Neuphoria Therapeutics Advances CNS Ion Channel Modulation with BNC210 amid Capital Intensity

Neuphoria focuses on novel α7 nicotinic receptor modulators addressing underserved neuropsychiatric disorders, with evolving clinical pipelines and strategic partnerships.

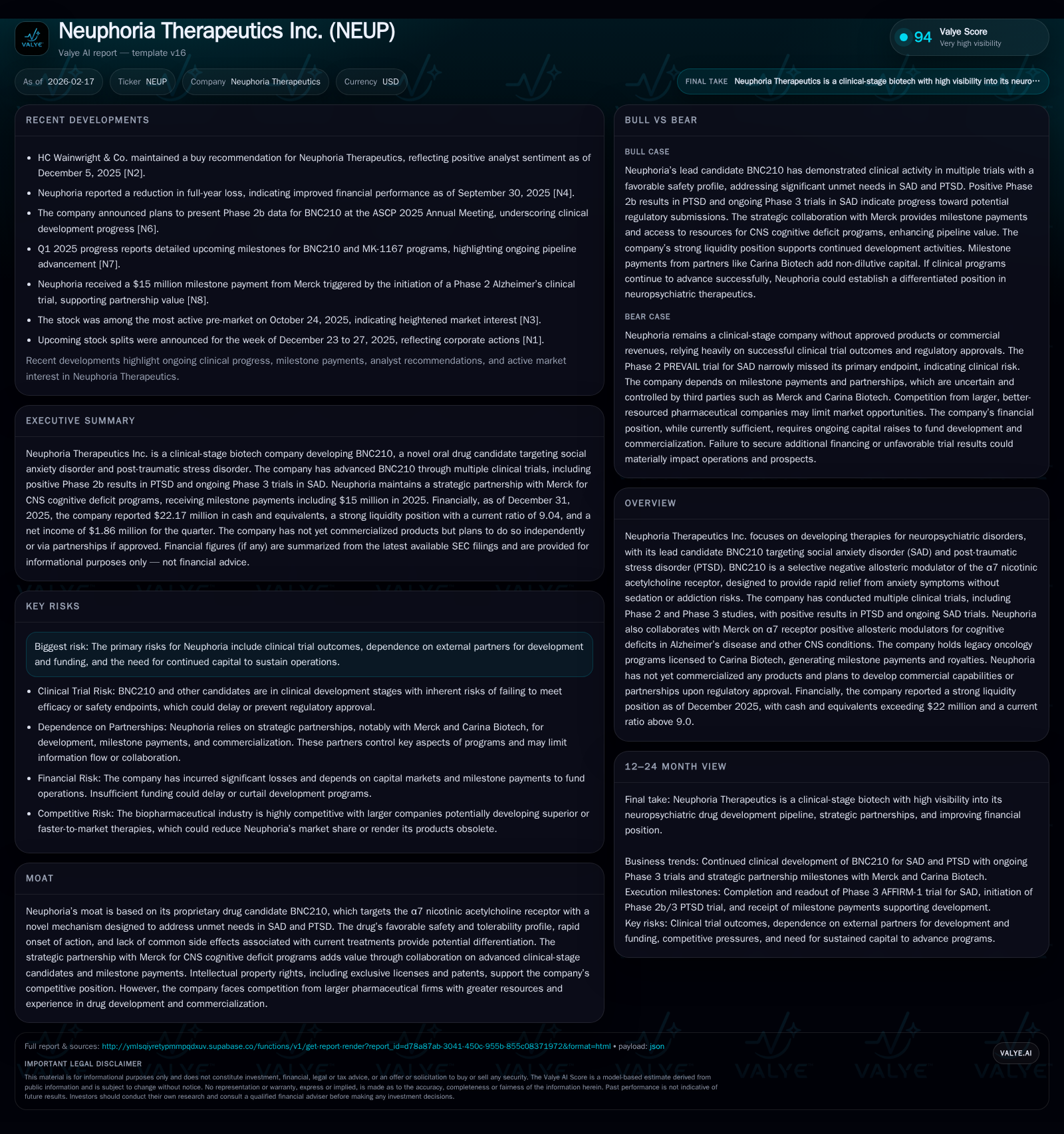

Neuphoria Therapeutics Inc. is a clinical-stage biopharmaceutical company pioneering therapies targeting the α7 nicotinic acetylcholine receptor to treat neuropsychiatric conditions such as social anxiety disorder (SAD) and post-traumatic stress disorder (PTSD). Despite recent setbacks, its lead candidate BNC210 shows promise for rapid relief without sedation or addiction risks. Collaborations with Merck on complementary positive allosteric modulators enhance its pipeline breadth, while legacy oncology licenses provide ancillary revenue streams. The company's financial profile reflects ongoing developmental expenditure with improving cash flow dynamics but necessitates continued capital infusion to sustain operations amid milestone-driven revenue potential. Return metrics such as ROE remain negative, and no dividends or buybacks have been declared, consistent with its clinical-stage status.

Company Overview and Intellectual Property

Neuphoria Therapeutics Inc. operates at the intersection of neuroscience and pharmacology focusing on allosteric modulation of ion channels critical to central nervous system (CNS) function. The company's lead candidate BNC210 is a selective negative allosteric modulator (NAM) of the α7 nicotinic acetylcholine receptor — a target implicated in regulation of emotion and cognitive pathways relevant to anxiety spectrum disorders such as social anxiety disorder (SAD) and post-traumatic stress disorder (PTSD). This modality aims to provide rapid symptom relief without the sedation or addiction liabilities seen with benzodiazepines or slower antidepressants [S1].

Beyond its proprietary NAM program, Neuphoria maintains a strategic alliance with Merck & Co., granting the latter exclusive rights within North America for positive allosteric modulators (PAMs) targeting cognitive deficits primarily in Alzheimer's disease. These assets supplement Neuphoria's pipeline diversification into broader CNS indications [S1,S11]. Concurrently, the company’s legacy oncology portfolio—licensed out to Carina Biotech—provides milestone-triggered payments and low-mid single digit royalties, helping offset some R&D expenditures [S20,S21].

Historical Performance: Growth Trajectory & Financial Context

Historically, Neuphoria's growth has been dominated not by product revenues but by milestone payments from collaborative partners and government grants supporting R&D activity. Its revenue base remains small; reported revenue for FY2023 was AUD 22k—a stark decline from AUD 264k in FY2022—primarily reflecting variability in milestone recognition timing given the nature of license agreements [F1].

The company endured substantial operating losses during recent years: -$17.9 million in FY2024 improving significantly to approximately -$1.1 million during the first half of FY2025 according to recent filings [F1]. Net losses also contracted sharply from -$15.5 million in FY2024 to near breakeven (-$0.4 million) by June 2025, underscoring efforts at cost containment alongside incremental milestone inflows [F1]. Operating cash flow similarly turned positive ($77k) from negative (-$14.7 million), indicating better liquidity management possibly reflecting receipt of Merck milestone payments (notably $15 million payment in March 2025) [S12,F1].

Financial data summary:

Historical performance (annual)

| FY | Rev ($) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 0 | 0 | -1 | +97.6% | ||

| 2024 | -15 | -15 | -18 | |||

| 2023 | 22047 | -91.6% | ||||

| 2022 | 263634 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex, Div, Buybacks, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -1.9 |

| 2024 | -88.6 |

| 2023 | |

| 2022 |

Source: SEC companyfacts cache [F1].

*Note: Operating income/net income data for FY2025 available only through June 30; Current ratio computed as current assets divided by current liabilities as of December 31, 2025.

Metrics such as capital expenditures, dividends paid, or share buybacks are not disclosed or available from the provided XBRL data or SEC filings.

Pipeline Development and Clinical Progress

BNC210 remains the centerpiece of Neuphoria's therapeutic ambitions. It embodies a first-in-class approach for acute "as-needed" treatment of SAD complemented by chronic PTSD therapy opportunities. The Phase 2 PREVAIL trial yielded encouraging trends despite missing its primary endpoint; this led to constructive interactions with FDA culminating in Phase 3 trial initiation (AFFIRM-1), enrolling approximately 332 patients across U.S. sites for rigorous confirmation of efficacy/safety profiles [S1]. Carefully designed post-hoc analyses influenced Phase 3 protocols emphasizing more sensitive symptom measures.

The partnership with Merck facilitates advancement of PAM candidates aimed at cognitive dysfunction linked to Alzheimer's disease—programs where mechanism-based synergy potentially complements BNC210’s focus on emotional regulation channels [S11,S12]. However, Merck retains control over these developments including commercialization decisions; Neuphoria’s financial participation depends heavily on triggered milestones and royalties tied to commercial success.

Preclinical programs focused on Kv3.1/3.2 ion channel modulation represent earlier-stage bets aiming at broader CNS indications characterized by high unmet need though their commercial timelines remain uncertain [S1].

Growth Catalysts & Constraints

Potential growth drivers include successful late-stage trial results for BNC210 securing regulatory approvals followed by market launch addressing a sizeable patient population exceeding 27 million SAD/PTSD cases in the U.S. alone [S1]. Incremental validation from Merck’s clinical progression could unlock substantial milestone revenue capped at approximately $450 million plus royalties under existing contracts [S11]. Milestone payments from oncology licensing also contribute intermittently.

Conversely, significant barriers persist such as:

- Risk intrinsic to clinical trial outcomes including potential efficacy shortfalls or safety flags given CNS drug development complexity.

- Dependence on external partners like Merck for critical program advancement reduces visibility over timelines and resource allocation.

- Regulatory complexities especially regarding coverage/reimbursement given ongoing shifts in U.S. healthcare policies impacting drug pricing paradigms [S4–S16].

- Ongoing capital requirements remain substantial given scale-up costs needed for commercialization preparation alongside sustained R&D investment.

Financial Outlook & Milestones To Watch

Explicit forward guidance is absent per reported sources; key upcoming events include:

- Interim/final results from AFFIRM-1 registrational Phase 3 trial.

- Data disclosures related to Merck’s PAM programs which can materially influence royalty/milestone prospects.

- Additional licensing milestones from Carina Biotech if oncology assets progress toward Phase 3 triggers unlocking ~$75M+ potential payments.

Investor attention should focus on quarterly updates detailing cash burn rates against realized payments plus any announcements indicating changes in development pace or financing actions.

Capital Structure & Returns Considerations

With an accumulated deficit exceeding $178 million as of June 30, 2025 [S19], Neuphoria remains unprofitable but shows stabilizing financial health evidenced by cash holdings around $22 million versus relatively low immediate liabilities (~$2.6 million), yielding an exceptionally strong current ratio (>9x), indicative of short-term solvency adequacy under current obligations [F1]. Management anticipates cash resources sufficing into mid-2027 barring unforeseen accelerations in capital needs or adverse events [S27].

No dividends or share repurchases have been declared or signaled; reinvestment prioritizes advancing pipeline development and regulatory compliance costs associated with becoming a U.S.-listed entity post-ASX delisting in August 2023 [S1,S17,S28]. Return metrics like ROE remain negative at approximately -1.9%, reflecting its development-stage financial profile rather than commercial profitability [F1].

Sector Contextualization & Intellectual Property Landscape Analysis

Within neuropsychiatric therapeutics focused on ion channel modulation, competition emerges not solely via direct drug mechanisms but also through therapeutic classes spanning antidepressants, benzodiazepines—and emerging digital therapeutics frameworks attempting adjunctive roles. Neuphoria’s unique NAM approach targeting α7 nicotinic receptors aligns well with growing neuroscience insights disfavoring sedative/anxiolytics’ side effect burdens.

Intellectual property surrounding BNC210 provides defensibility against generic encroachment with exclusivity periods bolstered further through molecular innovation patents licensed exclusively by Neuphoria internally or via Merck collaboration expansions [S9,S14]. However, competing pharmaceutical incumbents possess advantages rooted in scale manufacturing experience and global commercialization networks.

Risks Summary

Key risk vectors include:

- Clinical trial uncertainty encompassing unexpected adverse effects or failures delaying approval timelines.

- Financing risk tied to capital-intensive late-stage development given historical losses prior to recent improvements.[S19]

- Dependence on milestones exacerbates volatility in reported earnings and investor sentiment.

- Regulatory risk spans both pre-market approval complexity potentially necessitating additional studies plus post-marketing surveillance constraints impacting product usage controls.

- Pricing/payer pressures from evolving U.S. healthcare reforms coupled with multi-jurisdictional coverage variability introduce commercialization unpredictability.

Conclusion & Monitoring Points

Neuphoria Therapeutics presents an archetypical biotech developmental narrative: leveraging cutting-edge mechanistic science addressing large unmet neuropsychiatric markets but balanced by clinical execution risk and capital requirement burdens inherent until commercialization commences. Stakeholders keenly await definitive Phase 3 SAD data from AFFIRM-1 alongside ongoing collaborations with Merck that may validate extended CNS portfolio value propositions beyond anxiety/stress indications.

Cash runway appears secured through mid-2027 providing breathing room for pivotal developments while operational efficiencies marginally improved recently suggest prudent resource stewardship amid scaling infrastructure demands related to NASDAQ listing compliance and U.S.-centric study conduction.

Monitoring quarterly filings for updated clinical progress indicators combined with milestone recognition remains critical due diligence moving forward.

This report is based solely on publicly available information as cited herein without any forward-looking investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments