SSR Mining's Recovery Tradeoff Between Çöpler Suspension Costs and Hod Maden Development

SSR Mining's 2025 results highlight robust financial recovery despite operational setbacks and heavier capex deployment.

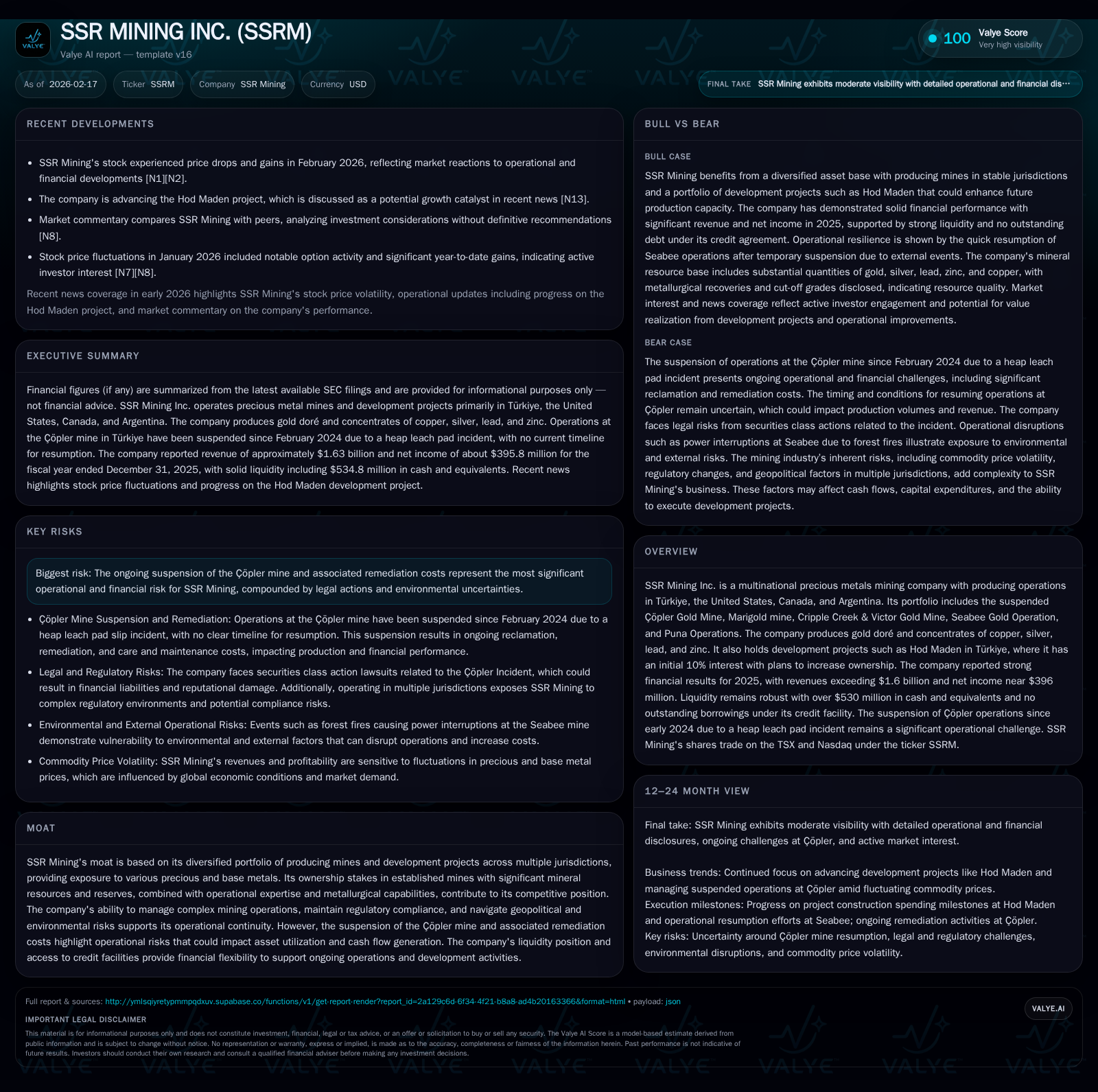

SSR Mining Inc. delivered a strong turnaround in 2025 with revenues of $1.63 billion and net income of nearly $396 million, rebounding from significant losses tied to the suspension of its Çöpler mine since early 2024. The company's diverse portfolio spanning Türkiye, the US, Canada, and Argentina partly insulated it from the operational halt at Çöpler. However, remediation costs and legal risks linked to the incident continue to pressure margins and capital allocation. Looking ahead, SSRM aims to grow through advancing the Hod Maden project in Türkiye with planned ownership increases contingent on development milestones. Financially, SSRM maintains robust liquidity with $535 million in cash and no outstanding credit facility borrowings, supporting upcoming structured payments for Hod Maden amid ongoing remediation expenses. Investors should monitor progress on the Çöpler remediation, regulatory outcomes, and milestone-driven investments at Hod Maden as key catalysts for future performance.

Historical Performance and Growth Drivers

SSR Mining experienced a pronounced financial recovery in FY2025 following two challenging years marked by operational setbacks primarily stemming from the suspension of its Çöpler Gold Mine in Türkiye. Revenue increased sharply by approximately 63.7% year-over-year [F1], climbing from about $996 million in 2024 to nearly $1.63 billion in 2025. This rebound was driven by elevated precious metal prices—48% higher realized gold prices and nearly a 46% increase in silver prices—as well as the strategic acquisition of the Cripple Creek & Victor (CC&V) mine completed early in 2025 [S24][S26]. These price dynamics combined with output growth excluding Çöpler cushioned overall revenue stability.

From a profitability standpoint, the company transitioned from a net loss of $261 million in 2024 to a net income of roughly $396 million in 2025 [F1]. Operating income similarly swung positive to $461 million compared to a loss of over $322 million prior year [F1]. This swing reflects both improved metal market conditions and normalization post-incident effects including business interruption insurance proceeds related to Çöpler [S16][S23].

Operating cash flow growth was especially notable: SSR generated approximately $472 million in CFO during 2025 versus only about $40 million in the prior year, marking an effective restoration of cash-generative capability [F1][S16]. The sharp rise enabled capital expenditures totaling $230 million (+60% YoY), focused on sustaining existing operations plus advancing new development projects including Hod Maden [F1][S23].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 1630 | 396 | 472 | 461 | +63.7% | +251.5% |

| 2024 | 996 | -261 | 40 | -322 | -30.2% | -166.6% |

| 2023 | 1427 | -98 | 422 | -130 | -150.5% | |

| 2022 | 194 | 161 | 190 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 0 | 0 | 242 |

| 2024 | 0 | 10 | -103 |

| 2023 | 58 | 56 | 198 |

| 2022 | 59 | 100 | 23 |

Source: SEC companyfacts cache [F1].

Dividends were suspended after 2023; buybacks ceased post-Çöpler incident.

Portfolio Composition and Operational Highlights

SSR Mining operates across four producing mines situated in different geopolitical regions: Marigold (USA), Cripple Creek & Victor (US), Seabee (Canada), Puna Operations (Argentina), alongside the suspended Çöpler mine (Türkiye). This diversification provides blended exposure to gold doré production complemented by copper, silver, lead, and zinc concentrates which help balance commodity cyclicality [S1].

The suspension of Çöpler, resulting from a heap leach pad incident reported in early 2024, remains SSR’s most significant operational hurdle impacting asset utilization and causing elevated remediation obligations estimated at approximately $172 million as of end-2025 [S1][S7]. The mine has been under care-and-maintenance protocols since suspension; costs related to ongoing remediation materially weigh on operating costs but are strategically managed alongside insurance recoveries.

In contrast, other mines sustained solid operational momentum during the period—evidenced by Marigold’s incremental revenue contributions and stable cost profiles [S21]. The acquisition of CC&V expanded SSR’s asset base adding resource life extensions pending permit amendments set to unlock additional value [S24][S26].

Future Growth Prospects: Hod Maden Project and Beyond

A key strategic growth catalyst lies with SSR's investment in the Hod Maden project located in Türkiye, where it currently holds an initial 10% stake with contractual rights aimed at increasing ownership up to 40%, contingent upon structured milestone payments linked primarily to construction spending thresholds [S4][N13]. This project targets precious metals extraction using advanced processing techniques optimized for low-sulfur sulfide ores characteristic of the area.

The upfront payment totaling approximately $120 million is phased with additional payments amounting to about $30 million scheduled within one year following commercial production onset; furthermore, contingent cash outlays up to an estimated $84 million hinge upon delineation success exceeding current mineral reserve estimates by half a million gold equivalent ounces [S4]. These stipulated payments present clear capital allocation tradeoffs as management balances near-term financial flexibility with longer-term production scaling aims.

Completion timelines and regulatory clearances around Hod Maden will be critical liquidity milestones alongside actual ramp-up outcomes that will materially influence SSR’s growth trajectory beyond its base portfolio.

Capital Structure, Liquidity Profile, and Returns

SSR Mining exhibits a robust liquidity position highlighted by cash and cash equivalents standing at approximately $535 million as of December 31, 2025—a substantial increase compared to prior periods driven by improved operating cash flows coupled with conservative financing policies [F1]. Notably, there were no outstanding borrowings against its Second Amended Credit Agreement at year-end while maintaining nearly $400 million undrawn facility capacity offering an ample buffer for working capital needs or opportunistic investments.

Capital allocation during the year favored reinvestment into property plant & equipment with capex rising about 60% YoY emphasizing expansionary projects plus acquisitions (notably CC&V for ~$100 million upfront payment) [F1][S23][S24]. The company did not pay dividends during either fiscal year 2024 or 2025 reflecting a prudent stance given ongoing uncertainty surrounding remediation efforts at Çöpler and developmental funding requirements for Hod Maden [F1]. Similarly, share repurchases paused following these events diverging from historically active buyback programs conducted earlier.

Approximate return on equity calculated from reported FY25 net income over shareholders’ equity suggests an ROE near 11%, signaling improved capital efficiency relative to preceding years when litigation provisions and impairment charges weighed heavily on returns [F1]. Free cash flow yield was positive at roughly $242 million derived from operating cash flow less capital expenditures indicating healthy internal generation capability despite heightened investment activity.

Risks: Incident Fallout and Legal Challenges

Although SSR Mining returned strongly financially for fiscal year ending December 31, 2025, unresolved risks associated with the Çöpler suspension continue imposing constraints on asset utilization and earnings visibility . The closure was triggered by an environmental safety event involving the heap leach pad triggering substantial remediation costs plus reputational damage.

Furthermore, multiple securities class actions remain active against SSR alleging misstatements regarding operation safety controls around Çöpler prior to incident disclosures—litigation carries legal expense uncertainties along with potential indemnity exposures [S7][S9]. Regulatory compliance challenges spanning multi-jurisdictional operational footprints require ongoing vigilance given complex permitting environments especially relating to future project developments like Hod Maden.

Environmental reclamation accounting embodies inherent estimation uncertainty affecting liabilities recognized due to changes in regulations or technological requirements potentially impacting reported results or capital allocations going forward [S17].

Analysis: Operational Leverage Amid Commodity Cycles

SSR’s diversified geographic footprint partially mitigates single-mine dependency risk but also complicates capital deployment strategies balancing maintenance capex across mature assets versus funding new builds under tight timelines such as Hod Maden expansion.

Metallurgical recovery variability—especially noted between oxide grind leach ores (53%-90%) versus sulfide ores (81%-91%) at Çöpler—also influences unit cost control capabilities once operations resume fully; this complexity underscores ongoing operational leverage sensitivity within their portfolio [S1]. Moreover, inflationary pressures embedded within global mining supply chains heighten cost risk particularly sustaining capital expenditures.

The demonstrated capacity for rapid improvement in operating cash flow reflects strong market-driven leverage but reliance on stable commodity pricing remains essential underlying variable exposing earnings variability often seen across mid-tier precious mining peers.

What To Watch

- Timelines governing resolution or restart prospects at Çöpler mine including remediation progress updates.

- Milestone achievements linked to Hod Maden ownership increments particularly construction spend completion reports.

- Any substantive developments related to securities litigation outcomes which could affect financial contingencies.

- Regulatory approvals or setbacks for resource permit modifications at CC&V enabling life extension opportunities.

- Commodity price trends influencing realized gold/silver prices that materially impact margins given product mix exposure.

- Management commentary during next quarterly earnings releases focusing on balance sheet strategies regarding debt usage or equity changes.

Disclaimer

This report is intended solely for informational purposes without offering investment advice or recommendations concerning SSR Mining Inc.’s securities or business prospects. All factual data is sourced from regulatory filings including SSR's recent annual report (Form 10-K), quarterly reports (Form 10-Q), press releases, as well as public news reports referenced accordingly. Readers should conduct independent due diligence before making any decisions related to SSR Mining or its industry environment.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments