TRIO-TECH INTERNATIONAL: Financial Opacity and Operational Uncertainty Amid Modest Profitability

Exploring TRIO-TECH’s opaque business profile through its limited disclosures and recent financial performance reveals a complex picture of stability shadowed by uncertainty.

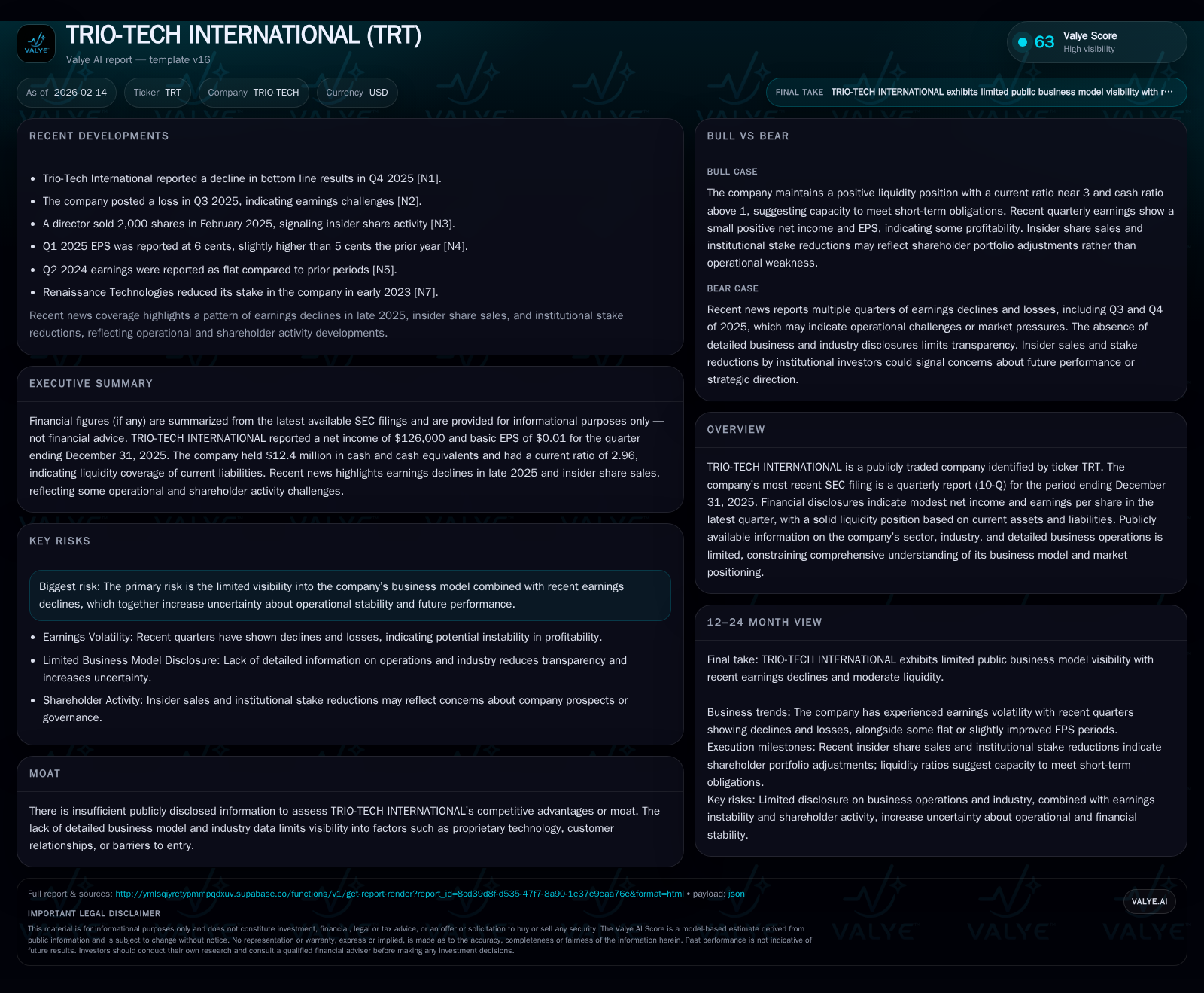

TRIO-TECH INTERNATIONAL (ticker TRT) presents a notable challenge for analysis due to the scarcity of disclosed sector and operational details despite its status as a public company. Its latest quarterly financials show modest profitability and a strong liquidity position, yet the absence of industry context limits traditional valuation and competitive assessment. This report examines TRT’s financial statements and risk disclosures to provide insight into the company’s current positioning while emphasizing the caution warranted by its informational opacity.

Unpacking TRIO-TECH’s Elusive Business Identity

What do we really know about TRIO-TECH INTERNATIONAL beyond its ticker symbol? The company’s latest quarterly SEC filing for the period ending December 31, 2025 ([S2]) provides scant detail on its operational focus or market sector. Despite being publicly traded under the symbol TRT, neither the 10-Q nor other easily accessible disclosures specify its industry classification or core business activities. This absence of contextual information leaves analysts peering through a fog when attempting to discern business drivers or competitive dynamics.

Such informational scarcity poses material challenges. Without clarity on product lines, service offerings, or customer bases, conventional approaches to valuation—such as peer comparables analysis or market size evaluation—are effectively handicapped. This lack also stymies efforts to evaluate operational efficiencies, margin structures, or strategic positioning beyond headline financial metrics.

A Dive into the Latest Financials: Stability Amid Thin Margins

Turning to hard numbers from the same quarterly filing ([S2], [F1]), we observe that TRT recognized $126,000 in net income during the quarter ending December 31, 2025. While clearly positive, this figure is modest considering historical revenue references—$32.5 million as last reported in mid-2021—and implies narrow profit margins under current conditions.

This subdued bottom-line performance suggests either pressure on cost structures or revenue growth constraints over recent periods. For investors or analysts accustomed to firms with clear growth narratives or robust profitability signals, such slim earnings can be hard to parse absent deeper operational insights. Nonetheless, positive net income remains an important foundation for potential value creation.

Decoding Liquidity: What the Balance Sheet Reveals

A silver lining emerges upon examination of TRT's balance sheet components ([F1]). Current assets totaled around $34.7 million against current liabilities near $11.7 million at the end of December 2025. The resulting current ratio approximates 2.96—a metric widely regarded as indicative of comfortable short-term liquidity coverage.

Cash and equivalents alone accounted for approximately $12.4 million, representing a sizeable liquid buffer relative to short-term obligations. This healthy liquidity position may afford the company operational flexibility amid uncertain external environments or within potential strategic pivots.

Interpreted cautiously given overall data paucity, this aspect nonetheless lends some reassurance regarding TRIO-TECH’s ability to meet immediate liabilities without distress.

Navigating Risks in the Fog of Limited Transparency

The risk factor disclosures in Item 1A ([S2]) underscore key concerns primarily centering on disclosure limitations themselves rather than specific industry risks. The company acknowledges that lack of clarity about its own business model contributes substantially to investor uncertainty. This opacity intersects with recent earnings variability to amplify concerns regarding operational predictability and future performance trajectory.

Such candid admission is noteworthy; it simultaneously reflects compliance with regulatory expectations and highlights profound underlying ambiguity. For stakeholders evaluating TRT’s risk profile, this creates a nuanced scenario where traditional risk assessments based on competitive threats or supply chain exposures give way to fundamental questions about business identity.

Assessing Moat Potential When Industry Clues Are Missing

In most equity analyses, evaluating a company’s economic moat—the sustainable competitive advantages protecting profits from competitors—is essential. With TRIO-TECH’s opaque disclosures and absent industry specification ([valye_report_excerpt]), conducting such an assessment verges on impossible.

Theoretically, moats might derive from proprietary technologies, entrenched customer relationships, high switching costs, regulatory licenses, or scale advantages. However, none of these can be confirmed nor refuted without concrete information regarding TRT’s operating environment or business fundamentals.

Thus, any discussion about moat potential here must remain conceptual rather than empirical; investors are left awaiting clearer signals should disclosure improve in subsequent reports.

Strategic Implications: What Investors Should Consider Next

Given the informational constraints surrounding TRIO-TECH INTERNATIONAL's public filings ([S2],[F1]), prospective investors and analysts would do well to emphasize strategic due diligence anchored in monitoring upcoming disclosures. Progressive clarity may emerge through newer quarterly updates or supplementary filings that shed light on segments served or client profiles.

In interim assessments, prudent consideration of risk versus reward is warranted; while liquidity metrics suggest financial stability that could support continued operations even amid adversity, thin profitability margins invite scrutiny related to operational scalability or cost containment effectiveness.

Exploring alternative research avenues such as vendor databases, industry intelligence providers, or consultations with domain specialists may also help compensate for current disclosure deficits.

The Data Deficit Dilemma: How to Interpret Confidence and Uncertainty

TRIO-TECH INTERNATIONAL epitomizes the challenges faced when analyzing companies cloaked in relative financial and operational obscurity. Balancing modest quantitative positives like net income presence and strong liquidity against overarching qualitative unknowns requires disciplined interpretation.

Despite enforcement-driven transparency efforts reflected in regulatory filings, critical gaps persist—leaving stakeholders forced into conjecture when forming views on sustainability and competitive positioning. This dynamic underscores broader questions about coverage standards for smaller or less communicative public entities.

Ultimately, maintaining investigative rigor while resisting overreach becomes central to navigating such data deficit scenarios with intellectual honesty and calibrated confidence.

This analysis is based entirely on publicly available SEC filings and verified numerical data as of February 14, 2026 ([S2], [F1]). It deliberately refrains from speculative conclusions unsupported by documented evidence and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments