Vertex Pharmaceuticals: Dominance in Cystic Fibrosis Amid Innovation Challenges and Market Pressures

A comprehensive analysis reveals Vertex’s commanding hold on the cystic fibrosis market balanced against risks from pipeline concentration and evolving biotech dynamics.

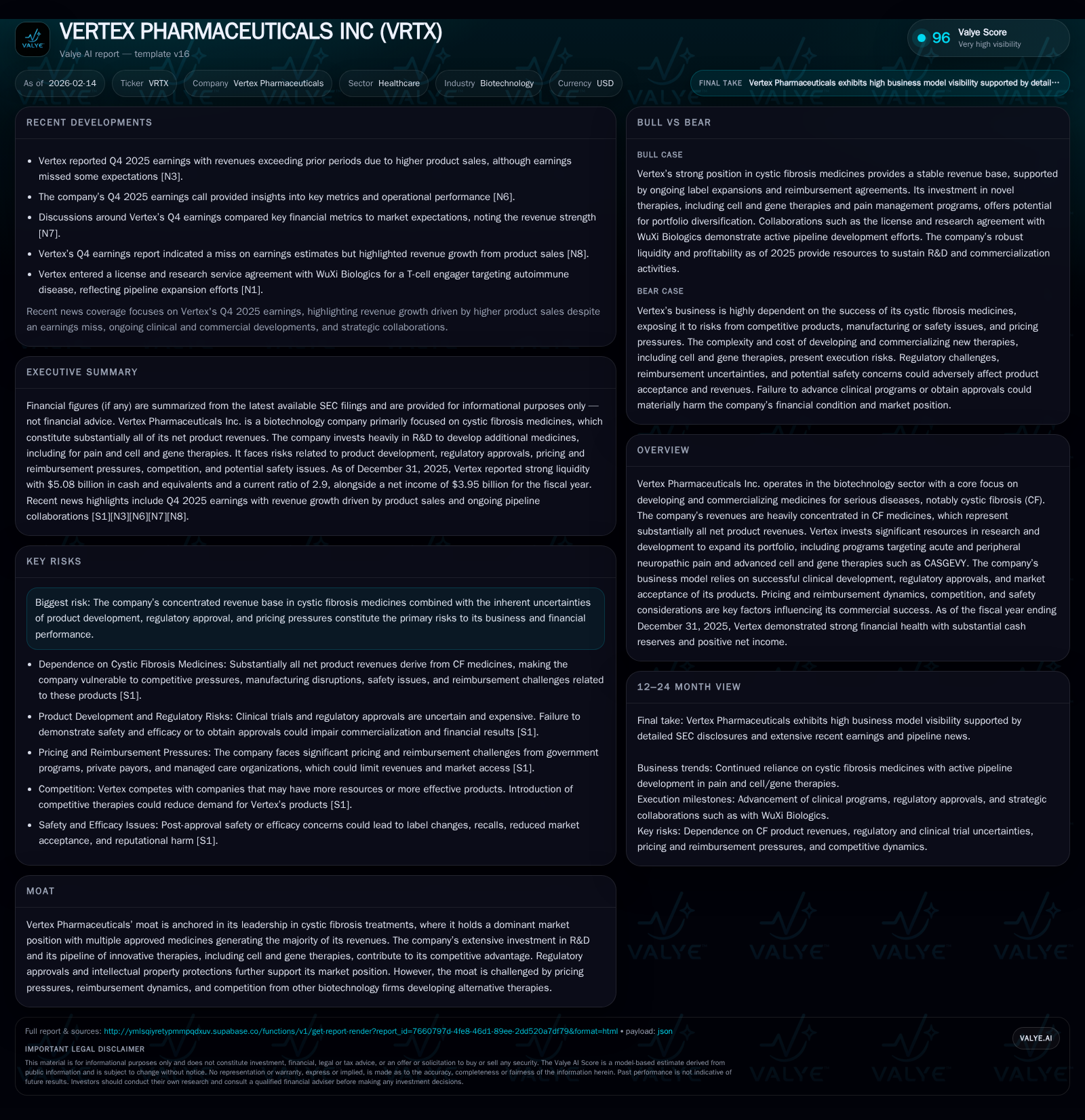

Vertex Pharmaceuticals remains the unshakable leader in cystic fibrosis treatment, with its suite of CF drugs forming the bedrock of its revenue and competitive moat. Yet this foundation is double-edged, exposing the firm to significant risk due to revenue concentration and intense pricing pressures. While its ambitious pipeline spans advanced cell and gene therapies like CASGEVY and neuropathic pain candidates, these programs face steep clinical and commercialization hurdles. Navigating regulatory complexities, reimbursement challenges, and a shifting competitive landscape will be pivotal for Vertex’s growth beyond its traditional core.

Vertex’s Cystic Fibrosis Stronghold: The Foundation of Its Moat

At the heart of Vertex Pharmaceuticals’ empire lies an undeniable dominion over the cystic fibrosis (CF) therapeutic space. Their portfolio of CF medicines accounts for nearly all net product revenues, positioning Vertex as the quintessential specialist in this rare yet devastating genetic disease [S1], [valye_report_excerpt]. This concentration is no accident but rather the fruit of years of focused R&D investment coupled with successful navigation of regulatory approvals that have secured intellectual property protections.

Yet this dominance carves a double-edged sword. While it cements a formidable moat against competitors through established patient bases and physician trust, it also leaves Vertex heavily dependent on a narrow product subset. Any disruption—be it emerging competitive therapies or shifts in payor reimbursements—could materially impact its financial health [S1]. Furthermore, the challenge intensifies as Vertex faces an imperative to innovate therapies for patient subsets not amenable to current CF medicines to sustain growth [S1].

The company’s moat is thus a fortress built on success but surrounded by vulnerability — one tethered tightly to the ongoing acceptance and evolution of its CF offerings.

The Financial Pulse: Robust Cash Position Meets Earnings Miss

Closing out fiscal year 2025, Vertex displayed strong balance sheet fundamentals underscoring operational resilience with cash & equivalents standing at approximately $5.08 billion and a healthy current ratio of about 2.9 [F1]. These metrics reflect ample liquidity to fuel ongoing research initiatives without immediate financing concerns.

Nevertheless, the nuanced picture revealed itself in Q4 earnings results: while total revenues exceeded expectations fueled by higher product sales, net income fell short of Wall Street forecasts [N2], [N3], [N4]. This divergence highlights operational complexities—perhaps increased costs related to R&D or commercial investments—that are pressuring near-term profitability despite top-line strength.

Such results necessitate balancing acts — maintaining investor confidence while financing ambitious innovation pipelines — amid a landscape demanding both short-term efficiency and long-term vision.

Innovation Pipeline: From Gene Therapy Ambitions to Neuropathic Pain Challenges

Vertex projects its future less as a single-indication powerhouse but more as a diversified innovator aiming beyond CF’s boundaries. The company’s marquee pipeline asset is CASGEVY, an advanced cell and gene therapy leveraging sophisticated technologies intended to address serious diseases through durable biological intervention [S1], [valye_report_excerpt]. However, CASGEVY introduces substantial manufacturing complexity; scaling production entails resource-intensive cell collection procedures and reliance on myeloablative preconditioning—a regimen associated with significant side effects that could hinder widespread acceptance.

Parallel to this are programs targeting neuropathic pain conditions via novel ion channel inhibitors (NaV1.7/NaV1.8). Although these represent promising avenues with sizeable unmet needs, they are fraught with clinical trial uncertainties—efficacy endpoints are difficult to achieve for pain indications—and face fierce competition from both established pharma players and emerging biotech entrants [S1].

Each pipeline component embodies a commitment to technological leapfrogging but underscores the precariousness inherent in early-stage biotech innovation where clinical failures or regulatory setbacks can swiftly recalibrate growth trajectories.

Pricing Pressures and Market Access: How Reimbursement Dynamics Shape the Future

Biotech drug pricing remains under intense scrutiny globally; payors are increasingly reluctant to grant premium reimbursement without demonstrable cost-effectiveness improvements [S1], [S2]. Vertex contends with these headwinds amidst rising healthcare budget constraints. Despite strong patient outcomes associated with CF therapies historically justifying higher prices, sustained margin integrity depends on successful negotiations with governments, insurers, and pharmacy benefit managers.

The complexity deepens for CASGEVY where not only efficacy but also procedural costs—including hospital administration of conditioning regimes—factor into payer calculus. Failure to secure adequate coverage could limit adoption regardless of clinical merit.

Pricing pressures thus form a dynamic battleground shaping commercial viability alongside clinical innovation.

Regulatory Landscape and Clinical Trial Uncertainties

Securing regulatory approvals remains a gateway hurdle for Vertex’s forward-looking ambitions. The company actively pursues accelerated pathways where possible but must deliver rigorous clinical evidence proving safety and efficacy [S2], [valye_report_excerpt]. Delays or negative data from trials could stall momentum; conversely, positive readouts bolster valuation narratives by extending patent lifespans through label expansions or novel indications.

Recent quarterly disclosures emphasize timelines for data availability from ongoing studies remain sources of uncertainty impacting near- to mid-term planning [S2]. As competition intensifies—especially with rival gene editing technologies emerging—maintaining regulatory agility is paramount.

The Road Ahead: Commercializing CASGEVY and Diversification Strategies

With clear recognition that CF revenues cannot indefinitely bear growth expectations alone, Vertex’s strategic playbook centers on scaling CASGEVY adoption while expanding its CF medicine footprint geographically and demographically [S1], [S2], [valye_report_excerpt]. Younger patient populations represent an extension opportunity for existing therapies; geographic expansions hinge upon navigating disparate regulatory environments effectively.

Commercializing CASGEVY poses unique challenges: operational demands rise exponentially relative to small-molecule drugs due to inpatient administration requirements and manufacturing intricacies. Management signals prioritization of building infrastructure supporting these processes alongside targeted marketing efforts geared towards educating physicians and payors about long-term benefits versus procedural risks.

Success here would mark a transformational shift in Vertex’s revenue composition from monoculture dependence toward biotechnological diversity.

Risk Considerations: Revenue Concentration and Competitive Threats

The specter underlying much of Vertex’s prospects is its continued reliance on cystic fibrosis medicines which embody both strength and exposure [S1]. Revenue concentration clouds visibility should market share erode due to new entrants or if reimbursement deteriorates sharply. Notably, competitors like CRISPR Therapeutics grappled recently with wider-than-expected losses casting a shadow over gene editing valuations more broadly—a context potentially influencing investor sentiment around advanced therapies under development at Vertex [N1], [N14].

Additional risks include supply chain vulnerabilities inherent in complex biologics production as well as regulatory setbacks that could delay approvals or enforce additional safety monitoring burdens.

Taken collectively, these factors underscore an asymmetric risk profile requiring vigilant monitoring going forward.

Wall Street’s Viewpoint: Recent Analyst Actions and Market Sentiment

Investor response post-Q4 earnings illustrates tempered optimism — Oppenheimer notably upgraded Vertex Pharmaceuticals citing confidence in entrenched leadership alongside pipeline potential albeit cautious about earnings execution variability [N11], [N12]. Market reaction evidences recognition that while near-term headwinds exist, the company’s moat around CF treatments provides durable value underpinning longer-term opportunities.

This sentiment balances hope against realism; institutional investors weigh steady cash flow generation against execution risks embedded in innovation-heavy biotech models.

This analysis synthesizes available public disclosures up to February 2026 without providing investment advice or forecasts. It aims solely to illuminate key business dynamics shaping Vertex Pharmaceuticals’ present condition and future avenues within the complex biotechnology sector.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments