Broadway Financial Corp DE: Navigating Profitability Amid a Bold Social Mission

Broadway Financial Corporation pursues equitable economic development through mission-driven banking despite ongoing financial headwinds.

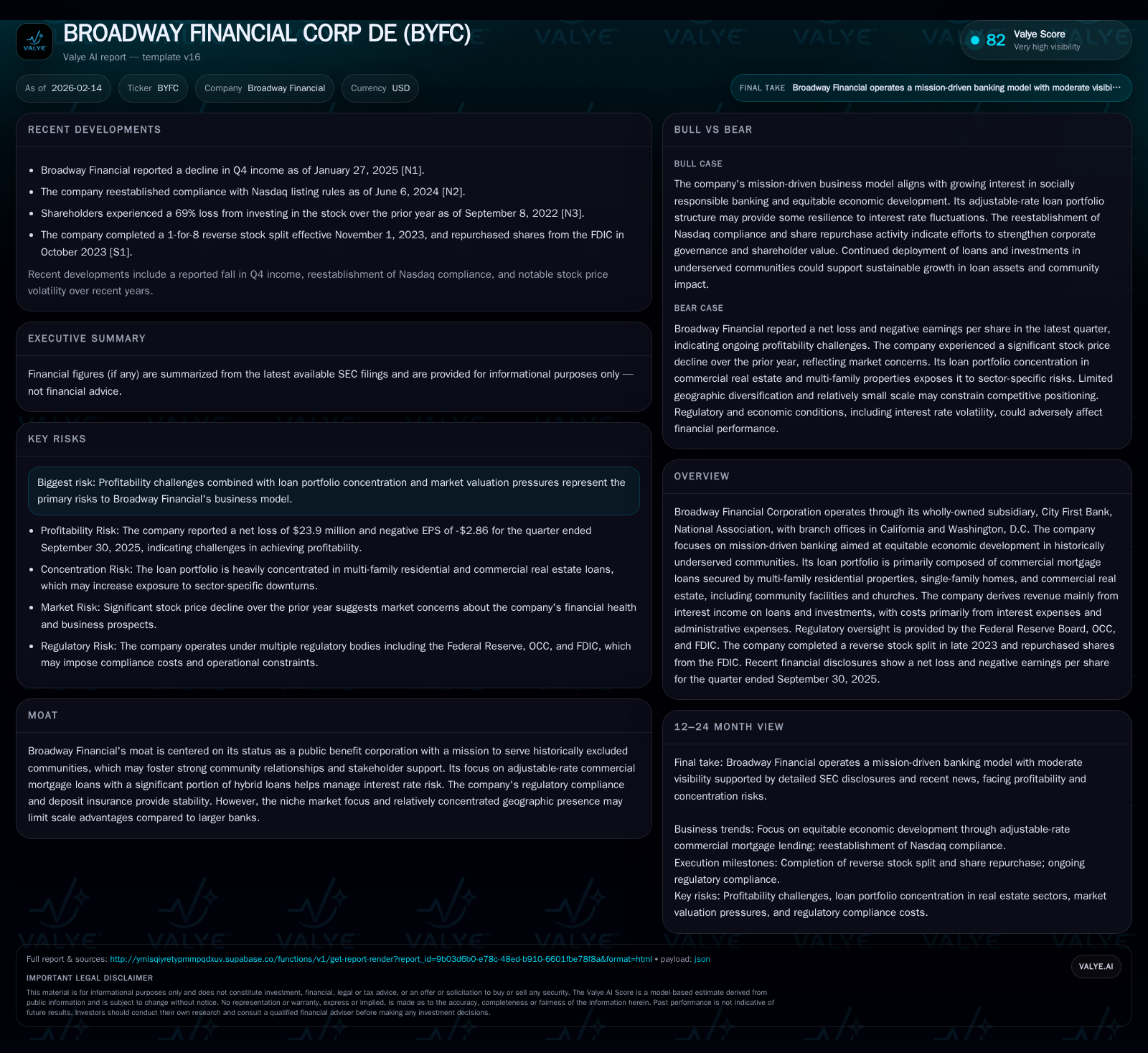

Broadway Financial Corporation, a Delaware public benefit corporation operating City First Bank, focuses on serving historically underserved communities through targeted real estate lending in Southern California and Washington, D.C. While its social mission creates strong community ties, the company faces significant profitability challenges amid a concentrated loan portfolio and macroeconomic uncertainties including inflation and rising interest rates. Recent strategic moves such as a reverse stock split and share repurchase from the FDIC aim to stabilize capital structure. The company’s long-term success will hinge on balancing its social impact objectives with competitive pressures and evolving regulatory demands.

A Mission Beyond Banking: The Public Benefit Model

Broadway Financial Corp DE occupies a unique niche within the banking sector as a Delaware public benefit corporation wholly owning City First Bank. This status transcends traditional profit-maximization motives by embedding a social mission aimed at driving equitable economic development within historically excluded communities. The bank's operational footprint—focused primarily in Southern California and the Washington D.C. metropolitan area—underscores this targeted approach. Broadway views capital deployment into multi-family residential projects, affordable housing initiatives, commercial real estate serving community needs, and even places of worship not just as financial transactions but as instruments of societal enhancement. This orientation fosters strong community ties that act as both a moat and an obligation. However, this dedication simultaneously confines scalability opportunities when compared to regional or national financial institutions with broader market penetration [S1], [valye_report_excerpt].

The Strategic Transformation: Mergers and Identity Shifts

In April 2021, Broadway Financial completed its merger with CFBanc Corporation—a move which culminated in the rebranding of its bank subsidiary to City First Bank, National Association. This consolidation was more than cosmetic; it crystallized Broadway's commitment to formalizing its stakeholder-centric mission through conversion to a Delaware public benefit corporation simultaneously with the merger. Consequently, governance frameworks are attuned toward creating social, economic, and environmental value alongside financial returns. The deliberate choice of operating under this legal structure aligns organizational purpose with operational reality—a pattern uncommon among publicly traded banking institutions.

In October 2023, Broadway executed a reverse stock split at a ratio of one-for-eight shares affecting all classes of common stock. This structural adjustment was designed to enhance per-share price metrics amid market pressures while streamlining shareholder composition. Concurrently, the Company repurchased nearly 245 thousand voting shares from the FDIC—shares initially acquired when the FDIC took control over First Republic Bank following its collapse earlier that year. This repurchase represented just under 4% of total voting shares prior to execution and helped consolidate shareholder power aligned with strategic goals [S1].

Portfolio Structure: Risks and Opportunities in Real Estate Lending

A defining characteristic of Broadway's asset base is its pronounced exposure to commercial mortgage loans secured by multiple forms of real estate collateral—primarily multifamily residential properties but also single-family homes, community facilities like churches, and other commercial spaces. These assets are geographically concentrated in Southern California and Washington D.C., both regions with distinctive economic profiles but also sensitive to localized market dynamics.

This concentration heightens vulnerability should adverse real estate trends emerge in these metropolitan areas. Declines in property valuations would erode collateral buffers underpinning loans while rising vacancies could diminish borrower cash flow stability. In turn, this scenario would likely increase delinquencies or defaults impacting nonperforming asset levels adversely—risking material capitalization strain [S1], [valye_report_excerpt].

Nonetheless, the bank’s focused lending provides opportunities for deep community engagement and relationship management uncommon among larger lenders more diffused across geographies.

Navigating an Inflationary and Interest Rate Heavy Environment

The macroeconomic backdrop presents formidable challenges for Broadway Financial’s operations. Elevated inflation that persisted into recent years triggered aggressive interest rate hikes by the Federal Reserve—seven times throughout 2022 followed by four additional increases in 2023—to temper price pressures nationally.

For Broadway’s adjustable-rate commercial mortgage lending model featuring many hybrid adjustable-rate loan facilities, this environment introduces complexity into interest income streams and customer affordability profiles.

Inflationary pressures burden commercial clients through increased wage costs and supply chain disruptions—heightening default risk on their loans if margins compress or sales deteriorate.

Additionally, liquidity considerations arise given sizable uninsured deposit balances held by banks post–First Republic collapse; such deposits pose heightened withdrawal risks during periods of economic uncertainty potentially amplifying funding cost volatility for banks including Broadway [S1].

Unpacking the Profitability Puzzle: Net Losses and Capital Moves

The financial results for the quarter ended September 30, 2025 exhibit net losses totaling approximately $23.9 million while simultaneously maintaining cash plus equivalents near $19.7 million [F1]. This disparity reflects ongoing revenue pressures against elevated administrative costs alongside rising provisions for credit losses possibly tied to challenged borrower performance amid inflationary strain.

Such losses underscore the difficulty of sustaining profitability within a highly focused mission-driven business model exposed to niche lending risks.

Capital actions like the October 2023 reverse stock split improved share price metrics enhancing attractiveness to market investors while reducing share count; repurchasing FDIC-held shares consolidated voting influence aiming to reinforce shareholder stability during turbulent periods [S1].

Overall these maneuvers depict calculated attempts at shoring up capital adequacy in anticipation of continued operational headwinds.

Competitive Landscape: Battling Larger Players for Niche Markets

Operating primarily within two major urban centers—the Washington D.C. area and Southern California—Broadway competes against entrenched regional banks alongside national institutions wielding greater resources and brand recognition.

This competition places Broadway at a disadvantage regarding scale economies impacting marketing reach or digital infrastructure investments necessary for modern consumer expectations.

Yet Broadway’s targeted socially focused banking proposition differentiates it meaningfully from peers by emphasizing inclusive economic development—not solely financial returns.

Successfully communicating this dual value proposition while managing cost structure remains critical as larger banks inevitably encroach into community finance sectors [S1].

Governance and Stakeholder Alignment: Balancing Purpose with Performance

Being a public benefit corporation inherently alters Broadway’s decision prism beyond simple shareholder profit maximization to include workers’ welfare, community impact, environmental stewardship—and overall societal benefits.

This multiplicity introduces complexities balancing competing priorities especially during periods demanding swift corrective action prompted by financial stress or market shifts.

While embedding greater accountability toward diverse stakeholder groups offers trust-building pathways with communities served—it also may limit the agility accessible to purely profit-driven competitors lacking such fiduciary dualities [S1], [valye_report_excerpt].

Maintaining transparent communication channels among shareholders who vary from mission advocates to traditional investors remains essential.

Examining Regulatory Oversight and Risk Management Approaches

Broadway Financial functions under stringent regulatory auspices including Federal Reserve Board supervision combined with oversight from the Office of the Comptroller of Currency (OCC) and deposit insurance conditions imposed by the FDIC.

These layers enforce rigorous standards concerning capital adequacy measurement especially surrounding allowance for credit losses—an area requiring close scrutiny given persistent risks embedded within real estate collateral susceptible to valuation declines during economic downturns.

Risk disclosures acknowledge interrelated factors encompassing macroeconomic volatility alongside localized property market dependencies necessitating prudent provisioning policies ensuring resilience amidst uncertainty [S1], [valye_report_excerpt].

Management appears cognizant of potential insufficiencies in current credit loss reserves vis-à-vis future actual realized losses demanding ongoing monitoring adjustments.

Forward-Looking Challenges and Strategic Imperatives

Looking forward, Broadway confronts an array of intertwined challenges emblematic of its specialized business model: navigating persistent inflationary environments affecting borrower stability; mitigating concentration risks linked to singular regional focus; countering intensified competition from larger institutions with broader capabilities; all while adhering uncompromisingly to its founding social mission encapsulated within public benefit corporate governance.

Strategic imperatives therefore include refining risk management frameworks adaptable to rapidly changing conditions; exploring modest portfolio diversification avenues respectful of mission constraints; securing additional capital support potentially via equity issuance or partnerships; fortifying digital banking capabilities enhancing customer engagement without compromising personal connection valued by communities; continuing transparent stakeholder dialogue balancing financial prudence with social outcomes.

Ultimately sustaining viability requires nuanced calibration uniquely suited to marrying community uplift objectives with disciplined banking fundamentals amidst complex macroeconomic headwinds [S1], [valye_report_excerpt].

Disclaimer: This analysis is provided solely for informational purposes based on publicly available data as of February 14, 2026. It does not constitute investment advice nor any recommendation regarding securities mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments