Motorola Solutions: Navigating Record 2025 Performance Amid Financial and Contractual Complexities

A deep dive into MSI's benchmark 2025 financials, multifaceted business model, and strategic positioning within a challenging tech environment.

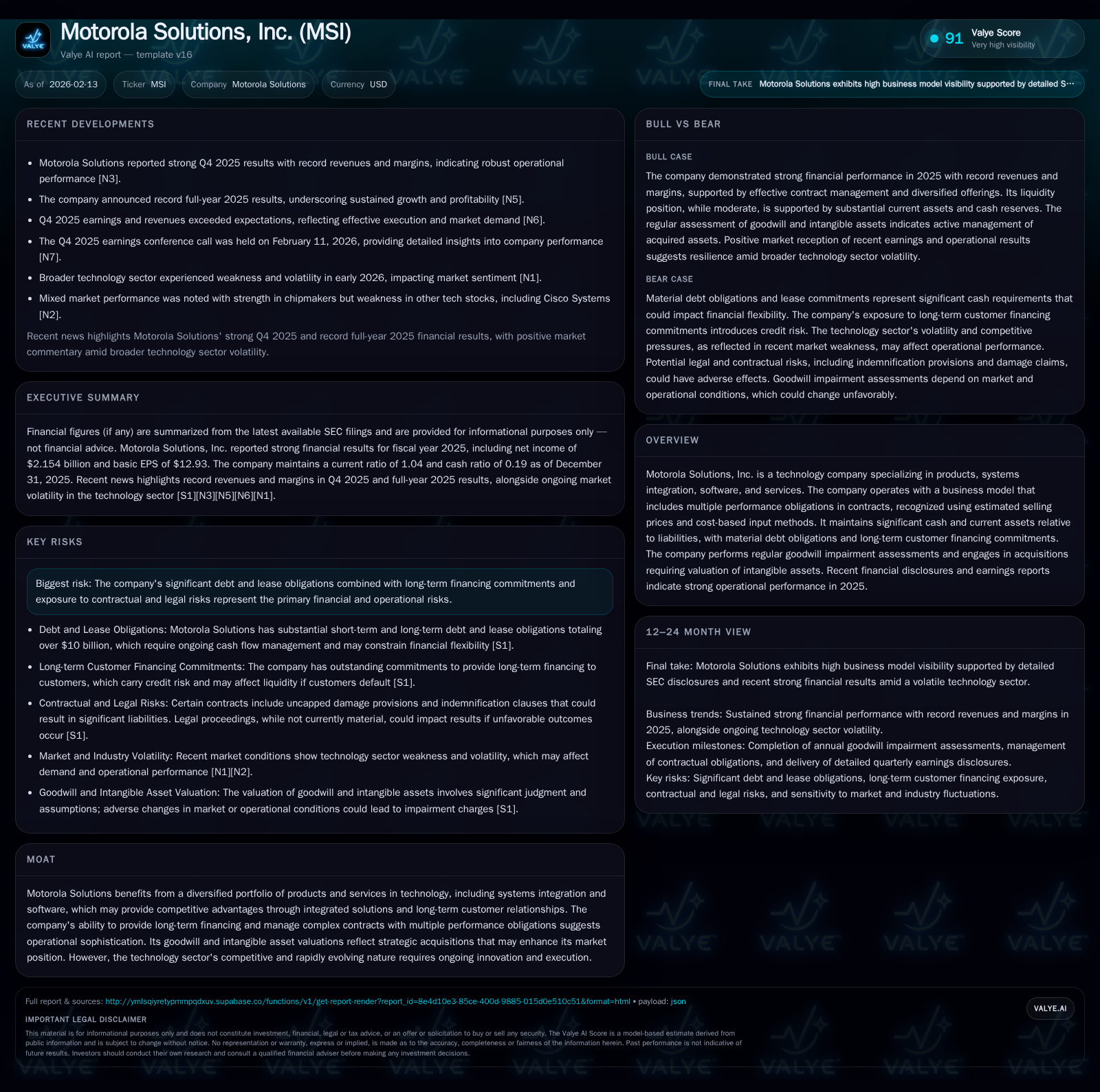

Motorola Solutions capped 2025 with record revenues and net income, fueled by integrated products and software services that underpin its competitive moat. The firm's complex contract structures and multiple performance obligations showcase operational sophistication but introduce nuanced risks. Despite robust liquidity, MSI carries significant long-term debt and contractual commitments that require vigilant balancing. Industry headwinds from tech sector volatility and evolving investor sentiment pose external pressures, while strategic acquisitions continue carving out valuable intangible assets. Forward growth depends on sustained innovation and disciplined financial management amid a dynamic landscape.

Record-Breaking 2025: Digging Into The Numbers

Motorola Solutions closed 2025 with headline-grabbing financials that exceeded Wall Street expectations. Full-year net income reached an impressive $2.15 billion supported by strong top-line performance and expanded operating margins as reported in their February release [N1][N3][F1]. Q4 alone continued this streak with revenues surpassing estimates accompanied by margin enhancements indicative of operational leverage [N4][N2]. The company’s ability to deliver consecutive quarters of growth amidst a turbulent tech landscape underscores its effective execution.

Dissecting the numbers reveals how MSI’s deeply integrated product and service offerings leverage synergies to drive both scale and profitability. Quarterly earnings transcripts highlight management's disciplined cost controls alongside targeted investments in growth arenas [N2]. The company’s fiscal discipline paired with dynamic customer engagement strategies anchors its strong earnings momentum.

Multipronged Business Model: Integration and Innovation

A central pillar of MSI’s success is its business model spanning multiple technology facets: from hardware communications devices to sophisticated software suites and systems integration complemented by pervasive service offerings [valye_report_excerpt][S1]. This ecosystem fosters sticky client relationships through long-term contracts embedding several performance obligations.

Revenue recognition here demands accounting finesse. Employing estimated selling prices alongside cost-based input methods reflects the complexity in assigning fair value across bundled deliverables [S1]. Such approaches can stabilize revenue streams over time but add layers of analytical rigor to quarterly results. Moreover, delivering integrated solutions supports differentiation enabling MSI to compete beyond commoditized hardware segments.

Long-term financing options offered to customers further entrench these relationships by aligning capital deployment strategies tailored to client needs [valye_report_excerpt]. This multipronged approach not only diversifies sources of income but also positions MSI competitively against peers emphasizing single-product lines.

Evaluating Financial Health: Cash, Debt, and Obligations

MSI exhibits a balanced liquidity profile heading into 2026 with cash reserves exceeding $1.16 billion juxtaposed against current assets measuring approximately $6.3 billion relative to current liabilities near $6.08 billion — establishing a current ratio around 1.04 which signals adequate short-term coverage [F1][S1].

However, beneath this surface lies significant leverage: the company holds over $8 billion in gross long-term debt obligations plus more than $670 million combined lease liabilities (short- and long-term), complemented by sizeable purchase commitments totaling over $770 million across periods [S1].

Management openly discloses efforts to rationalize real estate footprints aiming to reduce perpetual leasing costs while preserving operational flexibility — a move reflecting prudent capital stewardship amid a shifting office environment [S1]. Access to capital markets remains critical given these obligations; any restriction could heighten refinancing risks or cost of capital spikes in adverse conditions.

The interplay between robust cash flow generation from operations against structural cash outflows frames an ongoing balancing act central to sustaining growth without compromising financial flexibility.

Strategic Acquisitions: Building Intangibles and Moat

MSI’s strategic acquisition activity fuels growth by enhancing their portfolio capabilities especially in software-centric domains where barriers to entry are higher [valye_report_excerpt][S1]. Each transaction entails valuation of tangible versus intangible components with resultant goodwill forming a substantial asset base requiring frequent impairment testing.

Intangible assets often include acquired technology patents, customer relationships, trademarks, and development pipelines with amortization horizons extending up to two decades or more depending on asset type [S2]. The repeated affirmations of goodwill health in filings suggest management confidence; nevertheless, sector dynamism means constant vigilance is necessary.

This expanded intangible footprint helps solidify MSI's moat by embedding newer technologies aligned to evolving market demands including public safety communications — a segment demanding high reliability and regulatory compliance.

Operational Risks in a Complex Contract Landscape

The company faces contractual risks atypical for many technology firms due to provisions allowing for potential damages exceeding contract revenue — albeit rare — introducing outsized exposure if disputes arise [S1]. Such uncapped damages clauses mandate stringent performance oversight given the financial consequences.

Furthermore, indemnification responsibilities tied particularly to intellectual property rights signal growing legal pressures as patent litigations amplify across the tech ecosystem [S1]. While historically claims have been manageable, heightened IP indemnity risk calls for refined legal risk management frameworks.

Additionally, long-term customer financing commitments show an increase from $105 million at end-2024 to $179 million at end-2025 [S1], reflecting possibly greater reliance on structured sales arrangements that may impact liquidity timing or credit risk profiles.

Collectively these factors illustrate the nuanced contractual landscape MSI navigates requiring sophisticated governance beyond mere product delivery.

Comparing Value Options: Motorola Solutions vs. Competitors

Within the communications technology sector, peer valuation remains a spirited debate with recent analysis contrasting MSI against giants such as Ericsson [N14]. MSI’s sustained operational strength shown in record earnings forms a compelling case although macro factors pressure sector valuations broadly.

Recent headlines underscore divergent market reception where MSIs fundamentals shine despite sector volatility driven by tech macro fears including AI-related disruptions [N11][N12][N13]. Compared to Ericsson's exposure notably in telecom infrastructure segments facing cyclical challenges, MSI’s diversified portfolio encompassing public safety offers defensive characteristics but less explosive growth potential.

These dynamics position MSI within a mid-growth mid-defensive quadrant of investment consideration frameworks emphasizing quality earnings coupled with manageable risk profiles rather than high-beta growth plays.

Market Sentiments & Tech Sector Pressures

Investor psychology around broad technology stocks has soured lately under waves of AI hype intersecting with concerns about overspending and regulatory scrutiny [N11][N12][N13]. Stocks broadly plunged despite some pockets of strength such as chipmakers; companies like Cisco experienced mixed reactions underscoring uneven narrative flows.

In this context MSI represents an interesting outlier—its disciplined execution contrasts with the speculative enthusiasm tempering overall sector appetite. Yet sentiment drags can obscure fundamental strengths temporarily compelling nuanced risk assessments factoring both intrinsic value signals as well as systemic risk overlays.

Forward-Looking Perspectives: Sustainability of Growth

Looking ahead, sustaining MSI’s robust trajectory demands relentless innovation particularly as competitors vie aggressively in software-enabled service domains [valye_report_excerpt][N7][N8]. Contractual execution agility also remains paramount given the layered obligations complexity highlighted earlier.

Analyst discourse increasingly shifts toward indicators beyond headline revenue or EPS focusing on backlog visibility, margin sustainability under inflationary pressures, and capital allocation efficiency [N7]. Balancing organic growth alongside acquisition integration will test management acumen while preserving cash flow strength essential for debt servicing.

Ultimately MSI’s ability to maintain its differentiated moat hinges on toolkits blending product evolution with flexible financing solutions all deployed within fiscally responsible frameworks accommodating sector cyclicality yet capitalizing on public safety market momentum.

Disclaimer: This analysis is provided for informational purposes only and does not constitute investment advice or recommendations. Readers should conduct their own due diligence before making any financial decisions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments