AtlasClear Holdings: Navigating Profitability and Capital Dynamics Amid Operational Ambiguity

A closer look at AtlasClear Holdings' financial health and market maneuvers reveals a tale of solid liquidity against the backdrop of limited operational transparency.

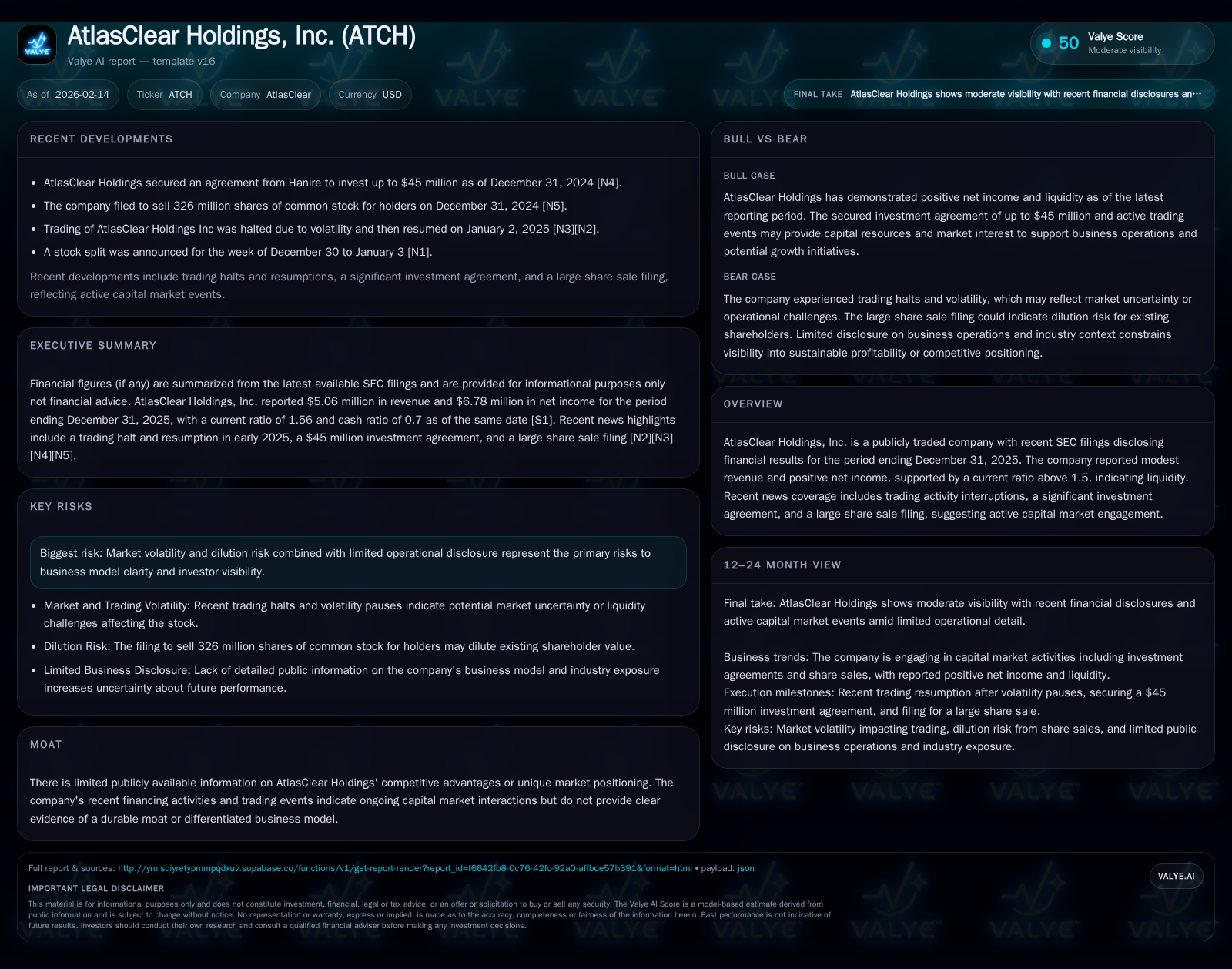

AtlasClear Holdings reported modest revenue of approximately $5 million yet posted net income exceeding $6.7 million in its latest quarter, indicating unusual profitability dynamics. The company's healthy current ratio of 1.56 and substantial cash reserves underline its sound short-term liquidity position. However, active capital market engagements, including recent trading interruptions and share sale filings, raise dilution concerns amidst sparse details on core operations. These factors combine to form a complex risk profile where strong financial footing contrasts with opaque business visibility.

Financial Snapshot: Profitability Against the Odds

AtlasClear Holdings’ financial results for the period ending December 31, 2025, present an intriguing profile. The company reported revenues just above $5 million yet achieved net income exceeding $6.7 million [F1]. This disparity between top-line and bottom-line figures is unusual; typically, net income trails revenue after expenses unless offset by non-operational gains or exceptionally low cost structures.

Such profitability that outpaces gross sales prompts questions about earnings quality and sustainability. Without detailed segment disclosures or explanatory notes in public filings, it is difficult to ascertain whether this reflects one-time items such as asset monetizations, accounting treatments favoring recognition of gains, or a genuinely efficient operating model with minimal costs.

Although positive earnings reinforce operational viability on the surface, the unusual margin warrants caution in interpreting ongoing profitability under normal business conditions.

Liquidity Strength: Navigating with a Healthy Current Ratio

Turning to balance sheet metrics, AtlasClear demonstrates a sound liquidity position as indicated by its current ratio of approximately 1.56 [F1]. This metric—current assets divided by current liabilities—signals that the company maintains $1.56 in liquid and near-liquid assets for every dollar of short-term obligations.

Specifically, cash and equivalents alone contribute a substantial $23 million cushion [F1], providing runway flexibility for working capital needs, potential capital expenditures, or debt servicing without immediate liquidity strain.

This strong cash position could support operational stability and agile response to external shocks within the short to medium term. It also suggests prudent treasury management amid the company’s more opaque operational details.

Capital Market Activity: Investment Agreements and Dilution Risks

Recent publicly available information highlights dynamic equity market activity surrounding AtlasClear. Notably, news coverage points to trading interruptions alongside announcements regarding significant investment agreements and large share sale filings [N1], which together underscore active engagement in capital raising efforts.

Such transactions often introduce shareholder dilution risk as new equity issuance expands outstanding shares, potentially exerting downward pressure on existing ownership percentages if not matched by proportional value creation.

The presence of these developments — especially amid an unclear narrative about core operations — can heighten investor caution. Market participants may be left discerning whether these equity raises fund growth initiatives or serve more remedial financial needs.

Operational Opacity and Its Investment Implications

A salient challenge in evaluating AtlasClear lies in the near absence of disclosed sector classification or industry affiliations. This opacity creates significant hurdles in contextualizing financial results relative to peers or broader market dynamics.

Without clarity on what markets the company operates in or what products/services it provides, potential investors face difficulties assessing competitive risks, growth prospects, customer concentration, regulatory exposures, or cyclical sensitivities.

Such informational sparsity can dampen confidence in valuation exercises as assumptions must anchor more heavily on limited quantitative data rather than qualitative insights rooted in corporate strategy or operational milestones.

Assessing Risk Landscape: Volatility and Unknowns

According to recent SEC filings [S2], additional risks remain consistent with those outlined previously in their Annual Report—predominantly encompassing general market volatility and industry uncertainties. Importantly, there were no material changes reported during the quarter.

However, this baseline risk posture is compounded by the unknown unknowns intrinsic to firms with limited disclosure frameworks. The absence of detailed operational narratives invites speculation about latent risk factors unquantified publicly.

In combination with active liquidity management via equity issuances—as evidenced by recent filings—the risk profile includes both external marketplace fluctuations and internal transparency deficits.

Moat or Mirage: Does AtlasClear Have Durable Competitive Advantages?

The concept of a “moat” refers to sustainable competitive advantages that protect long-term profitability against rivals. For AtlasClear, public materials offer scant evidence supporting such differentiation.

Without industry context or insight into core competencies—be they proprietary technology, scale economies, network effects, regulatory exclusivity, or brand strength—the notion of a durable moat remains speculative at best.

This absence necessitates a more cautious stance; robust financial metrics are encouraging but insufficient alone without underlying defensible business attributes that mitigate competitor threats over time.

The Road Ahead: What Investors Should Watch

Looking forward, several key developments merit close attention from observers tracking AtlasClear Holdings:

- Upcoming SEC filings that might provide deeper operational disclosure or clarify segment contributions to revenue and profitability.

- Market response to ongoing stock sale activities and any shifts in ownership structure that could signal strategic direction changes.

- Management commentary around use-of-proceeds from capital raises to evaluate whether funds aim at growth investments versus balance sheet repairs.

- Any shifts in liquidity ratios or emerging balance sheet trends that could impact short-term financial resilience.

- Broader macroeconomic factors influencing sectors potentially served by AtlasClear once revealed.

The interplay between strong liquidity foundations juxtaposed with informational opacity creates a unique investment narrative—one requiring continual monitoring for clarifying signals amid evolving circumstances.

Disclaimer: This report is prepared for informational purposes only and does not constitute investment advice or recommendations regarding securities of AtlasClear Holdings, Inc. Readers should conduct their own due diligence before making any investment decisions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments