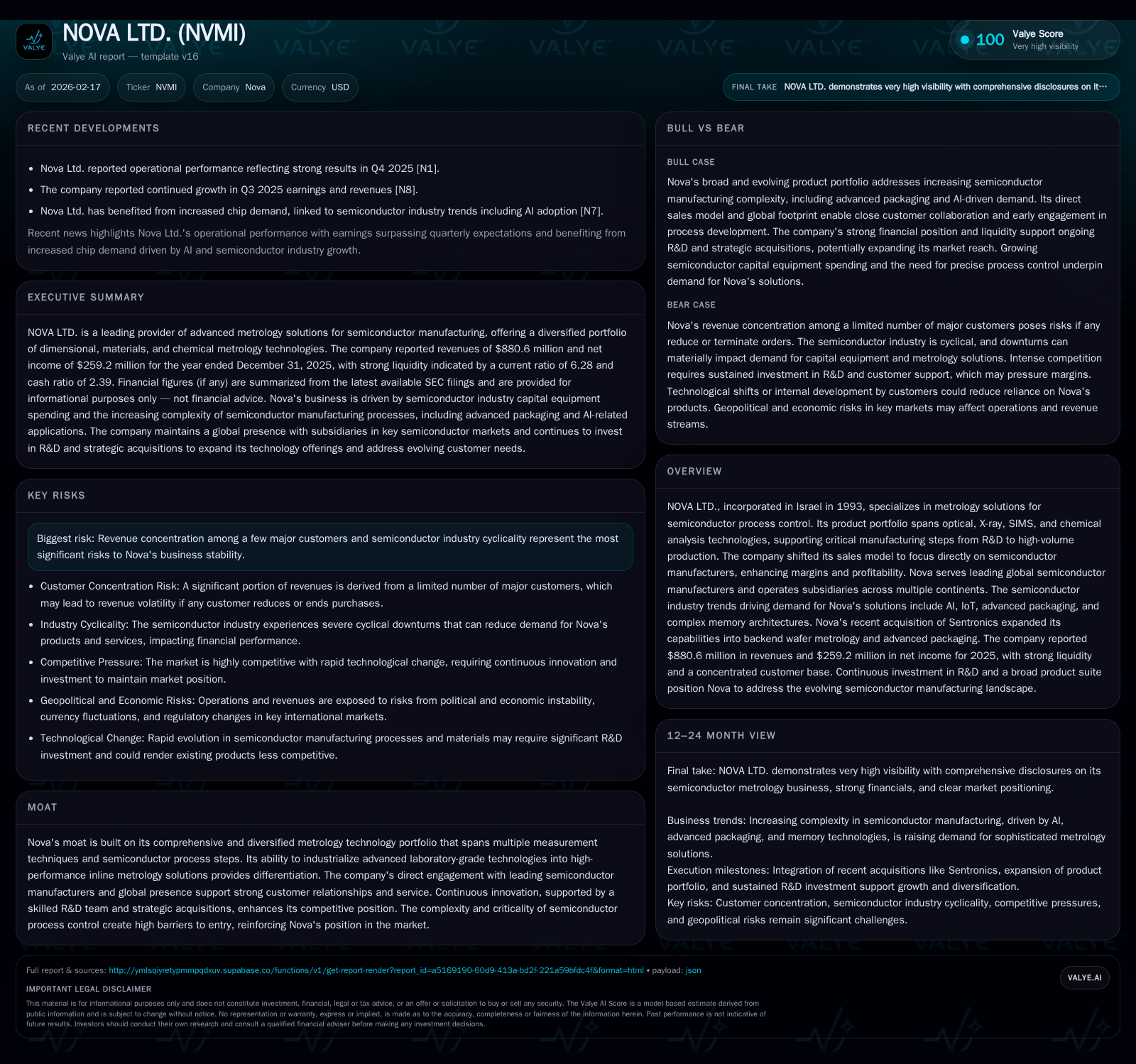

NOVA Ltd.'s Metrology Innovation and Market Expansion Drive Record 2025 Performance Amid Customer Concentration Risks

NOVA Ltd. delivered record revenue and profitability in 2025, underpinned by technology diversification and strategic acquisitions, while navigating semiconductor market cyclicality and customer concentration.

NOVA Ltd., an Israeli leader in semiconductor metrology solutions, recorded $880.6 million in revenues for 2025, a 31% increase year-over-year, supported by a broadening portfolio spanning optical, materials, and chemical metrology and enhanced by the Sentronics acquisition. Its direct sales approach to semiconductor manufacturers has improved margins significantly. The company is investing heavily in R&D to maintain technological leadership, aiming for $1 billion in revenue by 2027 amid growing demand driven by AI, advanced packaging, and complex memory technologies. However, significant revenue concentration among a few large customers and the cyclical nature of semiconductor capital spending remain material risks.

Company Background and Historical Performance

NOVA Ltd., established in Israel in 1993, is a key innovator providing advanced metrology solutions essential for semiconductor manufacturing process control. The company transitioned from selling primarily through process equipment manufacturers (PEMs) to direct sales to semiconductor manufacturers around 2008, significantly improving gross margins and profitability [S1][S27].

Between 2020 and 2025, NOVA achieved a compound annual growth rate (CAGR) of approximately 27.5% in product revenues, markedly outperforming the Process Control sector's estimated CAGR of about 16%, per Gartner forecasts [S10]. Revenues rebounded strongly from $517.9 million in FY2023 (following a dip linked to broader market softness) to $880.6 million in FY2025—a robust +31% year-over-year increase.

Net income surged even faster, rising from $136.3 million in FY2023 to $259.2 million in FY2025 (+41%), reflecting operational leverage benefits from scale and the higher-margin business model.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 881 | 259 | 246 | 253 | +31.0% | +41.1% |

| 2024 | 672 | 184 | 235 | 188 | +29.8% | +34.8% |

| 2023 | 518 | 136 | 124 | 132 | -9.3% | -2.8% |

| 2022 | 571 | 140 | 120 | 150 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex, Div. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 35 | 218 | 19.7 |

| 2024 | 30 | 218 | 19.8 |

| 2023 | 0 | 106 | 18.2 |

| 2022 | 21 | 98 | 23.9 |

Source: SEC companyfacts cache [F1].

Note: Dividend data is not available from the provided tags.

Gross margins remained stable near ~57-58%, despite shifts in product mix driven by evolving technology demands [S12]. Product sales accounted for approximately 80% of total revenues with services comprising about 20%, mainly from extended warranties and support contracts [S1][S18].

Operating cash flow was strong at $246 million (+4.4% YoY), supporting capital expenditures of $27.7 million (+61%) primarily for facilities upgrades and ERP system rollout [F1][S9]. Share repurchases totaled $35 million in FY25, underlining management's commitment to shareholder returns alongside reinvestment [F1].

Business Model and Product Portfolio

NOVA offers an integrated metrology technology suite covering dimensional (optical and X-ray), materials (thin films), SIMS (Secondary Ion Mass Spectrometry), and chemical analysis methods supporting semiconductor fabrication from R&D through high-volume production [S1][S27].

The company combines high-precision hardware with sophisticated software analytics that integrate physical modeling with machine learning enhancements—critical as device geometries shrink below nanoscale thresholds such as Gate-All-Around (GAA) transistors used in advanced logic nodes [S10][S16].

Key products include the Nova MARS physical/geometrical modeling suite coupled with Nova FIT machine learning solutions delivering comprehensive measurement platforms [S4]. Materials metrology throughput gains are enabled via server-based solutions working with proprietary instruments like VeraFlex.

Strategic acquisitions such as Sentronics GmbH (closed January 2025) expanded NOVA's capabilities into backend wafer-level packaging—an area of increasing importance amid chip heterogeneity—with modular dimensional metrology tools addressing specialty device measurements [S16].

Sales Strategy: Direct OEM Engagement & Geographic Reach

Pivoting away from PEM intermediaries like Applied Materials around a decade ago, NOVA now engages directly with leading semiconductor manufacturers throughout early process development through volume ramp phases, driving tighter integration and better margin capture [S1][S27].

The company operates subsidiaries globally—in Israel (headquarters), USA, Taiwan, South Korea, China, Japan, Singapore, Germany—providing localized sales engineering support and customer service worldwide [S1][S14]. Customers include major integrated device manufacturers (IDMs), foundries, and memory producers predominantly across Asia-Pacific (Taiwan, South Korea), the U.S., Japan, and Europe.

Top five customers contribute approximately half (~51%) of total revenues with individual contributions ranging between ~6–23%, highlighting material customer concentration risk typical for this capital equipment sector [S5][F1].

Industry Dynamics: Drivers & Risks

Rising complexity in semiconductor manufacturing driven by AI/IoT proliferation demands sophisticated multidimensional sensing at ever-smaller geometries—fueling demand for NOVA’s comprehensive metrology across Logic/Foundry advanced nodes (GAA), scaled DRAM/NAND memory architectures, and heterogeneous integration packaging schemes [S10][N5][N6]. This underpins NOVA’s recent strong growth.

However, inherent cyclicality in capital equipment spending introduces order timing volatility; downturns may pressure sales given long fab expansion lead times coupled with fixed R&D investments limiting cost flexibility [S11][S22].

Customer concentration exposes NOVA to risks if major clients alter purchasing strategies or face financial distress [S6][F1].

Geopolitical factors also elevate cybersecurity risks due to NOVA’s Israeli headquarters amid regional tensions; additionally regulatory compliance challenges arise from increasing AI governance frameworks impacting product development cycles [S11][S14][S21].

Competition includes established rivals such as KLA Corporation and Onto Innovation Inc., each heavily investing across complementary metrology technologies including CD/XRF/SEM techniques; sustained innovation blending hardware/software remains critical for leadership [S22][S23].

Capital Allocation & Financial Strength

As of FY25 end, NOVA holds a strong balance sheet with equity exceeding $1 billion supporting positive operating leverage trends; current ratio stands at approximately 6.28 reflecting liquidity combining $214 million cash against $224 million current liabilities [F1].

Capital expenditures rose to ~$28 million (+61%) reflecting facility investments plus new ERP system deployment launched January 2026 designed to improve operational efficiency despite initial adjustment challenges [S9][F1].

Research & development expenses remained stable at roughly $143 million or ~16% of revenues during FY24-25 periods showing continued focus on organic innovation including machine learning algorithm development layered onto physical models as well as integrating acquired technologies [S12][S16].

Share repurchases totaling $35 million underscore management confidence balanced against reinvestment needs; dividend payments are not disclosed indicating possible retention for growth or acquisitions [F1].

Future Growth Outlook & Milestones To Watch

NOVA targets achieving approximately $1 billion in revenue by calendar year 2027 through combined organic growth plus strategic acquisitions [N9][S17], driven by:

- Accelerated adoption across advanced Logic nodes (GAA transistor scaling), Memory (3D NAND), Packaging leveraging Sentronics backend metrology assets;

- Increasing integration of AI/ML enhanced software platforms paired with physical measurement for improved yield management;

- Broader geographic penetration especially within fast-growing Asian fabs;

- Continued investment expanding into emerging metrology domains addressing novel device architectures.

Challenges include maintaining technological leadership amid aggressive competitor activity; managing customer diversification to mitigate concentration risk; navigating macroeconomic headwinds marked by capital expenditure slowdowns affecting order timing; and operational stabilization following ERP rollout.

Monitoring quarterly order backlogs versus shipments will provide insight into demand sustainability post-record results.

Competitive Moat & Innovation Pathway

NOVA’s competitive advantage derives from its breadth across multiple measurement technologies—dimensional optical/X-ray methods plus unique materials and chemical characterization—all industrialized into inline metrology deployed globally at scale [S10][S27]. Coupling high-fidelity hardware with proprietary modeling software augmented by AI creates significant barriers given integration complexity.

Strategic acquisitions like Sentronics broaden addressable markets particularly tapping into the growing backend packaging processes vital for future heterogeneous systems beyond traditional node scaling [S16]. Collaborative research partnerships with major fabs reinforce long-term relationships enhancing defensibility.

Intellectual property protection remains crucial given ongoing litigation risks common within this capital equipment domain [S19].

Risk Summary

- Customer concentration (>50%) among top clients heightens revenue volatility;

- Semiconductor industry cyclicality causes order fluctuations impacting financial results;

- Elevated geopolitical/cybersecurity risks due to Israeli headquarters location amid regional conflicts;

- Regulatory pressures increasing due to evolving AI governance frameworks affecting software stacks;

- Intense competition necessitates sustained R&D investment (~16% revenues) influencing margin expansion potential.

Conclusion

NOVA Ltd.’s record fiscal year ending December 31, 2025 underscores its successful strategy diversifying technologies combined with direct customer engagement driving profitable growth [F1][S10]. Expansion into backend wafer-level packaging via acquisitions positions it well within evolving process control landscapes. Despite inherent risks from customer concentration and cyclical capital spending, its solid financial position supported by strong operating cash flows enables ongoing innovation investment alongside disciplined capital returns including share repurchases [F1]. Post-ERP operational stabilization alongside demand visibility will be key near-term indicators supporting sustained momentum. Its commitment integrating advanced analytics via machine learning atop robust physical measurement platforms fortifies its technology moat critical amid increasing fabrication complexities facing global semiconductor leaders.

This analysis synthesizes information from SEC filings dated February 17, 2026 (20-F) and related news sources without offering investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments