Flux Power Holdings: Unpacking Financial Stability Amid Sector Ambiguity and Limited Disclosure

Flux Power shows modest profitability and solid liquidity, yet its market positioning and strategic moat remain opaque.

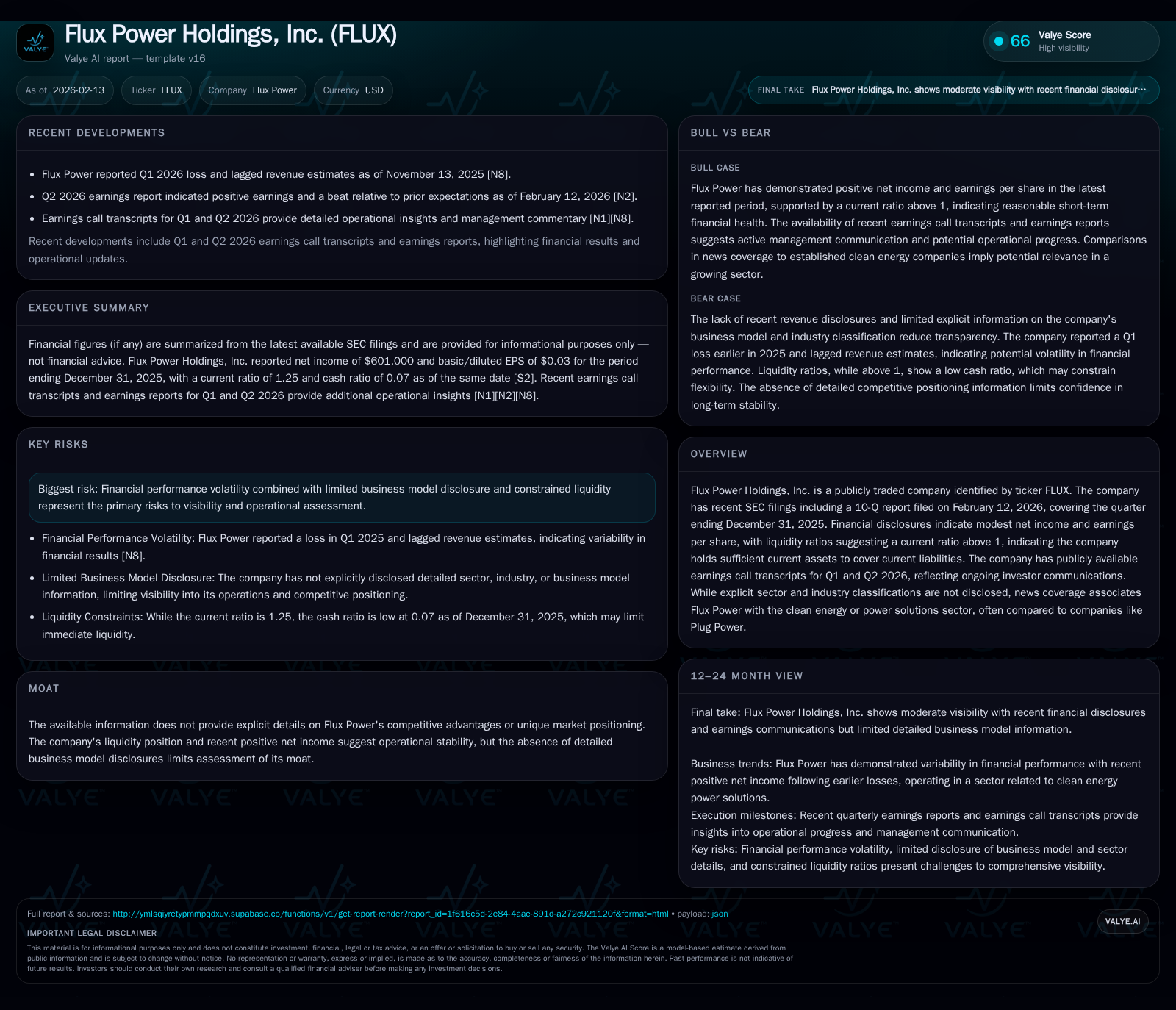

Flux Power Holdings, Inc. (FLUX) has reported steady but modest net income alongside a current ratio surpassing 1, indicating manageable liquidity. Its recent earnings beat and positive management tone provide some operational confidence despite minimal detail on business model specifics. The company occupies a somewhat ambiguous niche within the clean energy sector and lacks clear disclosure of competitive advantages, presenting challenges for visibility. Investors should weigh stable financial footing against limited transparency and inherent risks documented in recent SEC filings.

Charting Flux Power’s Financial Trajectory

Flux Power Holdings, Inc.'s latest SEC filings portray a company navigating modest profitability within an evolving energy landscape. As of December 31, 2025, the firm reported net income of approximately $601,000 — a tangible positive result that underlines cautious operational stability rather than rapid expansion [F1][S2]. Revenue trends remain less transparent due to data sparseness; however, available figures suggest consistent but unspectacular top-line outcomes thus far.

This constellation reflects an entity maintaining financial footing, albeit without pronounced growth acceleration. Such patterns are noteworthy because they denote survival and incremental advancement amid competitive pressure rather than breakthrough transformation.

Decoding Quarterly Highlights and Market Reception

The Q2 2026 earnings beat garnered attention when Flux Power outperformed consensus estimates, a near-term bullish signal that helped mitigate apprehension associated with limited disclosures [N2]. Management's tone during the earnings call was measured—balancing guarded optimism over operational improvements with reticence concerning explicit forward guidance [N1].

This cautious balance partly mirrors a company conscious of both its incremental progress and the opaque contours of its broader strategic pathway. No sweeping announcements or disruptive initiatives emerged from the dialogue, underscoring a narrative anchored more in steady execution than aggressive ambition.

Liquidity and Balance Sheet: Operational Stability Amid Tight Margins

A critical aspect underscored by Flux Power’s financial snapshot is its liquidity profile. The December 2025 quarter reveals current assets totaling roughly $27.6 million against current liabilities near $22.1 million, producing a current ratio around 1.25 [F1]. In practical terms, this ratio implies sufficient short-term resources to cover immediate obligations—a crucial buffer given the nascent profitability and volatility risks inherent in small-cap power technology firms.

Cash and equivalents stand at about $1.59 million as of September 2025, enough for operational continuity but not signalling significant excess cushion [F1]. The substantial current liabilities highlight ongoing working capital demands or accrued expenses. Thus, while the balance sheet supports operational resilience now, it also reflects tight margins warranting close scrutiny.

Competitive Landscape: Where Flux Fits Within Clean Energy Solutions

Despite explicit sector classification being absent from filings, external sources associate Flux Power with the clean energy or power solutions domain [valye_report_excerpt]. Media comparison to players like Plug Power positions it within a transformative industry segment focused on alternative energy storage or generation technologies.

However, this arena is crowded and rapidly evolving—with competition ranging from established firms to innovative startups advancing battery tech and power management solutions. Given scant public disclosure regarding product differentiation or market niche focus, determining Flux’s precise competitive placement remains challenging.

Exploring the Company’s Understated Strategic Moat

Neither the company's filings nor investor communications delineate concrete competitive advantages that might constitute a moat [valye_report_excerpt]. This lack of clarity can be a double-edged sword: while it prevents premature conclusions about sustainability of any edge, it also reflects underlying uncertainty about differentiation strategies in a high-tech sector dependent on innovation.

Nonetheless, positive net income alongside favorable liquidity metrics suggests operational competence—if not yet dominance—which might underpin future moat development pending strategic clarity.

Risk Factors: Navigating Visibility and Volatility Challenges

Flux Power explicitly acknowledges several risk dimensions affecting its outlook [S2]. Financial volatility emerges prominently—reflecting fluctuating earnings potential tied to sector dynamics and internal execution capabilities. Additionally, liquidity constraints relative to liabilities impose cautionary limits on runway flexibility.

Compounding these are disclosure limitations hindering comprehensive assessment by external analysts or investors. This opacity around business model details restricts visibility into revenue drivers, customer concentration, or technological differentiators—all pivotal for valuation certainty.

What Investor Communications Reveal — And Conceal

Earnings call transcripts from Q2 2026 provide rare insights into Flux’s narrative tone [N1]. Management emphasizes incremental gains but avoids detailed commentary on market share shifts or innovation pipelines. Repeatedly, references to operational ‘improvements’ are paired with acknowledgments of ‘ongoing challenges,’ reflecting pragmatic restraint.

The calls serve more as reassurances to maintain investor interest than definitive strategy disclosures. As such, they illuminate messaging priorities—stability over hype—but leave open questions about long-term prospects.

Valuing FLUX: Potential Upside vs. Disclosure Gaps

The juxtaposition of stable financial fundamentals such as positive net income and adequate liquidity against pronounced disclosure gaps complicates any straightforward valuation approach [valye_report_excerpt][F1][N2]. While Q2 earnings beats can hint at underlying momentum, insufficient transparency regarding operations curtails confident extrapolation.

Prudent valuation perspectives would therefore incorporate scenario analysis weighing fluxes in business model execution against macro industry tailwinds present in clean energy.

Looking Ahead: Key Catalysts and Monitoring Points

Future investor focus should center on quarterly filings for signs of revenue expansion or margin improvement that substantiate recent operational commentary [N1][S2]. Any shifts toward clearer communication regarding competitive positioning or new contracts could materially enhance understanding.

Additionally, monitoring moves by comparable companies like Plug Power may offer contextual benchmarks influencing Flux’s strategic trajectory within the broader clean energy evolution.

This analysis synthesizes publicly available information without extending investment advice or price forecasts. Readers should consider additional data sources when forming opinions about Flux Power Holdings.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments