Credit Acceptance Corp's Subprime Auto Financing Faces Rising Expenses and Cybersecurity Imperatives

A specialized auto loan financier balances credit risk management, expense growth, and rigorous cybersecurity controls in early 2026.

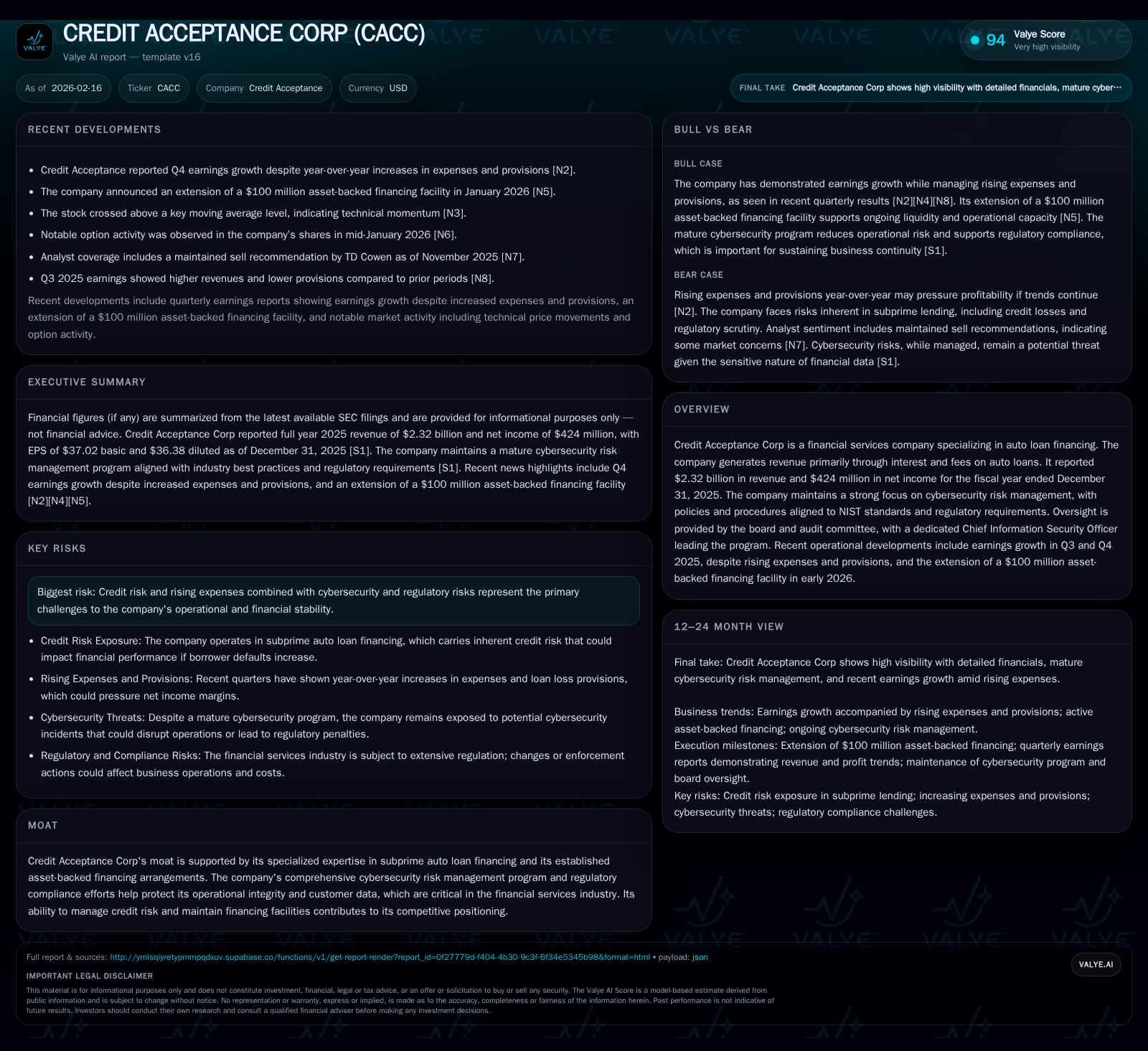

Credit Acceptance Corp (CACC) reported solid revenue and net income growth in the fiscal year ending 2025 despite a noted increase in expenses and credit provisions. The company’s niche expertise in subprime auto financing supports its strong asset-backed financing arrangements, critical for sustaining operations amid rising credit risks. Its comprehensive cybersecurity program, anchored in NIST frameworks and overseen by a dedicated CISO, addresses evolving regulatory and threat landscapes that are vital to maintaining operational integrity. The extension of a $100 million asset-backed financing facility signals ongoing liquidity support for its loan portfolio expansion.

Business Model and Financial Performance

Credit Acceptance Corp operates primarily in the subprime auto loan market—a sector characterized by higher credit risk but lucrative interest yields. The company's revenue model hinges on originating loans to borrowers with impaired or limited credit histories, generating income through interest payments and associated fees on these loans. In fiscal year 2025, CACC reported revenues of $2.32 billion alongside net income of $424 million [F1]. These figures underscore both the scale of their portfolio and operational effectiveness despite ongoing risk exposures.

Quarterly performance data highlights an earnings beat in Q4 2025 driven by strong loan originations; however, this came paired with increased operating expenses and higher credit loss provisions compared to prior periods [N2][N3]. Rising provisions are consistent with macroeconomic pressures impacting borrower repayment capacity within the subprime space. This dynamic necessitates prudent credit risk management alongside robust financing strategies.

Financing Strategies and Capital Structure

Liquidity management is pivotal given the capital-intensive nature of auto loan financing. Early January 2026 saw CACC extend a $100 million asset-backed financing facility [N6], an arrangement that securitizes pools of auto loans to optimize capital efficiency. Such facilities are critical for sustaining loan origination volumes without straining balance sheet resources.

CACC’s securitization expertise enhances its moat by enabling access to diverse investor bases while managing funding costs effectively. Historically, maintaining these securitization lines requires transparency into loan performance metrics such as delinquency rates, default probabilities, and loss severities—key focus areas for portfolio oversight.

Cybersecurity Risk Governance

In an industry increasingly reliant on customer data and digital platforms for underwriting and servicing loans, Credit Acceptance’s emphasis on cybersecurity emerges as a strategic necessity rather than a compliance afterthought.

The company has integrated cybersecurity risk management tightly into its enterprise risk framework. Oversight is provided by the board of directors through dedicated committees including the audit committee which receives formal reports on security posture [S1]. The appointed Chief Information Security Officer (CISO), holding a CRISC certification and with more than twenty years’ experience within financial services cybersecurity, leads program implementation.

Adherence to the NIST Cybersecurity Framework (SP 800-37 Rev. 2) guides policies designed to classify information systems based on criticality to business outcomes—differentiating between systems whose compromise could cause material financial or compliance harm versus secondary systems [S1]. The security program employs AI-assisted anomaly detection within network monitoring tools that elevate incident identification capabilities beyond traditional signature-based methods.

Annual audits led by internal teams supplemented by external experts perform vulnerability assessments from external, internal, and social engineering perspectives. This multilayered approach extends to third-party vendors whose security practices undergo rigorous scrutiny ensuring supply chain cyber risk is minimized.

Mandatory annual social engineering training for all employees further aids in reducing human-factor vulnerabilities—a notable source of breaches in financial firms broadly.

Sector Challenges: Credit Risk & Expense Management

Subprime footings inherently carry elevated default risks necessitating erring on the side of conservatism when setting reserves. The increase in provisioning seen during late 2025 highlights this pressure [N2][N3]. Managing these risks while preserving loan growth opportunities requires fine balancing acts where underwriting discipline meets data-driven decision-making.

On the expense front, incremental investments reflect broader industry trends where enhanced regulatory scrutiny around consumer lending practices compels higher spend in compliance infrastructure and operational controls. Inflationary pressures on labor and technology sourcing also contribute to rising costs.

Competitive Moat Considerations

CACC specializes in subprime auto loans with proprietary underwriting models tailored to borrowers often underserved by traditional lenders. Coupled with long-term relationships enabling repeated asset-backed securitization deals, the company retains a competitive edge hard for newer entrants lacking scale or structured funding capabilities.

However, market conditions remain fluid; shifts toward electric vehicles may influence future collateral valuations impacting recovery rates post-default—a subtle but important consideration as vehicle mix evolves industry-wide.

Regulatory Landscape

Compliance obligations span federal statutes such as the Gramm-Leach-Bliley Act requiring safeguarding customer information integrity alongside sector-specific rules like New York State Department of Financial Services cybersecurity regulation (23 NYCRR 500) [S1][S7].

Constant monitoring of regulatory evolution remains paramount since lapses can produce reputational damage or enforcement actions affecting licensing or capital adequacy.

Summary

Credit Acceptance Corp stands at a crossroads where multifaceted pressures—from growing credit cost concerns to intensifying cybersecurity threats—converge simultaneously. Its sustained revenue growth supported by specialized underwriting prowess coexists with rising expense burdens related principally to provisions and risk controls.

The recent renewal of its asset-backed financing facility complements its financial agility essential for continued loan portfolio expansion. Meanwhile, its mature cybersecurity posture aligns firmly with industry best practices underscored by ongoing board engagement and layered defenses leveraging AI innovations.

Stakeholders should observe how effectively CACC navigates these interconnected challenges over coming quarters amid evolving macro-financial conditions that disproportionately affect subprime borrowers.

Disclaimer: This analysis is intended solely for informational purposes regarding Credit Acceptance Corp's business operations and market context as of early 2026. It does not constitute investment advice nor any endorsement of securities trading.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments