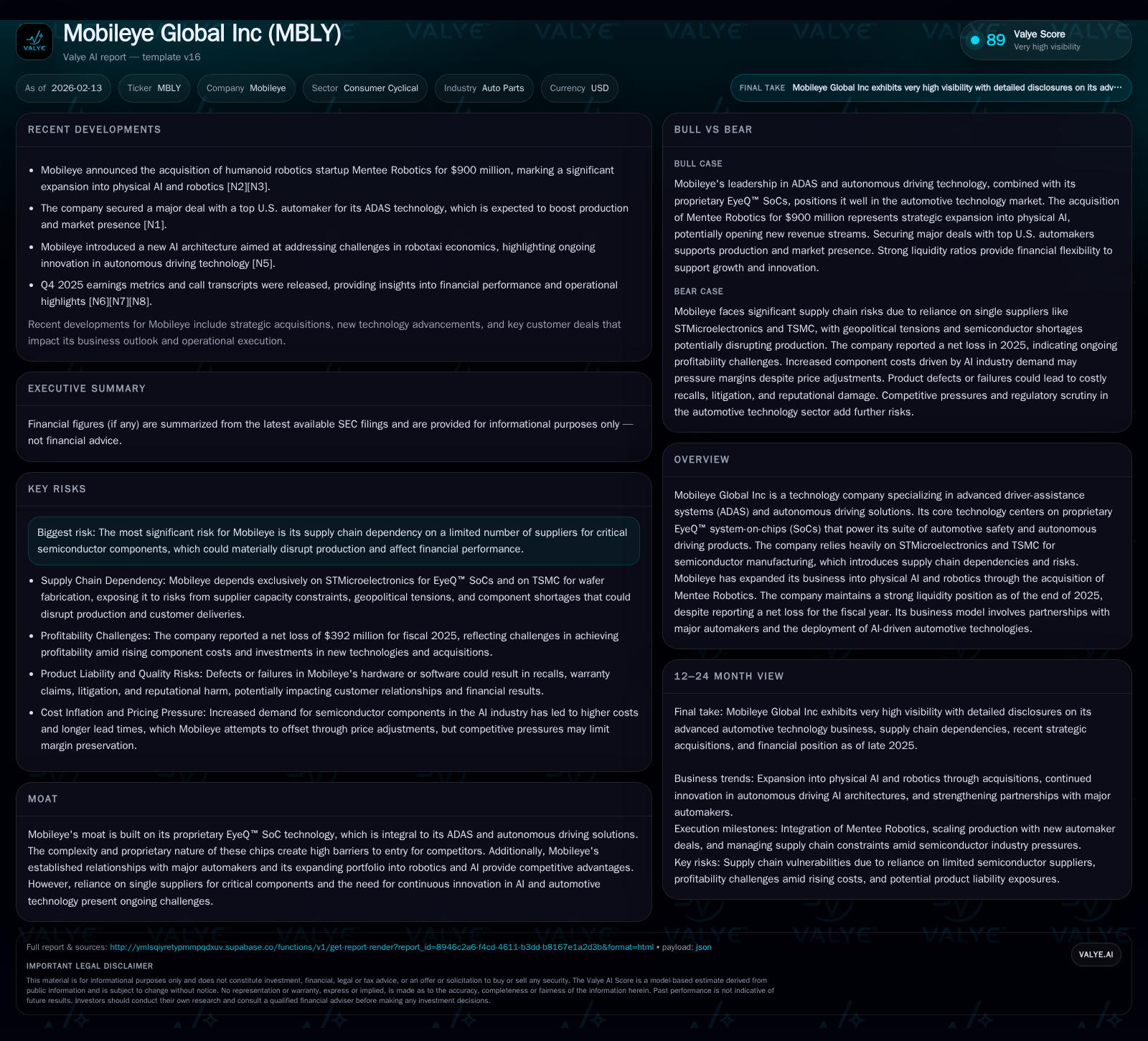

Mobileye at a Crossroads: Advancing ADAS Leadership and Robotics Expansion Amid Supply Chain Challenges

Mobileye Global Inc navigates a pivotal phase leveraging its proprietary EyeQ™ SoCs to reinforce ADAS dominance while launching into robotics, all under the shadow of semiconductor supply dependence.

Mobileye remains a foundational player in advanced driver-assistance systems, anchored by its EyeQ™ system-on-chip technology embedded across millions of vehicles worldwide. The company’s recent $900 million acquisition of humanoid robotics startup Mentee signals an ambitious diversification into physical AI and robotics beyond automotive applications. Nevertheless, Mobileye’s supply chain remains tightly coupled with STMicroelectronics for chip manufacturing, a focal operational risk that could constrain growth. Liquidity remains ample despite continued net losses, supported by strong OEM partnerships and an expanding production footprint. Strategic challenges ahead center on executing robotics integration, managing supply vulnerabilities, and sustaining innovation in a competitive auto tech landscape.

From Pioneering ADAS to Autonomous Future: The Core of Mobileye’s Innovation

Mobileye Global Inc has solidified its reputation as a trailblazer in advanced driver-assistance systems (ADAS) technology with more than 25 years of continuous innovation. Central to its technological prowess is the proprietary EyeQ™ system-on-chip (SoC), which powers a comprehensive suite of automotive safety and autonomous driving solutions. As of late 2025, this technology had been installed across approximately 1,400 different vehicle models worldwide and in excess of 230 million vehicles overall [S1]. These figures underscore Mobileye's remarkable breadth in terms of deployment scale and OEM engagement.

The company’s portfolio not only ascends from traditional ADAS functionalities but also anticipates the transition toward full autonomy. Its EyeQ™ SoCs are optimized to deliver mission-critical edge computing capabilities, combining sophisticated sensor fusion, real-time processing, and AI inference workloads necessary for both driver assistance and autonomous driving features [S1]. Strategic agreements, such as recent production deals with major U.S. automakers secured early in 2026, further validate Mobileye’s role as an integral tier-one supplier within automotive ecosystems [N2][N3]. This blend of proprietary hardware specialization married with deep OEM integration embodies Mobileye's technological foundation enabling it to shape the evolving mobility landscape.

Behind the Chips: The Critical Supply Chain Nexus with STMicroelectronics

Despite its technical strengths, Mobileye’s operational model reveals notable supply chain dependence risks centering on semiconductor manufacturing. The company currently contracts exclusively with STMicroelectronics for fabrication of its EyeQ™ SoCs [S1][S2]. This exclusivity stems from the chips' complex proprietary design which limits alternative manufacturing avenues without incurring steep requalification costs or technical hurdles.

Historical precedent accentuates this vulnerability—widespread global semiconductor shortages during 2021-2022 resulted in significant constraints on EyeQ™ chip availability. STMicroelectronics struggled to meet Mobileye's demand amid substrate scarcity and foundry capacity limits, forcing Mobileye into low inventory buffers entering 2022 [S1]. While conditions ameliorated in 2023 allowing inventory rebuilds and improved supply stability, any recurrence could severely impair timely deliveries and customer satisfaction.

Consequently, Mobileye maintains vigilant inventory monitoring to buffer against disruptions but building such inventory requires substantial capital outlays and exposes the business to risks related to component obsolescence [S1]. This precariousness amplifies capital allocation challenges given the need for continuous innovation alongside supply-side fragility.

Financial Pulse: Liquidity Strength Versus Persistent Net Losses

Examining Mobileye's financial health illuminates a nuanced picture—robust liquidity provides operational cushion even as profitability remains elusive. As of fiscal year-end December 27, 2025, the company reported cash and equivalents totaling approximately $1.84 billion against current liabilities near $406 million yielding an exceptionally strong current ratio above 6x [F1]. This healthy liquidity reflects prudent capital management amidst ongoing investments.

Nevertheless, Mobileye recorded a net loss of $392 million for the full year 2025 [F1], continuing a pattern rooted in heavy R&D spending and scaling costs inherent to high-tech automotive segments [N4][N7]. The company does not anticipate dividend payments in the foreseeable future partly due to these earnings constraints and reinvestment needs [S1].

Market responses following Q4 earnings indicated measure-aligned expectations were met with no major surprises. Operational commentary suggests incremental momentum driven by expanding OEM contracts but tempered by cost pressures linked predominantly to production scale-up challenges [N4][N6][N7][N8]. This dynamic underscores Mobileye’s status: a growth-oriented entity balancing cash preserve strategies while navigating path-to-profitability hurdles typical within emerging autonomous technologies.

New Frontiers: Evaluating the Mentee Robotics Acquisition and Robotics Expansion

In a pronounced strategic pivot during early 2026, Mobileye announced acquisition of Mentee Robotics—a humanoid robotics startup—for approximately $900 million [N1]. This move signals ambition beyond traditional automotive confines toward physical AI-driven robotics applications.

Mentee’s expertise centers on humanoid robots designed for interaction within human environments—a notably different domain yet leveraging synergies around sensing technologies, AI perception algorithms, and real-time computing honed at Mobileye [N1][S1]. This acquisition complements Mobileye’s existing AI capabilities by extending physical embodiment possibilities parallel to virtual autonomy efforts.

By branching into robotics alongside entrenched ADAS revenue streams, Mobileye seeks to diversify growth levers while capitalizing on cross-domain innovation potential. However, integrating this new business line will require adapting organizational competencies and investing further capital—underscoring that tangible benefits remain prospective rather than guaranteed.

Customer Confidence: Partnerships Anchoring Growth and Market Reach

Mobileye's ecosystem strength largely derives from its extensive OEM partnerships forming the backbone of its deployment strategy. Over 50 vehicle manufacturers globally incorporate Mobileye solutions into their platforms [S1], highlighting broad market acceptance.

Recent contracts secured with leading U.S. automakers exemplify this trend—most notably a high-profile agreement finalized in early January 2026 aimed at substantially increasing chip shipments tied to next-gen ADAS features over coming years [N2][N13][N14]. Such deals not only bolster near-term production visibility but reinforce competitive positioning vis-à-vis rivals pushing autonomous capabilities.

This network effect affords volume advantages aiding economies of scale while embedding Mobileye deeply within automotive value chains—critical fortification amid cyclical economic environments that influence vehicle production rates.

Quarterly Earnings Decoded: Market Reaction and Operational Momentum

Dissecting Q4 2025 financial results reveals measured progress juxtaposed with cautious optimism from investors. Earnings met consensus estimates without material deviations signaling steady execution under prevailing industrial pressures [N4][N7][N8].

Operator commentary from earnings calls elucidated ongoing initiatives around ramping production volumes aligned with new contract deliveries while highlighting cost management imperatives linked chiefly to supply chain calibration including chip procurement rhythms [N6].

The stock price reaction was muted yet positive following announcement—reflecting belief that while short-term volatility may persist due to external factors (e.g., semiconductor softness), underlying fundamentals retain integrity thanks to product relevance and expanding adoption.

Navigating Risks: Semiconductor Bottlenecks & Supply Chain Vulnerabilities

A recurring theme permeates all facets of Mobileye’s narrative—the critical dependency on uninterrupted supply of complex EyeQ™ chips from STMicroelectronics presents an ever-present operational risk with financial ramifications [S1].

Itemized risk disclosures explicitly warn that any prolonged disruptions could impair meeting customer orders affecting revenues materially through delays or order cancellations. Moreover, global macro-level factors such as pandemics exacerbating logistics bottlenecks or component raw material scarcity further amplify risk profiles.

Such vulnerabilities inevitably temper growth trajectories and introduce uncertainty layers not easily mitigated without diversification strategies such as alternative foundry engagement or redesigned chipset architectures—a non-trivial endeavor given intellectual property constraints.

Valuation Questions in a Cyclical Consumer Tech Landscape

From an analytical standpoint, evaluating Mobileye’s valuation requires balancing promising technological footholds against sector cyclicality paired with persistent operating losses. The consumer cyclical nature of automotive demand often injects volatility into revenue streams heavily influenced by vehicle production cycles [F1].

Additionally, reinvestment demands driven by continuous AI innovation advancements alongside newly embraced robotics lines suggest capital intensity will remain elevated precluding near-term free cash flow generation sufficiency for dividends or rapid deleveraging [S1][N9].

Investor expectations premised on sustained earnings beats must reconcile these structural realities—valuation narratives hinge critically on successful scaling execution across multiple fronts rather than transient metric improvements alone.

Envisioning Tomorrow: Strategic Challenges & Opportunities Ahead

Looking forward, Mobileye finds itself at a strategic inflection point marrying its entrenched ADAS authority with ambitions unlocked through robotics expansion. Core challenges rest on maintaining relentless AI innovation pace essential for competitive differentiation within automotive tech while achieving seamless integration of Mentee Robotics’ assets into broader corporate vision [S1][N1].

Supplier diversification emerges as another critical axis requiring foresight—as single-source reliance threatens future disruption risks hazardous to operational continuity [S1][N2]. Concerted efforts toward fabricator qualification alternatives or chip redesigns could serve to hedge vulnerabilities long term.

Competitive pressures also intensify from legacy auto suppliers pushing smart mobility solutions alongside emerging pure-play autonomous tech entrants escalating market fragmentation. Success therefore mandates dual execution excellence—in advancing cutting-edge technical offerings whilst orchestrating prudent commercial partnerships emphasizing reliable delivery commitments.

In essence, Mobileye embodies both the promise borne from pioneering embedded intelligence in vehicles and the caution necessitated by imperfect supply ecosystems amid rapid sector evolution. Navigating this landscape deftly will define whether it can sustainably transform technological leadership into durable market advantage across increasingly diverse domains.

This report is based solely on publicly available information as cited; it is intended for informational purposes only and does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments