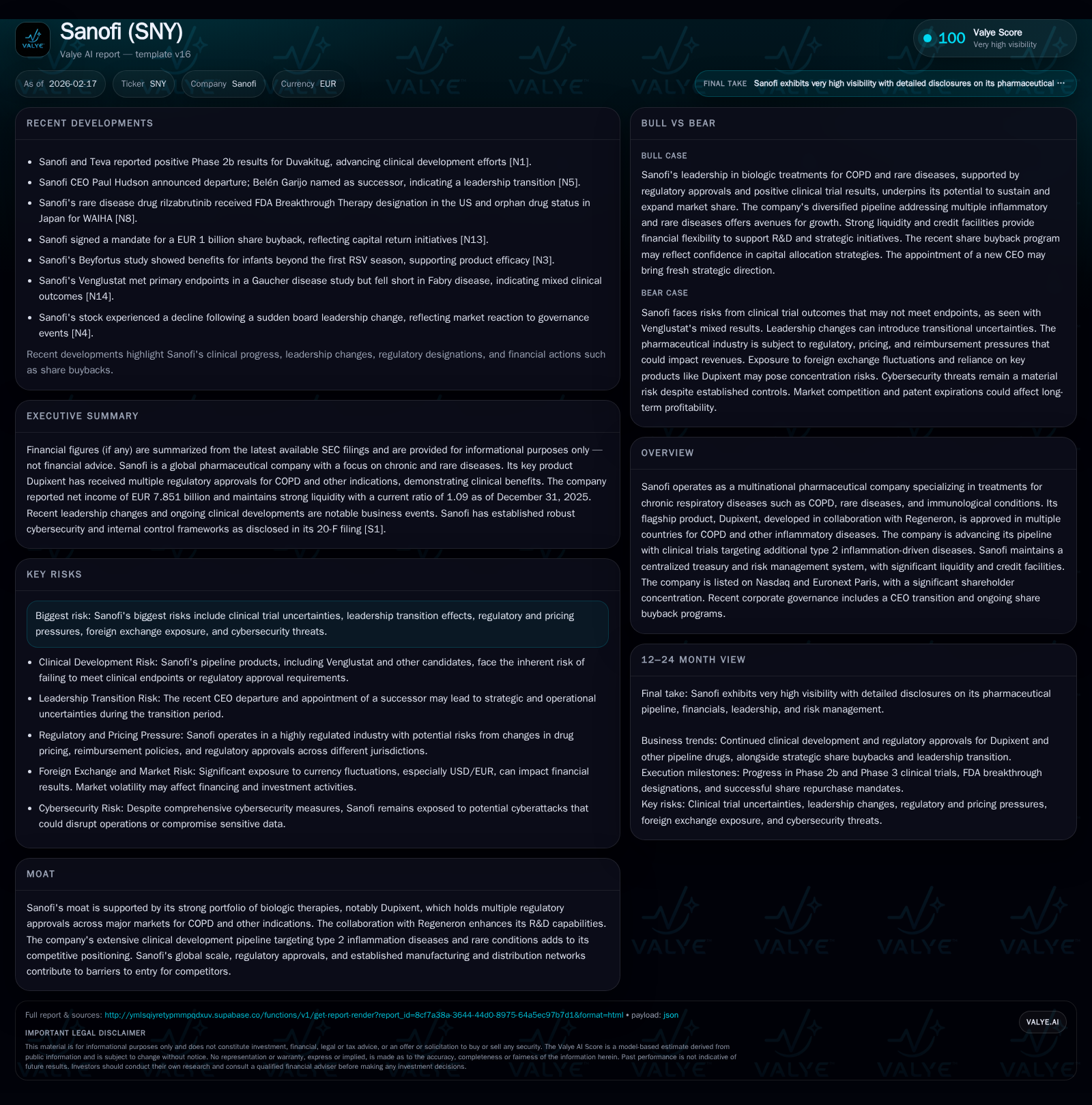

Sanofi's Strategic R&D and Leadership Shift Drive Next Growth Phase

Sanofi’s accelerated profit growth stems from Dupixent’s expansion, a strong pipeline in type 2 inflammation, and governance changes.

Sanofi transitioned from steady performance to rapid profit acceleration in 2025, largely driven by its flagship biologic Dupixent’s global approvals and launches in COPD and other inflammatory diseases. The company’s robust clinical pipeline, including positive Phase 2b results for Duvakitug and breakthrough therapy designations for rilzabrutinib, reinforces its biologics leadership. A sudden CEO change in early 2026 injected uncertainty, while disciplined capital allocation continues with significant share buybacks supported by solid liquidity and risk management. Investors should watch upcoming trial readouts and regulatory milestones amid persistent risks like clinical uncertainties and foreign exchange exposure.

From Steady Legacy to Accelerated Profit Growth: A Closer Look at Past Performance

Sanofi demonstrated a pronounced shift from relatively stable profitability metrics into a phase of significantly accelerated net income growth by FY2025. Net income rose by approximately 39.7% year-over-year to €7.85 billion from €5.62 billion in FY2024 [F1], reversing several years of modest or single-digit growth holds. This jump was primarily fueled by Sanofi's Dupixent franchise—the flagship biologic that expanded indications into the large COPD segment characterized by type 2 inflammatory phenotypes.

Meanwhile, shareholders' equity moderated downward from €77.9 billion at end-FY2024 to €71.7 billion at end-FY2025, reflecting share repurchases and possibly other capital restructuring activities amidst the aggressive buyback program [F1]. Despite this dip in equity base, return on equity (ROE) rebounded sharply from ~7.2% to around 10.9%, highlighting enhanced capital efficiency aligned with strong top-line drivers.

Historical performance (annual)

| FY | Net ($bn) | Net YoY |

|---|---|---|

| 2025 | 7.9 | +39.7% |

| 2024 | 5.6 | +3.3% |

| 2023 | 5.4 | -35.9% |

| 2022 | 8.5 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, CFO, OpInc, Capex, Div, Buybacks, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 10.9 |

| 2024 | 7.2 |

| 2023 | 7.3 |

| 2022 | 11.3 |

Source: SEC companyfacts cache [F1].

Note: Revenue and operating cash flows are not available from provided XBRL tags.

Biologic Innovation Momentum: Dupixent and Clinical Pipeline Updates

Dupixent's trajectory remains central to Sanofi’s biologic leadership strategy, underpinning much of the recent profit surge. Approved initially for type 2 inflammatory conditions like asthma and atopic dermatitis, Dupixent achieved landmark approvals for chronic obstructive pulmonary disease (COPD) characterized by elevated blood eosinophils — a clinically distinct type 2 inflammation-driven subset with up to a third greater exacerbation risk despite standard triple therapies [S1].

Regulatory achievements are extensive: after the EMA's positive opinion in mid-2024 followed by European Commission approval allowing add-on maintenance treatment for adults with uncontrolled COPD, China’s NMPA granted approval late that year too [S1]. Shortly thereafter, FDA endorsement positioned Dupixent as the first biologic treatment for COPD patients exhibiting an eosinophilic phenotype in the US [S1][N1]. By October 2025, Dupixent COPD indications were approved in over fifty countries globally with launches in seventeen major markets including Japan—illustrating rapid geographic expansion [S1].

Clinical data reinforce this success: pooled analyses from pivotal Phase 3 studies BOREAS and NOTUS showed significant reductions in exacerbation rates alongside improved lung function metrics versus placebo cohorts treated with ICS/LABA/LAMA regimens or LABA/LAMA combinations where ICS was unsuitable [N1][S1]. This efficacy profile strongly supports the product's position as a leading biologic option recommended by pulmonologists managing inadequately controlled COPD with type-2 inflammatory signatures.

Pipeline innovation further bolsters Sanofi’s moat. Positive Phase 2b results for Duvakitug—a collaborative asset targeting similar type-2 inflammation pathways in COPD—reflect continued efficacy enhancements adjacent to Dupixent's indication stack [N1]. Another compound advancing toward regulatory milestones is rilzabrutinib, which recently received Breakthrough Therapy Designation from FDA for warm autoimmune hemolytic anemia (WAIHA), supplemented by orphan drug status granted by Japanese authorities [N9][N10][S1]. Additional rare disease projects like Venglustat have also demonstrated clinical endpoints successes although with mixed results depending on condition subsets such as Gaucher versus Fabry diseases [N12][N14].

Taken together, these clinical-phase outputs advance both indication breadth and competitive differentiation within specialized immunology niches—a core component of Sanofi’s long-term biologics focus.

Leadership Transition Implications for Strategy and Market Perception

On February 12, Sanofi disclosed an abrupt CEO transition: Paul Hudson stepped down effective immediately, succeeded by current executive board member Belén Garijo [N3][S3]. The announcement triggered a material negative reaction wherein share prices dipped due to market concerns about leadership continuity amid a critical execution phase where pipeline maturation was expected to drive further growth [N6].

This change invites scrutiny regarding governance stability essential for maintaining innovation momentum characteristic of large pharmaceutical entities heavily reliant on sustained R&D investment cycles. As a multinational entity bound by French corporate law frameworks coupled with NASDAQ dual-listing governance provisions tailored as a foreign private issuer—the management transition places emphasis on properly balancing continuity plans against shareholder expectations noting that major shareholders retain notable voting concentration stakes potentially influencing directional decisions [S10][S21].

Internal communications emphasize adherence to AFEP-MEDEF recommendations complemented by robust oversight from audit committees addressing executive succession procedures while preserving operational integrity amidst external uncertainties such as pricing reforms or geopolitical influences affecting markets.

Capital Allocation Discipline: Buybacks, Dividends, and Liquidity Management

Sanofi maintains an assertive capital return posture underscored by share repurchases made under approved mandates amounting cumulatively to over €18 billion authorized through consecutive Annual Shareholders’ Meetings encompassing periods into late-2026 [S6][S8][S13]. In calendar year 2025 alone, over fifty million shares were repurchased primarily during H1-H2 at average prices close to €97/share post cancellation of roughly thirty million shares repurchased from L’Oréal—its largest shareholder—thereby enhancing per-share value metrics and reducing free float accordingly [S8][S11].

Dividend information lacks explicit numeric totals within XBRL but SEC filings confirm normalized payout policy signaling ongoing shareholder distributions juxtaposed against reinvestment needs typical of growth-stage pharma companies focused on emerging biologics franchises [S9].

Financial strength indicators show robust liquidity at €7.66 billion cash/cash equivalents complemented by substantial undrawn credit lines totaling about €8 billion split evenly between maturity dates ending December 2027 and March 2030—unencumbered by financial covenants providing comfort against unforeseen funding stresses or strategic flexibility needs [S4][S5].

Treasury management employs centralized cash pooling arrangements optimizing deployment across divisions spanning Europe, North America, Asia Pacific facilitating efficient currency risk hedging programs aimed at mitigating translation exposures common for euro-reporting multinationals operating widely denominated USD/CDN/JPY liabilities and assets through derivatives instruments including currency swaps and forwards valued at tens of billions notionals managed actively throughout FY2025 [S1][S17][S18]. This structured risk management alignment effectively smooths volatility impact on reported earnings despite macro FX fluctuations.

Risk Landscape: Regulatory, FX, and Trial Uncertainties

Beyond typical pharmaceutical risks inherent to product development cycles lies an amplified set stemming from reliance on biologic therapies subject to stringent regulatory scrutiny particularly regarding safety/efficacy profile validations through multi-phased clinical trials extending over numerous market jurisdictions globally [S10][S12],[N10],[N14]. Biological products such as Dupixent benefit from extended exclusivity attributed partly via orphan drug pathways—for rilzabrutinib’s WAIHA indication this includes FDA breakthrough designations accelerating review timelines but still carry uncertainties around actual commercial viability until final approvals remain pending.

Foreign exchange exposure persists albeit hedged systematically with derivative overlays; any unexpected policy shifts or financial market disruption represent underlying tail risks potentially translating into earnings volatility especially given USD/euro mix impacting reported consolidated accounts despite economic hedges targeting balance sheet equivalence rather than operational hedging fully neutralizing transactional impacts [S1].

Pricing pressures shaped by healthcare reform initiatives worldwide impose continued margin compression threats particularly when payer negotiations intensify amidst inflationary cost environments or tender competitiveness—reimbursement challenges could delay product uptake or restrict optimal pricing levers.

Cybersecurity remains elevated within technology-focused infrastructures supporting complex manufacturing processes and data-intensive R&D endeavors involving sensitive patient data protected under international privacy regimes proactively monitored via dedicated operational centers following frameworks such as NIST integrated into executive risk committee reporting cycles ensuring timely mitigation responses covering internal personnel training up to vendor risk assessments safeguarding supply chain integrity reliability [S22]-[S24].

Near-Term Catalysts and Milestones to Monitor

Looking forward without explicit management guidance available publicly yet detailed near-term inflection points include multiple anticipated Phase 3 clinical trial readouts building off encouraging Phase 2b endpoints—for example evaluations assessing Duvakitug efficacy across broadened COPD phenotypes alongside rare disease pipeline expansions notably rilzabrutinib’s progress through FDA priority review timelines concluding late Q1/Q2-26 enabling potential accelerated launch windows contingent on favorable outcomes evidence missed earlier confirmation.

Regulatory filings queued beyond COPD remain key watch items encompassing data submissions expected from Gaucher disease indications extending Venglustat development portfolio diversification efforts balancing recent mixed appraisal results affecting Fabry disease targets presenting ongoing scientific optimization requirements.[N1],[N3],

Post-CEO appointment integration effectiveness along with corporate governance recalibrations particularly shareholder activism reactions remain areas closely monitored as critical barometers validating continuation of strategic blueprint execution sustaining growth turnaround momentum forged over recent years.

Disclaimer: This analysis is based solely on publicly available information including SEC filings and news sources cited herein up to February 17th, 2026. It does not constitute investment advice or recommendations. Readers should independently verify facts before making decisions related to Sanofi.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments