Decoding Westin Acquisition Corp’s Financial Signals Amid Sparse Disclosures and Liquidity Concerns

An in-depth analysis reveals key financial insights and the challenges posed by limited public disclosures for Westin Acquisition Corp.

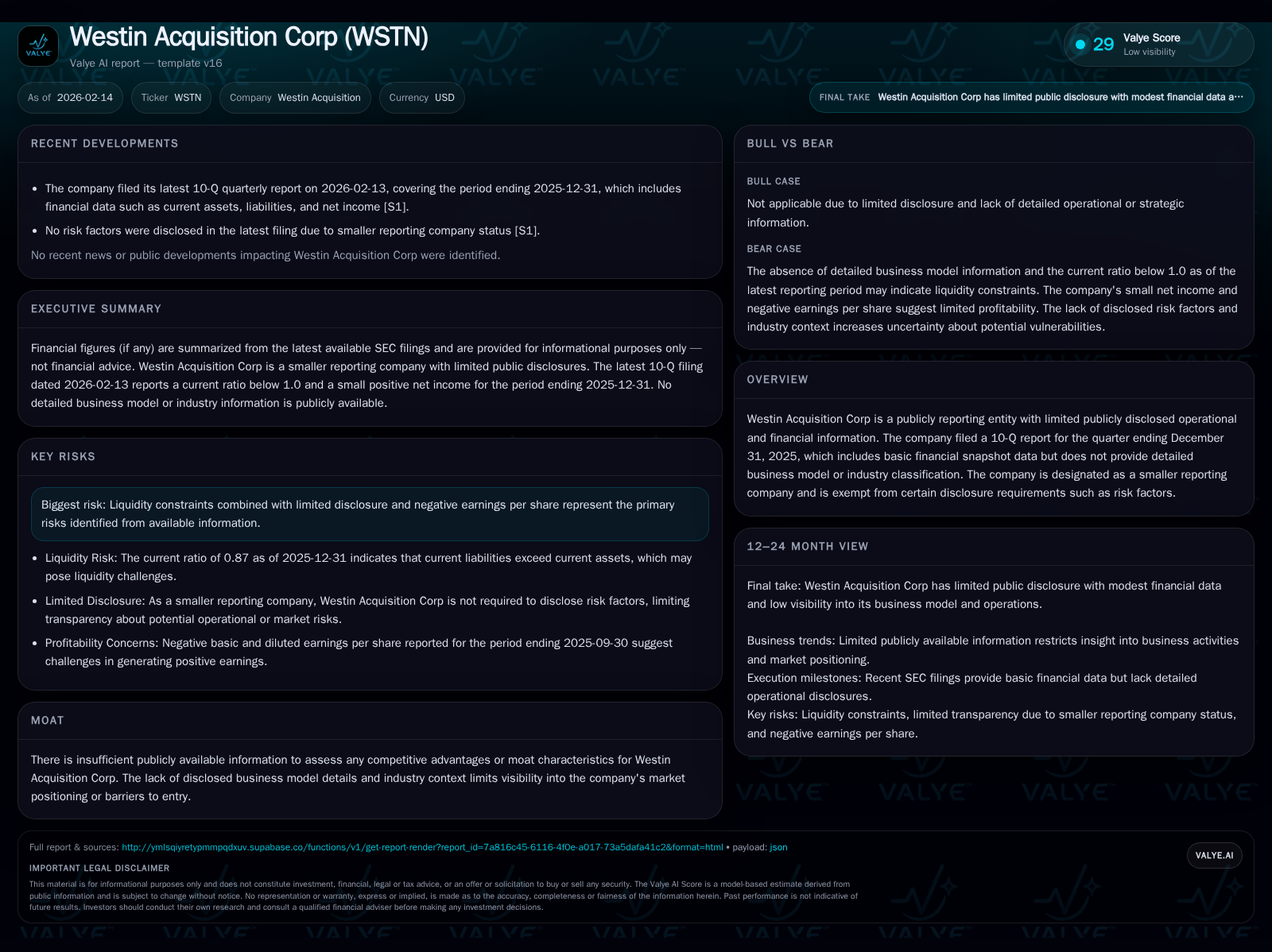

Westin Acquisition Corp operates under a veil of limited public information, classified as a smaller reporting company exempt from certain SEC disclosure requirements. Its latest 10-Q filing reveals a modest net income alongside a current ratio below one, highlighting liquidity pressures. The absence of clear business model details or industry classification complicates efforts to assess competitive positioning or risk factors. This memo unpacks the implications of these opaque signals within the context typical of acquisition vehicles.

Behind the Curtain: Unpacking Westin Acquisition Corp’s Quiet Existence

Westin Acquisition Corp stands as a company shrouded in relative silence within the public filings ecosystem. Identified solely as a smaller reporting company in its recent 10-Q submission dated February 13, 2026, it benefits from regulatory relief that exempts it from detailed disclosures typically mandated of larger firms [S2]. Notably absent are core elements such as business model description or industry classification — an omission placing substantial limits on anyone seeking to understand Westin’s operational fundamentals or competitive positioning.

This minimalistic approach to disclosure leaves Westin floating in an informational void where fundamental analysis relies heavily on sparse numerical indicators rather than narrative context. For analysts accustomed to dissecting comprehensive filings brimming with management discussion or segment breakdowns, this blank slate demands cautious interpretation.

A Closer Look at the Latest 10-Q: Financial Health Amid Sparse Details

The company's most recent quarterly results end December 31, 2025, reveal a few concrete datapoints amidst ample silence. Net income registers at a niche-positive $128,860 [F1], a figure that surprises given typical acquisition companies often operate near break-even pending deal completion. Current assets total $432,172 contrasted by current liabilities standing at $494,328 [F1], creating an immediate financial tension.

These raw numbers sketch a tenuous portrait of Westin's financial health absent operational color: profitability exists but is marginal; liquidity flags signal strain. The filing abstains from elaborating on cash flow dynamics or asset composition — components critical to evaluating sustainability.

Liquidity Tightrope: Parsing Current Assets versus Liabilities

With a calculated current ratio of approximately 0.87 [F1], Westin finds itself below the general benchmark of one often cited as indicating adequate short-term coverage. This suggests that its existing current assets may not suffice to fully meet short-term liabilities without drawing upon additional financing or asset liquidation.

In practical terms, this tight liquidity position could constrain operational flexibility and pressure management decisions around capital allocation or urgent financing solutions. Without details on the nature of these current assets — whether cash-like instruments or less liquid holdings — the exact runway duration remains uncertain.

The Elusive Business Model: Understanding What Westin Isn’t Saying

Westin's failure to disclose its industry sector or elaborate on strategic direction leaves stakeholders navigating in darkness regarding its core operations. This lack precludes any precise assessment of competitive differentiation or barriers to entry—features that typically inform considerations about economic moat strength.

One might conjecture typical SPAC vehicle characteristics given the acquisition nominal references and profile; however, no explicit confirmation exists within filings [S2]. The opacity also hinders peer comparison and renders attempts at benchmarking financially precarious.

Risk and Disclosure Dynamics for Smaller Reporting Companies

Under SEC guidelines governing smaller reporting companies, Westin is permitted leniency exempting mandatory risk factor disclosures traditionally included in Item 1A [S2]. This regulatory relaxation corresponds with lessened disclosure burdens but inversely impairs transparency regarding potential hurdles or material uncertainties facing the firm.

The absence of such risk narratives complicates investor due diligence efforts by removing a critical lens through which vulnerabilities might otherwise be identified. Whether liquidity risk or sector-specific headwinds exist goes unexplored in official communications.

Earnings Insight: Small Profits in a Sea of Unknowns

Achieving modest net income in this opaque setting poses questions about underlying revenue streams or expense controls practiced by Westin. With limited operational descriptions, it's challenging to determine if the profit reflects recurring operations, one-time gains, or financial investment returns.

Moreover, scale considerations are paramount; while positive earnings imply operational viability at some level, their sustainability absent visible growth initiatives remains an open question [F1].

What We Don’t Know: Assessing the Impact of Limited Industry Information

The absence of any declared industry affiliation curtails meaningful comparative valuation and forecasting exercises. Without contextualizing Westin alongside peer performance metrics or sector-specific trends, projecting future prospects is speculative at best.

Regrettably, this knowledge gap obstructs conventional analytic frameworks reliant on market size dynamics, competitive landscape assessments, and macroeconomic sensitivities that typically inform strategic expectations.

Potential Pathways Forward: Navigating Uncertainty and Market Positioning

Given Westin Acquisition Corp’s profile and typical patterns among acquisition entities classified similarly by regulators, one plausible scenario involves positioning itself as a shell entity potentially targeting future mergers or acquisitions. Such vehicles often maintain low operational footprints until deal announcements catalyze value realization.

Nonetheless, without concrete information about transactions underway or strategic partnerships disclosed publicly thus far, forecasting directional moves remains conjectural beyond acknowledging possible SPAC-like functions common among such firms.

Investor Implications: Risks and Opportunities in Opaque Waters

For investors evaluating exposure to Westin Acquisition Corp amid these conditions, the confluence of constrained liquidity (current ratio <1), negligible yet positive earnings figures ($128K), and scarce operating insight forms a complex risk-reward calculus [F1][S2].

Limited regulatory disclosure relief further underscores asymmetry in information accessibility—heightening diligence demands when assessing viability or capital allocation suitability.

While slim profits hint at some level of operational achievement uncommon for pure shell entities solely awaiting acquisition opportunities, pressing liquidity concerns necessitate close monitoring for signs of capital restructuring or fundraising activity.

Ultimately, the dearth of industry context coupled with fundamental opacity dictates prudent transparency expectations recognizing inherent analytical limitations intrinsic to Westin’s public reporting framework.

Disclaimer: This memo synthesizes available SEC-filed data points exclusively without extending investment advice. Readers should consider broader market context and seek additional sources before making allocation decisions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments