Citius Oncology’s LYMPHIR Launch: Innovation Amid Financial Strains in the CTCL Market

An in-depth review of Citius Oncology’s pioneering therapy LYMPHIR, its early commercial steps, financial hurdles, and competitive dynamics within a niche lymphoma segment.

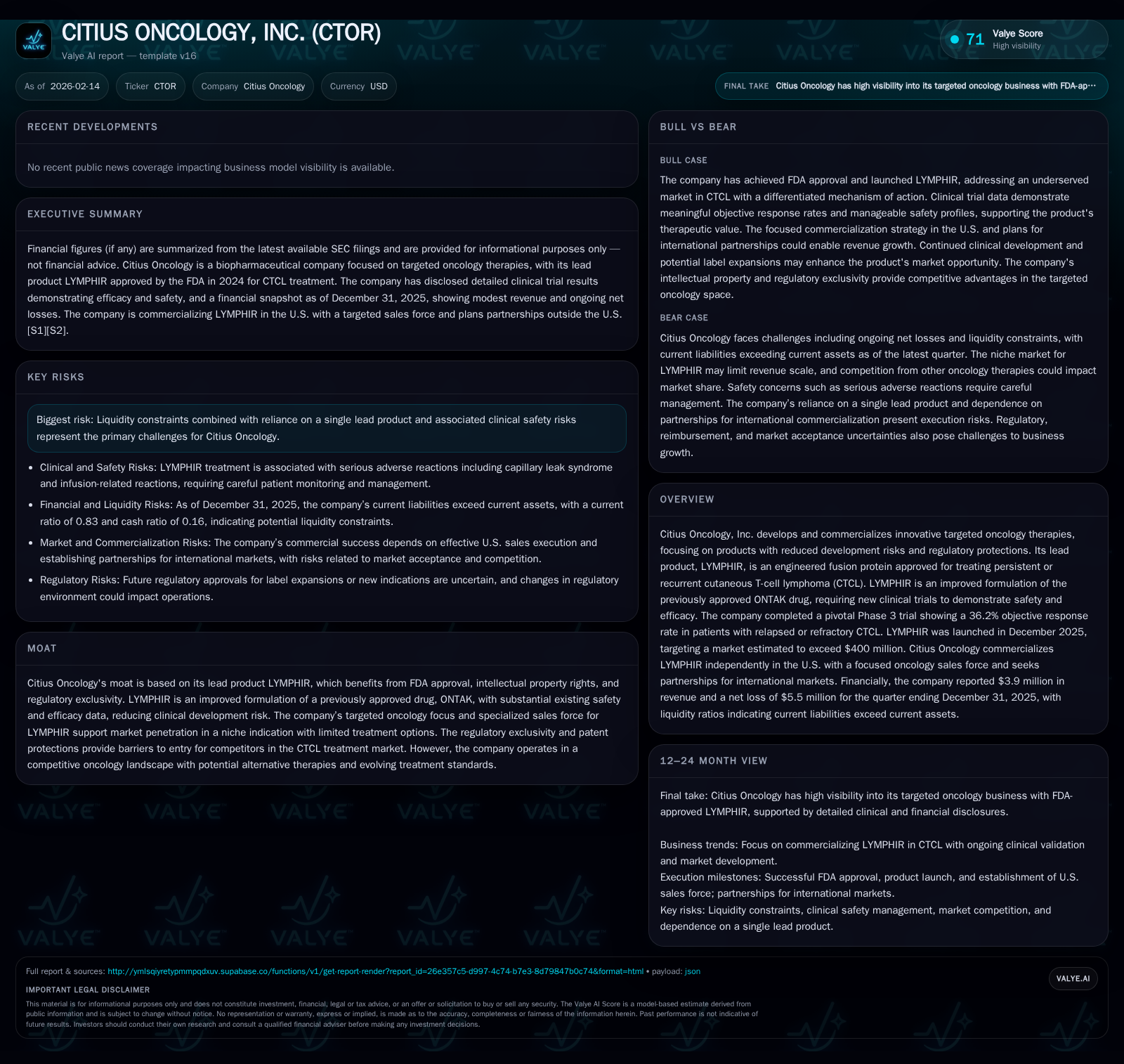

Citius Oncology emerged from complex corporate restructuring to launch LYMPHIR, a refined therapeutic targeting persistent or recurrent cutaneous T-cell lymphoma (CTCL), a rare and challenging cancer subtype. LYMPHIR’s FDA approval and pivotal Phase 3 data provide clinical credibility and a protective moat grounded in intellectual property and regulatory exclusivity. However, the company faces notable fiscal headwinds with limited cash runway post-launch, necessitating strategic partnerships or additional financing to sustain operations and expand its market footprint in a competitive oncology landscape. This report balances the promise of LYMPHIR against imminent operational risks tied to capital constraints and reliance on a single asset.

From Lab to Launch: LYMPHIR’s Journey and Promise

Citius Oncology’s lead asset, LYMPHIR™, represents both the culmination of an intricate development path and the onset of considerable challenges associated with first-in-market commercialization. As an engineered IL-2 diphtheria toxin fusion protein approved by the FDA in August 2024 [S1], LYMPHIR was specifically designed to address persistent or recurrent cutaneous T-cell lymphoma (CTCL), a rare subset of non-Hodgkin lymphoma characterized by limited effective treatment options. The company advanced LYMPHIR after acquiring rights from legacy formulations, notably improving on ONTAK® — an earlier approved drug sharing the same fusion protein backbone but differing in formulation.

To validate safety and efficacy reflective of its re-engineered profile, Citius conducted a rigorous pivotal Phase 3 clinical trial culminating in an objective response rate (ORR) of 36.2% in relapsed/refractory CTCL patients [valye_report_excerpt]. This respectable efficacy figure demonstrates meaningful disease control within an underserved population segment while helping de-risk the product clinically compared to wholly novel molecular entities. After securing FDA approval that conferred regulatory exclusivity protections — critical to protecting commercial value — LYMPHIR was officially launched in December 2025 [S1]. The company aims to penetrate a specialty oncology market estimated at over $400 million annually, suggesting significant growth potential as physicians gain familiarity with the drug.

Innovating on Familiar Ground: The Strategic Edge of Re-Formulation

Rather than embarking on development from molecular inception, Citius Oncology strategically capitalized on pre-existing efficacy and safety data related to ONTAK by introducing an improved formulation—LYMPHIR—that necessitated additional clinical trials but mitigated typical development risks inherent with de novo drug candidates. This approach reflects a broader industry trend where reformulated or repurposed agents leverage known pharmacological profiles to accelerate approvals while extending patent lifelines.

At its core, LYMPHIR comprises the IL-2 diphtheria toxin fusion protein backbone familiar from prior approvals; however, adjustments in manufacturing processes, excipient profiles, or stability parameters require fresh regulatory scrutiny [valye_report_excerpt][S1]. Intellectual property rights surrounding these novel formulation techniques grant Citius substantial protective moats against generic entrants or biosimilar competition during statutory exclusivity periods. This intellectual property advantage is particularly valuable given the niche status of CTCL treatment markets, which might otherwise be vulnerable to rapid commoditization.

Nevertheless, this strategy entails balancing cost implications arising from additional Phase 3 testing with expedited clinical timelines due to extant data—a tradeoff that continues shaping Citius's development expenditures and influencing investor confidence amid macroeconomic biotech funding shifts.

Short-Term Financial Turbulence: Dissecting Capital Constraints and Cash Burn

Despite progress advancing LYMPHIR into the marketplace, Citius Oncology's financial footing remains precarious based on recent filings [F1][S1]. In fiscal year 2025, revenue generation was nascent at approximately $3.9 million following LYMPHIR’s late-stage launch; concurrently net losses persisted at roughly $5.53 million underscoring ongoing operational burn.

More critically, liquidity metrics depict constraints that may impair near-term sustainability. As of December 31, 2025, cash and cash equivalents stood near $7.3 million juxtaposed against current liabilities approximating $44.7 million—a current ratio below unity at just 0.83 reflects insufficient short-term assets relative to obligations [F1]. Such imbalance signals reliance on external funding avenues for continued commercialization efforts, including sales infrastructure expansion and further clinical programs exploring additional indications.

This financial strain echoes through auditor assessments highlighting "substantial doubt" about ongoing viability absent further capital raises [S1]. Historically funded primarily through equity issuances supplemented by parent entity Citius Pharma support—with the latter owning roughly 78% stake as of late 2025—the company contemplates multiple strategic alternatives such as licensing deals or joint ventures that could inject liquidity while sharing commercial execution risk [S1]. How successfully management navigates these capital markets realities will be pivotal moving forward.

Commercial Ambitions vs. Clinical Realities: Targeting the CTCL Niche Market

On the commercial front, Citius Oncology has forged a targeted U.S.-based sales operation concentrating predominantly on key academic cancer centers treatment hubs where specialized oncologists manage CTCL patients [valye_report_excerpt]. This lean sales force approach optimizes resource allocation towards stakeholders most likely to prescribe LYMPHIR initially given its orphan indication.

However, real-world uptake presents familiar challenges: physician awareness must extend beyond early adopters into broader hematology-oncology practice communities; payor reimbursement pathways require navigation complicated by rare disease status; and patient identification remains inherently limited by CTCL’s low prevalence rates.

While competitors exist within this space—including newer immunotherapies or emerging agents—LYMPHIR's differentiated mechanism combined with regulatory exclusivity should ideally foster preferential consideration among prescribing clinicians [valye_report_excerpt][S1]. Yet execution risks persist whether due to delayed adoption curves or emergence of alternative modalities offering superior efficacy/safety balance.

Internationally, Citius plans partnerships rather than direct commercialization given operational limitations—moving cautiously abroad until domestic traction solidifies—a pragmatic stance reflecting lessons learned across specialist oncology drug launches.

Navigating Competitive Pressures and Regulatory Protections

LYMPHIR benefits considerably from intellectual property rights accompanied by FDA-granted regulatory market exclusivity—a dual-layered moat impeding direct competition for defined intervals post-approval [valye_report_excerpt][S1]. This protection reduces immediate threat from generic entrants or biosimilar substitutes which frequently erode value rapidly within oncology niches lacking patent coverages.

Nonetheless, clinical concentration risks emerge because corporate prospects hinge heavily on this single asset’s sustained market performance without diversified pipeline backup currently disclosed publicly. If adverse events materialize unwarranted by prior data or if efficacy fails longer term expectations, commercial demand could falter detrimentally.

Moreover, oncology therapeutics evolve briskly; competing innovations such as checkpoint inhibitors or next-generation biologics targeting diverse T-cell lymphoma subtypes might shift treatment paradigms thereby challenging LYMPHIR’s market share gradually [analysis]. Expansion into companion indications remains speculative pending clinical validation—delays or failures therein will exacerbate concentration exposure.

Strategic Pathways Ahead: Partnerships, Financing, and Expansion Opportunities

Recognizing immediate financial bottlenecks alongside growth imperatives underpins management’s openness toward multiple strategic scenarios [S1][valye_report_excerpt]. These include equity or debt financings keyed toward replenishing working capital essential for scaling commercial infrastructure beyond initial geographies.

Moreover, licensing agreements permitting globalization of LYMPHIR sales represent viable catalysts unlocking non-U.S. revenue streams without commensurate capital burden on the balance sheet—an industry-standard path for specialized biopharma products suffering distribution scale limitations domestically.

Potential alliances through joint ventures or co-marketing arrangements also serve dual purposes: mitigating execution risk while enabling shared R&D costs should lineage expansion into additional lymphoma variants progress successfully. However, such partnership negotiations can be protracted requiring alignment over valuation tiers amid volatile biotech markets.

Ultimately these strategic gambits aim at bridging short-term cash deficits while positioning the franchise for sustainable long-term earnings growth contingent upon robust adoption trends alongside manageable operating leverage enhancements.

Investor Takeaways: Catalysts, Risks, and Valuation Implications

Citius Oncology embodies a classic case study balancing innovative scientific repositioning within high-barrier niche oncology segments against tangible fiscal fragility characteristic among emerging biotech firms transitioning toward commercialization horizons [F1][S1][valye_report_excerpt].

For investors monitoring fundamental trajectories rather than trading narratives alone, key catalysts include progressive revenue growth validating physician adoption of LYMPHIR; positive updates regarding geographic expansions or label extensions; alongside successful closing of financing transactions alleviating immediate liquidity concerns.

Conversely risks cluster around accelerating burn rates outpacing operating income improvements; inability to scale sales coverage effectively; emergence of superior therapeutic alternatives altering prescribing behaviors; alongside regulatory setbacks related to manufacturing controls or postmarket safety profiles.

Assessment requires nuanced appreciation that while intellectual property-driven moats bolster competitive durability within CTCL markets normally constrained by low patient volumes—a reliance on single product lines combined with ongoing capital requirements underscores vulnerability inherent within small-cap specialty pharma businesses navigating commercialization inflection points.

In sum, Citius Oncology faces meaningful near-term operational challenges entwined with promising product attributes creating asymmetric potential if execution aligns tightly with strategic initiatives to optimize both clinical adoption curves and financial structuring efficiencies.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments