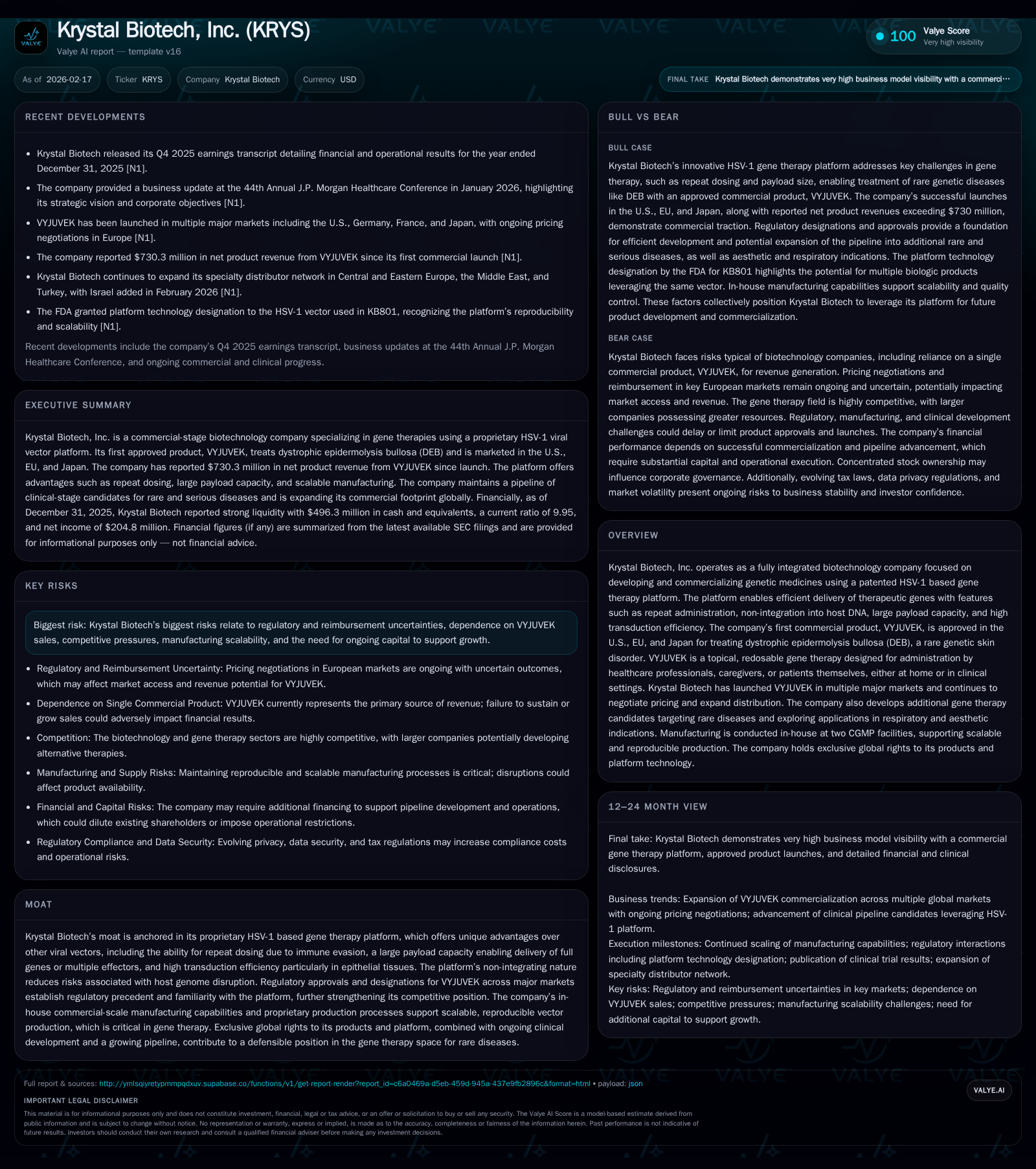

Krystal Biotech’s Financial Turnaround and Pipeline Expansion Signal New Era for Genetic Medicines

Krystal Biotech has shifted from multi-year losses to profitability driven by VYJUVEK’s commercial rollout and its differentiated HSV-1 gene therapy platform.

Krystal Biotech demonstrated a dramatic financial transformation in FY2025, leveraging its proprietary HSV-1 based gene therapy platform. The company’s first approved product, VYJUVEK, secured regulatory approvals and commercial launches in the U.S., EU, and Japan, fueling rapid growth in operating income, net income, and cash flow. While reimbursement negotiation and regulatory complexity remain key challenges, Krystal is actively expanding its pipeline into rare diseases and aesthetic indications through its platform versatility. Capital allocation reflects disciplined investment supporting scalable manufacturing with a solid ROE of nearly 17%. The near-term outlook hinges on further market access gains and clinical milestones.

Financial Transformation: From Historic Losses to Operating Profitability

Krystal Biotech’s fiscal trajectory over the last five years reveals a remarkable financial turnaround culminating in FY2025 profitability. After incurring substantial operating losses of approximately -$145 million in FY2021 and -$110 million in FY2023 [F1], the company swung to positive operating income of $66 million by FY2024 and then surged exponentially to $161 million by FY2025—a striking 145.5% year-over-year growth [F1]. Net income mirrored this trend with an almost 130% jump from $89 million in FY2024 to $205 million in FY2025. Operating cash flow also followed suit advancing from negative territory (-$101 million in FY2021) into strong positive cash generation totaling $201 million by FY2025.

Increasing cash conversion coincides with the commercialization ramp of VYJUVEK, suggesting solid leverage of product revenues despite absence of explicit revenue disclosure in XBRL tags. Capital expenditures rose modestly to $12 million in FY2025 from prior years but remain low relative to operating cash flows ensuring free cash flow (approximated at ~$189 million) supports ongoing investments without pressuring liquidity. Overall shareholder equity swelled to nearly $1.22 billion by FY2025 reinforcing balance sheet strength alongside a current ratio approaching 10, indicative of comfortable short-term financial flexibility [F1]. This progression positions Krystal well as it navigates growth scaling post-product launch.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 205 | 201 | 161 | 12 | +129.7% |

| 2024 | 89 | 123 | 66 | 4 | +715.6% |

| 2023 | 11 | -89 | -110 | 12 | |

| 2021 | -140 | -101 | -145 | 53 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 189 | 16.8 |

| 2024 | 119 | 9.4 |

| 2023 | -101 | 1.4 |

| 2021 | -154 | -26.8 |

Source: SEC companyfacts cache [F1].

Note: Revenue data unavailable from provided tags; YoY growth calculated where prior year data exists.

Proprietary HSV-1 Based Platform: Technical Advantages Shaping the Moat

Krystal’s cornerstone competitive advantage resides in its proprietary replication-defective herpes simplex virus type-1 (HSV-1) gene therapy platform. Unlike commonly used AAV vectors that confront neutralizing antibodies limiting redosing potential, Krystal’s HSV-1 vector exploits the natural immune-evasive properties of wild-type HSV-1 latency mechanisms while excising pro-inflammatory elements to minimize host immunogenicity [S1]. This unique repeat dosing capability directly addresses durability challenges endemic to viral gene delivery systems.

Moreover, the platform facilitates high transduction efficiency particularly targeting epithelial tissues—the relevant cell population for dermatological applications like dystrophic epidermolysis bullosa (DEB). Its large transgene payload capacity also enables delivery of full-length genes or multiplexed effectors not feasible with vectors constrained by size limitations such as AAV.

Importantly, Krystal’s vector is non-integrating which reduces genotoxicity risks associated with some integrating vectors thereby improving safety profiles critical for chronic or repeated administration regimens essential in skin diseases. Supporting commercial viability is Krystal’s two in-house CGMP manufacturing plants producing vector material at scale ensuring reproducible quality outputs critical for regulatory compliance and supply reliability [S1].

This combination of technical attributes constitutes a moat protecting Krystal against newer entrants constrained by immunogenicity or scalability issues while establishing a sustainable foundation for expanding indications.

Commercial Launch of VYJUVEK: Multi-Region Rollout and Market Penetration

VYJUVEK represents Krystal Biotech’s first approved product capitalizing on its HSV-1 platform. This topical redosable gene therapy received FDA approval in the U.S. in 2023 targeting dystrophic epidermolysis bullosa (DEB), followed by approvals within the European Union and Japan where launches commenced in 2025 [S1].

Commercialization leverages VYJUVEK’s distinct profile as an accessible topical treatment administered either by healthcare professionals or caregivers/patients themselves at home or clinical settings enhancing patient convenience—a differentiator compared to injectable gene therapies requiring specialized facilities.

While explicit sales data remain confidential per filings, earnings call commentary hints at encouraging initial demand trajectories supported by increasing commercial personnel deployments and distributor channel expansions across multiple major markets [N1]. Pricing negotiations continue across payors aiming for optimal market access amid generally evolving coverage frameworks detailed below.

Establishing baseline pricing benchmarks internationally remains challenging given high-cost gene therapy categorizations compounded by regional reimbursement disparities. Nonetheless, early traction indicates Krystal is building scale beyond initial U.S.-centric dynamics while also managing supply chain execution enabled by its internal manufacturing capabilities.

Regulatory Landscape and Reimbursement Challenges Across Key Geographies

Krystal faces multi-layered complexity navigating reimbursement pathways particularly due to the novel nature of redosable gene therapies targeting ultra-rare conditions such as DEB. In the U.S., Medicare, Medicaid managed care plans as well as private insurers demand rigorous demonstration of medical necessity coupled with pharmacoeconomic evidence substantiating cost-effectiveness compared to existing supportive care standards—necessitating costly health technology assessments (HTAs) that can extend timeline unpredictably .

European member states reflect fragmented HTA methodologies wherein securing meaningful reimbursement often requires country-specific dossier submissions encompassing comparative effectiveness studies often labeled a barrier for orphan therapies lacking large clinical datasets.

Japan additionally imposes unique price setting hurdles involving initial premium evaluations followed by biennial re-pricing reviews which may pressure margins absent continuous real-world outcome validations.

Beyond pricing parity risks, Krystal contends with extensive compliance mandates under anti-kickback statutes, false claims acts, physician payment transparency laws (e.g., Sunshine Act), privacy regimes including HIPAA/HITECH/CCPA/GDPR overlays across jurisdictions—all heightening legal operational burdens allocating resources toward governance rather than pure commercialization acceleration .

This dynamic underscores payer skepticism toward new technology premiums despite compelling unmet need incentivizing adoption—a tension requiring careful balancing through strategic stakeholder engagement.

Pipeline Development: Rare Disease Programs and Potential New Indications

Though VYJUVEK anchors current revenue streams, Krystal pursues an ambitious pipeline expansion leveraging its differentiated platform chemistry backing candidates across several indications characterized by rare genetic etiologies alongside opportunistic exploration into more prevalent pathologies.

Near-term clinical-stage projects target additional rare monogenetic disorders sharing dermatologic or ocular tissue tropisms benefiting from HSV-1 transduction efficiency and payload adaptability documented for skin-targeted therapeutics under patent protection extending through late decade [S1].

Simultaneously, Krystal strategically channels innovation into non-rare but commercially attractive domains such as non-small cell lung cancer (NSCLC), exploiting gene delivery vector properties for tumor microenvironment modulation—a frontier area poised for transformative impact if engendering durable responses.

Complementing these efforts is wholly owned Jeune Aesthetics subsidiary focused on cosmetic applications aiming at skin rejuvenation via gene-based mechanisms—a segment providing diversification beyond strictly life-threatening conditions with differing regulatory paths potentially expediting early revenues.

Research & development spend mirrors this broad scope underscoring balanced risk distribution with ongoing investment prioritizing candidates demonstrating strong translational rationale supported by preclinical models while maintaining momentum within core rare disease franchises [F1][N1].

Capital Deployment: Cash Flows, ROE, and Capital Expenditures Analysis

Krystal exhibits disciplined financial stewardship evidenced in elevated free cash flow generation approximating $189 million for FY2025 after modest capital expenditures totaling $12 million invested primarily toward scaling commercial manufacturing technologies supporting sustained product supply chain robustness amid growing demand [F1].

Equity financing rounds historically supplemented investment needs earlier during developmental phases but have receded in significance since FDA approval milestones reduced capital intensity relative to revenue inflows.

Based on reported net income of $205 million against total stockholders’ equity near $1.22 billion at year-end 2025 implies an approximate return on equity (ROE) of ~16.8%, reflecting efficient capital use even accounting for biotech sector inherent R&D expenditure volatility [F1].

No data on dividends or share repurchases are available from provided tags; accordingly no dividends or buybacks have been reported during this period consistent with typical biotechnology growth company practice emphasizing reinvestment over direct shareholder distributions pending deeper pipeline maturation cycles [F1].

Overall, Krystal appears positioned financially sound enabling continued strategic investments without external financing dependence under prevailing operating conditions.

Outlook and What Investors Should Monitor Next

Looking ahead based on recent earnings discussions and regulatory disclosures, key near-term catalysts include progression toward broader reimbursement coverage decisions notably across European national health systems where country-specific HTA outcomes will markedly influence overall uptake velocity [N1][S1].

Geographic expansion beyond primary markets into secondary regions with established regulatory pathways could incrementally lift top line provided logistical complexities are effectively managed.

Clinical milestones within the pipeline—particularly early-stage readouts validating safety/tolerability alongside preliminary efficacy signals—will critically inform longer-term valuation narratives concerning platform scalability beyond DEB indication.[N1]

Critical risk parameters remain regulatory environment evolution especially under shifting drug pricing reforms such as Medicare negotiation impacts alongside intellectual property litigation risks heightened by increasing competitor activity within the gene therapy domain.[S4–S8][S17]

Additionally, manufacturing scale-up achieving optimized vector yields retaining product consistency will demand sustained managerial focus given intrinsic biotech process variability challenges noted sector-wide.

In summary, while considerable headwinds around pricing/reimbursement exist typical for novel gene therapies targeting rare diseases, Krystal Biotech’s unique HSV-1 system combined with rising profitability offers a credible basis for growth contingent upon execution proficiency across commercialization infrastructure expansion coupled with successful pipeline development outcomes.

This analysis is based solely on publicly available information including company SEC filings ([F1],[S#]) and recent earnings transcripts ([N#]). It does not constitute investment advice or recommendations. Forward-looking statements referenced herein are subject to risks detailed in official disclosures which readers should review independently.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments