising Demand in Defense & Aerospace

MOBIX LABS has quietly carved out a focused niche with its filter connector products—a specialized component category that has recently attracted notable interest from defense and aerospace sectors. This traction materialized as strong revenue growth in calendar year 2024, culminating in approximately $2.5 million reported by Q1 of fiscal 2025 [N1][F1][S1]. Although the company does not broadly disclose detailed segment breakdowns or industry classification, the surge in demand from strategic industries suggests that MOBIX’s technology meets critical technical or quality thresholds prized in highly regulated markets like defense.

This filtered yet potent demand signals meaningful business momentum. Such sectors conventionally require highly reliable connectors that can withstand rigorous environmental and electromagnetic interference standards—indicating MOBIX’s product may possess engineering attributes that resonate well within this challenging customer base. However, the lack of more granular commercial or competitor data tempers exuberance; while promising, this foothold remains narrowly defined in both scope and scale at present.

Leadership Transition and Strategic Direction: Navigating Change

At the core of MOBIX’s unfolding narrative is a leadership change occurring amid this pivotal phase of growth and strain [valye_report_excerpt][S1]. Details surrounding management shifts are sparse, but transitions at executive levels frequently underscore intentions to realign strategic priorities or infuse fresh operational discipline.

Given the liquidity crunch and persistent losses MOBIX faces (discussed below), steady leadership is paramount to coordinate crisis management while capitalizing on emerging product opportunities. The new incumbents will need to balance driving contract expansions in defense/aerospace against tightening financial controls to sustain runway. In an environment where nimbleness counts, leadership vision will likely set the trajectory between recovery and potential distress.

Deep Dive into Financials: Revenue Growth versus Persistent Losses

The juxtaposition between incremental revenue advances and ballooning net losses draws sharp focus onto MOBIX’s operational dynamics [N1][F1][S1][S2]. The reported $2.5 million revenue figure for early 2025 marks an advance relative to prior years—but net income lags dramatically behind with a loss north of $10 million for the full fiscal year ending September 2025.

This disparity suggests high fixed costs, investment-heavy activities (possibly R&D or production scale-up), or inefficiencies weighing down profitability. While investor enthusiasm might gravitate toward top-line gains, underlying burn raises flags about cost structure sustainability absent immediate mitigation or scaling benefits. Thus, the revenue trajectory evidences potential but is far from reflecting economic viability on its own.

Crunching the Numbers: Liquidity Ratios and Cash Constraints

MOBIX’s liquidity position paints an urgent picture that overshadows optimistic sales signs [F1][S1][S2]. End-2023 cash on hand was a mere $7,525—practically negligible for funding ongoing operations or unexpected expenses. Meanwhile, total current assets hovered around $2.9 million by late 2025 against crushing current liabilities exceeding $25.2 million.

The resulting current ratio of roughly 0.11 stands well below traditional thresholds considered safe (>1), flagging severe short-term solvency risk if obligations mature imminently without fresh financing or drastic cost reductions next quarter(s). Even factoring typical working capital cycles in industrial manufacturing contexts, this gulf suggests imminent liquidity pressure.

This structural imbalance likely imposes constraints on supplier negotiations, staff retention, and capital expenditures—any further deterioration threatens operational continuity absent external intervention.

Evaluating the Moat: Niche Focus on Filter Connectors Without Clear Barrier Metrics

MOBIX's specialization in filter connectors offers a concentrated advantage within a technically demanding segment favored by defense-related contracts [valye_report_excerpt]. By focusing resources on perfecting these components' performance under stress conditions typical in aerospace applications, MOBIX may cultivate reputational goodwill difficult for generic competitors to replicate rapidly.

Yet there is scant evidence pointing to legally enforceable intellectual property protections—such as patents—or defensible market share metrics that would confirm durable barriers to entry. Without these safeguards, potential competitors could erode share if switching costs are low or technological know-how diffuses.

Therefore, while MOXIBX's moat seems grounded in product specificity and sectoral fit rather than overt legal protections or scale economies, its durability remains unproven publicly—a cautionary note for analysts assigning valuation premiums based on presumed defensibility.

Risk on the Horizon: Managing Operating Losses Amidst Market Uncertainty

The twin specters of deteriorating liquidity and sustained operating losses constitute central risks putting MOBIX’s fate in jeopardy [valye_report_excerpt][F1][S1]. If cash depletion continues unchecked beyond near term without compensatory capital inflows or expense cuts, solvency issues may force asset sales or restructuring undertakings detrimental to long-term value creation.

Moreover, economic uncertainties affecting defense budgets or aerospace supplier chains could delay contract ramp-ups, compounding revenue unpredictability just as burn rates remain elevated. Management faces an imperative trade-off: accelerate sales efforts which may increase costs further versus conserving cash potentially at the expense of market penetration speed.

Absent clear visibility into refinancing options or cost control strategies disclosed publicly thus far, these risks dominate MOBIX's immediate outlook.

Future Outlook: Can MOBIX Convert Promise into Sustainable Stability?

Now stands a crossroads where early-stage promise clashes with harsh financial reality [N1][valye_report_excerpt]. The nascent defense contract demand invites hope that expanded orders or breakthrough deals could elevate revenues materially in subsequent periods. Yet these prospects alone won’t suffice unless paired with operational efficiency improvements reducing losses sustainably.

Further complicating prospects is the absence of detailed guidance on planned financing measures—be it equity raises, debt arrangements, or strategic partnerships—to ease liquidity strain and fund necessary growth investments. Without clear remedial action paths integrated with commercial momentum, transforming short-term achievements into durable stability will be difficult.

Execution clarity from new leadership will be pivotal for credible turnaround narratives moving forward.

Investor Takeaway: Positioning amidst Growth and Financial Fragility

For buy-side stakeholders examining MOBIX LABS today, tension pervades every angle—entrepreneurial gain balanced precariously against financial fragility [N1][F1][S1]. The company’s unique niche product resonates well within specialized sectors like defense/aerospace providing tailwinds unseen at many rivals’ stages.

However, steep net losses combined with woefully inadequate liquid resources impose daunting near-term survival questions overshadowing growth stories. The leadership transition adds layers of uncertainty but might equally catalyze much-needed strategic discipline if executed effectively.

Ultimately, any valuation must incorporate this kinetic push-pull between promising top-line development and untenable balance sheet positions rather than defaulting to overly optimistic extrapolations or uniform pessimism.

Disclosure: This analysis is intended solely as an informational overview synthesizing publicly available data without providing investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments