Navigating Uncertainty: An Investigative Review of Lendway, Inc.’s Financial Resilience and Leadership Shifts

A detailed examination of Lendway, Inc. reveals significant opacity in operations amid recent financial strains and leadership transitions.

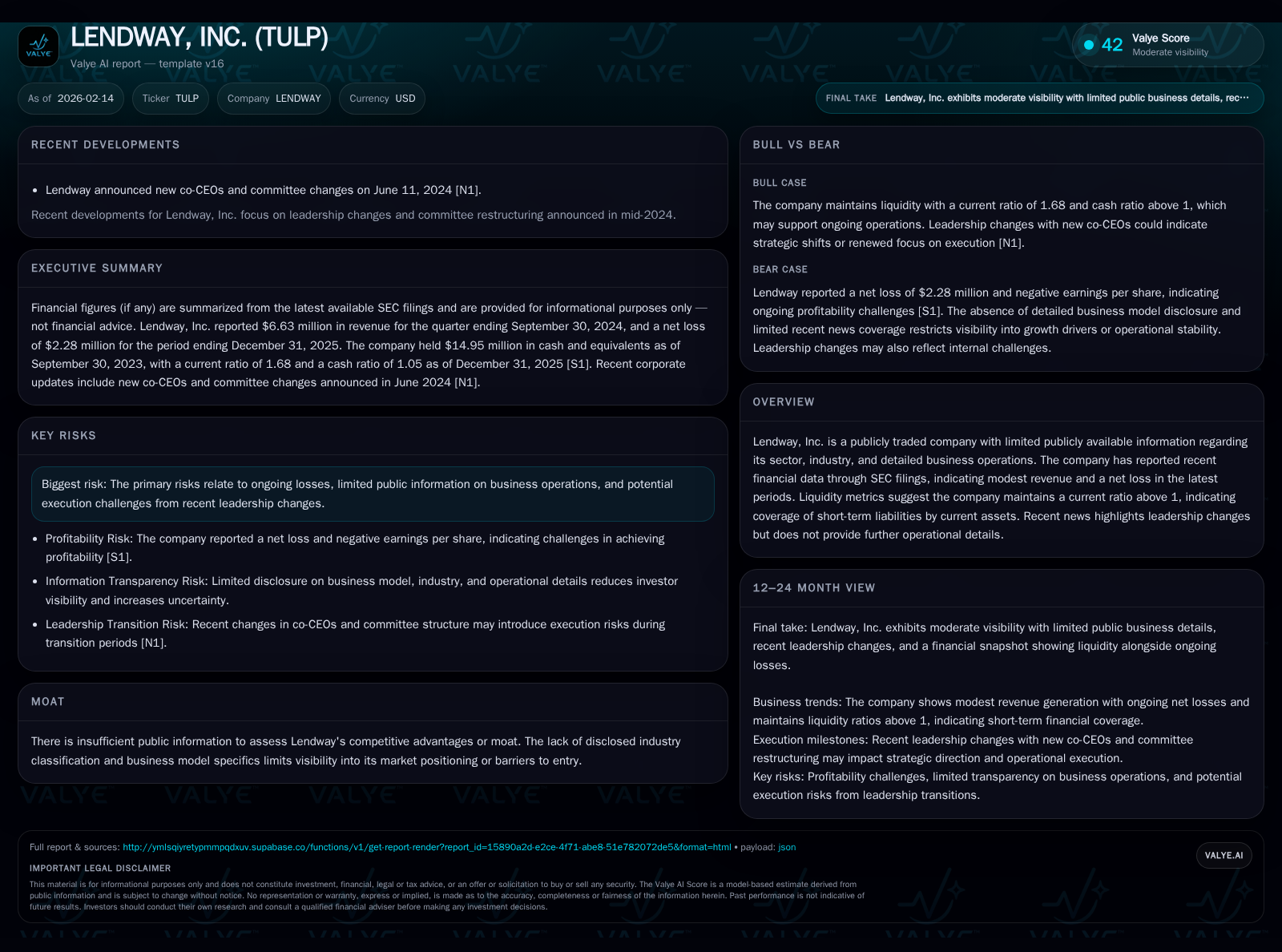

Lendway, Inc. presents a rare investigative challenge, with scant public information on its business model or industry classification. The company's financial disclosures reveal modest revenue generation juxtaposed with persistent net losses, while liquidity metrics such as a solid current ratio suggest some near-term financial cushioning. Recent leadership changes introduce further uncertainty around the firm's execution capabilities and strategic direction. Without clearer operational details, assessing Lendway’s competitive positioning or future outlook remains speculative.

Unpacking the Enigma: Who is Lendway, Inc.?

Lendway, Inc., trading under ticker TULP, stands out as an unusual specimen in the public equity universe: a publicly traded company devoid of any explicit sector or industry classification in its filings or disclosures. This opacity extends into operational descriptions — the company has not clearly articulated its business model or market niche in available documents [valye_report_excerpt]. For analysts and market observers accustomed to dissecting granular competitive dynamics within defined sectors, Lendway presents an unusual puzzle. The lack of publicly available information raises questions about the nature of its activities and complicates efforts to place it within any recognizable market ecosystem.

This absence of clarity also poses challenges to standard valuation frameworks which rely heavily on sector-anchored comparables and operational context. Researchers must therefore pivot their focus toward what can be tangibly assessed: disclosed financials and recent corporate developments.

Financial Portrait: Interpreting the Numbers Behind the Veil

Scrutinizing Lendway’s latest SEC filings reveals a company operating at a modest scale facing tangible headwinds. As of September 30, 2024, reported revenue sits at approximately $6.62 million—an amount that suggests a small enterprise or possibly a specialized niche player [F1]. The latest net income figure recorded on December 31, 2025 indicates a loss totaling roughly $2.28 million [F1][S2], reinforcing an ongoing challenge in managing costs relative to top-line inflows.

The share structure presents roughly 1.77 million common stock shares outstanding [S2], which positions Lendway as a micro-cap entity by traditional definitions. While these numbers provide some scaffolding for understanding scale and performance trajectory, deeper insight into revenue drivers or expense composition is unavailable due to minimal narrative disclosure.

Leadership Realignment: What Could Recent Changes Signal?

Recent reports of leadership changes within Lendway add complexity to interpreting the company's future prospects [valye_report_excerpt]. Without detailed commentary on executive roles impacted or strategic mandates driving this realignment, one must cautiously interpret such transitions as potential sources of execution risk.

For smaller companies already navigating near-term financial strain, leadership turnover can disrupt continuity and delay critical operational improvements or strategic pivots. Given the veil over core business activities, stakeholders are left uncertain whether new leaders bring fresh capital infusion strategies, operational expertise, or alternative growth initiatives necessary to reverse losses.

Liquidity Strength in the Shadows: Current Ratio and Cash Position

Despite reported net losses, Lendway maintains relatively sturdy liquidity metrics that merit attention. The latest cash and cash equivalents figure stands near $14.95 million as of September 2023 [F1], providing tangible runway for operations at least into forthcoming quarters absent major cash outflows.

Contributing further to this defensive posture is a current ratio calculation (current assets divided by current liabilities) of approximately 1.68 at year-end 2025 [F1]. This implies that short-term liabilities are comfortably covered by liquid assets plus other current receivables and holdings—a notable strength when balanced against the underlying operational losses.

Liquidity cushions such as these afford the company some degree of flexibility to manage expenses, potentially invest selectively in growth initiatives, or restructure obligations without immediate solvency threats.

The Growing Pains of Modest Revenue and Persistent Losses

The juxtaposition of relatively small revenues against consistent net losses frames Lendway’s financial narrative as one marked by growing pains and structural challenges [F1][S2]. While generating $6.6 million in annual turnover conveys some commercial traction, scaling beyond this threshold toward profitability evidently remains elusive.

This dynamic begs inquiry into cost structures or investment levels consuming revenue gains—details which remain undisclosed but are critical to understand if loss trends are to be arrested long-term. In absence of explicit financial breakdowns by segment or function, only cautious interpretation is possible regarding operational efficiency or margin pressures.

Risk Factors Amplified by Limited Transparency

From an analytical perspective, the greatest risks arise not solely from numeric losses but from the broader opacity enveloping Lendway’s business model and operations [valye_report_excerpt]. Scarce disclosures limit constructive scrutiny around revenue sustainability, customer concentration risks, technological differentiation (if any), or market positioning.

Additionally, execution risk is heightened due to recent leadership changes combined with known financial challenges. Without clear visibility into management strategy or inherent competitive advantages (moat), uncertainty persists around value proposition durability.

Investors and analysts face compounded difficulty conducting thorough due diligence; unknown contingencies or off-balance-sheet commitments could exist unseen beneath surface-level filings.

Market Footprint & Business Model: Reading Between the Lines

With no stated industry affiliation visible via filings nor public disclosures explaining product offerings or service lines, speculation on Lendway’s market footprint must remain guarded [valye_report_excerpt]. Such omission itself may suggest either highly proprietary niche operations not typical for reporting benchmarks or a transitional phase pending more formalized disclosure.

Absent explicit data points or comparative indicators, one might consider possibilities ranging from fintech solutions targeting specialty lending markets (inferred from name) to broader technology-enabled financing activities—however these remain speculative until verified.

The lack of classification compels caution in assuming scale effects, competitive landscape intensity, or regulatory frameworks applicable to Lendway’s activities.

Outlook Ambiguity: The Road Ahead for Lendway

The interplay between modest revenue scale, persistent net losses, liquidity adequacy, and leadership shifts encapsulates an ambiguous outlook for Lendway [valye_report_excerpt][F1][S2]. While near-term financial resilience appears supported by positive working capital metrics and cash holdings, these strengths do not fully offset concerns related to business model clarity and strategic direction under new management.

From this foundation emerges fundamental uncertainty about whether existing resources can be effectively leveraged to foster meaningful growth or reverse income deficits without clearer market positioning insights.

In sum, improved transparency through enhanced disclosures would be instrumental for all stakeholders seeking to discern authentic value creation potential in upcoming periods.

This analysis reflects information available as of February 14, 2026; it does not constitute investment advice but aims to provide an informed viewpoint grounded in documented evidence.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments