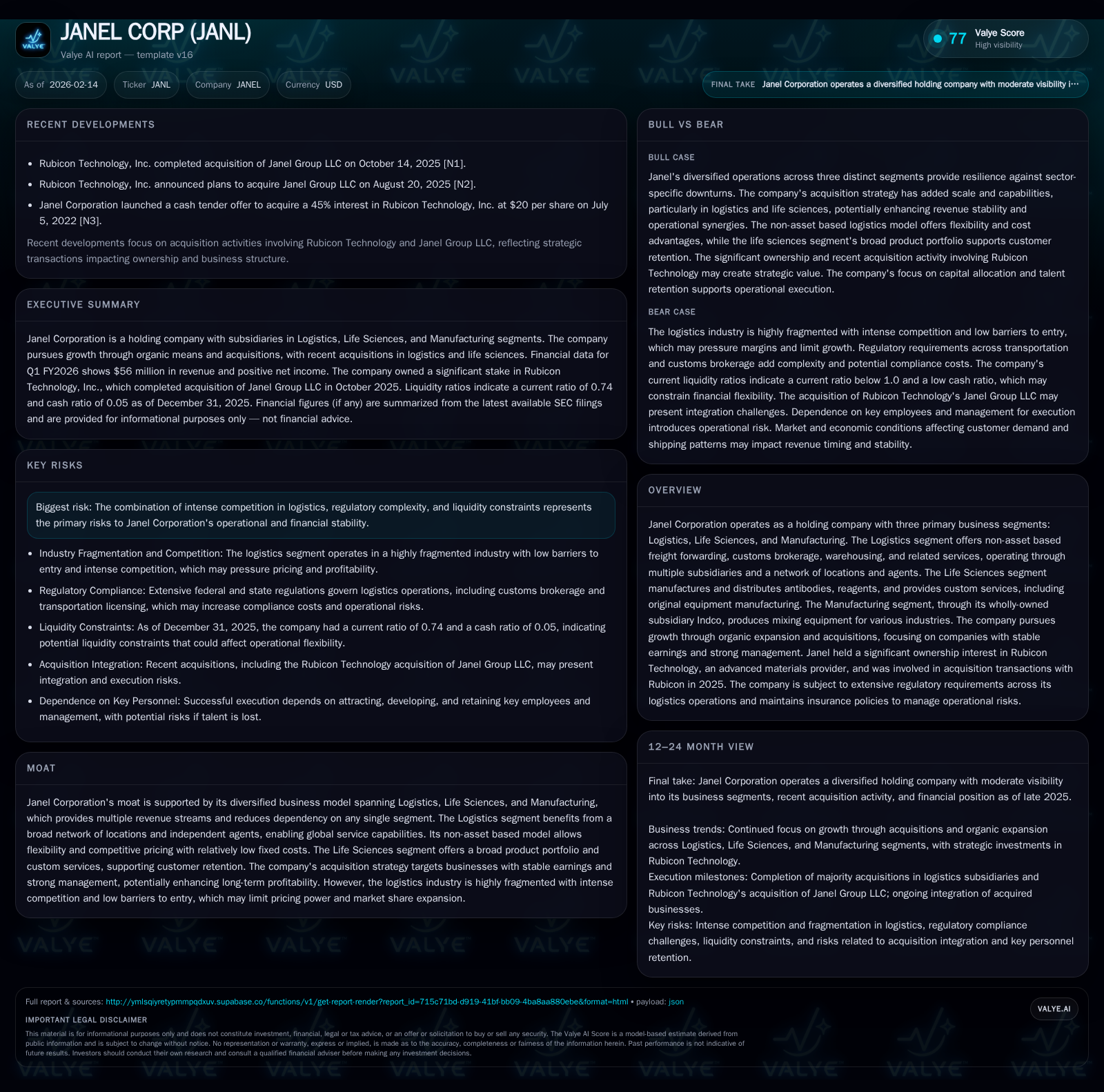

Janel Corporation: Balancing Diversified Holdings and Acquisition-Driven Growth Amid Financial and Integration Challenges

Janel Corp unfolds a multi-industry holding structure with strategic acquisitions underscored by operational complexity and liquidity constraints.

Janel Corporation operates as a holding entity across three distinct segments—Logistics, Life Sciences, and Manufacturing—each contributing unique revenue streams and operational dynamics. Its growth strategy heavily leans on acquisitions targeting stable earnings and strong management, yet this ambition brings notable integration risks and financial pressures evidenced by tight liquidity and slim profit margins. While the diversified model offers resilience against individual segment volatility, intense competition, especially in logistics, and the complexities of assimilation temper its strategic opportunities.

Janel Corporation at a Glance: An Intricate Holding Company

Janel Corporation presents itself not simply as an operator but as a conglomerate steward managing three quite distinct businesses under a single corporate umbrella. Founded in 2000 and headquartered in New York, Janel’s structure is fundamentally that of a holding company directing capital allocation, governance, and strategic growth for subsidiaries segmented into Logistics, Life Sciences, and Manufacturing [S1]. This arrangement inherently demands navigating the complexities that come with varied business models—from asset-light forwarding services to specialized scientific products and industrial machinery.

Central to Janel’s philosophy is diversification to mitigate dependence on any one segment. This approach theoretically stabilizes revenue streams against sector-specific headwinds but simultaneously imposes managerial challenges in harmonizing disparate operational demands. Capital allocation decisions within this holding framework are critical; the parent company must weigh growth capitalization opportunities in each segment against overarching financial health considerations.

Navigating Logistics: The Pulse of a Non-Asset-Based Powerhouse

Among Janel’s segments, logistics commands attention both through scale and distinctiveness. The segment operates primarily as a non-asset-based freight forwarder coupled with customs brokerage, warehousing, distribution, trucking, and ancillary value-added services [S1]. This model circumvents the capital-intensive risks typical of asset-heavy competitors by leveraging an extensive network of wholly-owned subsidiaries alongside independent agents.

The benefits are palpable: operational flexibility allows price competitiveness with relatively reduced fixed costs. For example, recent acquisitive moves such as securing majority ownership stakes in Airschott (80% acquired mid-2024) emphasize expanding footprint without traditional asset burdens [S1]. Yet such flexibility comes with tradeoffs; the freight forwarding industry is notoriously fragmented—with low entry barriers encouraging new players—and intensely competitive pricing environments that compress margins.

Additionally, the reliance on numerous agents across geographies necessitates intricate coordination to ensure service quality consistency. Accessorial revenues tied to fuel surcharges or handling fees provide incremental earnings but can add complexity to billing structures. The logistics segment’s success thus hinges on adept orchestration of both affiliate networks and customer relations amid fiercely contested markets.

Life Sciences & Manufacturing: Engines of Steady but Niche Revenue

While logistics dominates in terms of size and scale, Life Sciences and Manufacturing represent pivotal anchors supplying steadier niches insulated from cyclical logistics shocks. The Life Sciences segment manufactures antibodies, reagents, and provides custom original equipment manufacturing services—a portfolio offering bespoke scientific tools crucial in research applications [S1].

Manufacturing is chiefly represented by Indco, Janel’s wholly-owned unit producing mixing equipment selected by industries requiring precise material handling capabilities. This industrial niche roots itself in specialized engineering rather than commoditized product lines.

Together these domains underpin steady cash flows characterized by stable demand tempered by market specialization. Although their relative size is smaller compared to logistics ([F1]), their differentiated products help diversify operational risk amidst volatile transport markets. The reliance on custom solutions also aids customer retention through embedded client relationships difficult to replicate.

Acquisition Ambitions: Growth with High Stakes and Complexities

Janel’s growth narrative strongly emphasizes acquisition-led expansion focusing on targets with stable earnings trajectories and seasoned management teams [S1]. Recent deals illustrate this intent: besides Airschott, additional small-scale acquisitions enriched the customs brokerage network during 2025 [S1].

However, management openly acknowledges the array of risks inherent in this strategy—a candid admission uncommon in typical corporate disclosures but reflective of experiential lessons [S1]. Key challenges cited include difficulties assimilating operational cultures; disruptions causing short-term earnings dilution; increased working capital requirements stretched thin against existing liquidity; potential erosion of employee or client goodwill; plus exposure to unforeseen liabilities lurking within acquired entities.

Moreover, competitive pressures from larger financially endowed bidders complicate deal terms potentially inflating acquisition costs or reducing advantageous negotiation leeway. Such transactional complexity requires precise integration playbooks balancing speed against thorough diligence. Notably, goodwill impairment charges remain an ever-present concern given potential overpayments or underperformance post-acquisition.

Financial Health Check: Liquidity Hurdles and Profit Slimness

Pinpointing Janel’s financial contours reveals underlying fragility notwithstanding its ambitious scope. For fiscal year ending 2025’s Q4 interim filing [F1], total revenue clocks at approximately $56 million juxtaposed against net income a mere $419 thousand—translating to razor-thin profitability margins indicative of pricing pressure or elevated operational costs.

More worrying is the liquidity picture: current assets stand at roughly $94.9 million against $127.9 million in current liabilities yielding a current ratio around 0.74 [F1]. A ratio below one signals inability to cover near-term obligations purely from current assets prompting concerns about funding agility during growth phases or crisis episodes.

Cash reserves at about $6.7 million further underscore constrained buffers amid ongoing acquisitions demanding both working capital injection plus incremental overhead absorption [F1]. These metrics situate Janel precariously where missteps in operational execution or protracted integration timelines could exacerbate financial strain or necessitate external financing potentially at unfavorable terms.

Operational Risks Underneath Expansion Dreams

Delving deeper into operational contours exposes latent dangers tied squarely to expansion zeal. Management details aggregation stressors such as:

- Difficulties melding acquired entities’ personnel and systems into seamless operations,

- Temporary business interruptions risking client satisfaction or contract adherence,

- Resource diversion including managerial bandwidth stretched thin overseeing broadened portfolios,

- Upholding uniformity in procedural standards amid diverse subsidiaries,

- The dual challenge of safeguarding employee loyalty while integrating fresh hires,

- Potential impaired relationships lost from cultural friction,

- Heightened capital demands for newly added operations,

- Exposure to legacy risks subsidized within acquired balance sheets.

Such factors collectively suggest that aggressive growth without calibrated integration frameworks portends tangible risk amplification threatening sustainable operational excellence [S1]. Notably absent are union pressures helping preserve labor stability despite diversity in sectors serviced—a soft advantage mitigating some internal disruption probabilities.

Moat Realities: Diversification Strength vs. Sector Fragility

Janel’s moat appears conditional rather than impregnable—not rooted in overwhelming market dominance but sculpted through structural diversification which helps moderate systemic downturns across segments [S1].

The Logistics segment exemplifies fragility due to its high competition level alongside regulatory labyrinths impacting customs brokerage operations globally—anchoring limits on pricing leverage or rapid market share gains despite network advantages.

Meanwhile Life Sciences’ specialized products insulate against direct freight industry cyclicality but face their own competitive pressures from innovation cycles or dependency on niche customer bases.

Manufacturing side-steadies revenue streams yet does not escape demand sensitivity linked to broader industrial trends potentially subjecting it to capex fluctuations sector-wide.

Hence Janel’s protective advantage emerges less from dominating share than from spreading risk exposures appropriately—though this also caps exceptional upside potential inherent in monolithic standouts.

Strategic Management: Talent as an Unseen Competitive Edge

The human dimension subtly underpins Janel’s multifaceted operations yet often escapes headline focus. With no collective bargaining agreements fomenting labor relations stability across its workforce numbering just over 350 employees nationwide [S1], the company benefits from uninterrupted operations devoid of work stoppages or union-driven disputes.

Talent recruitment and retention remain priorities given reliance on specialized skill sets spanning complex logistics coordination to manufacturing engineering to life sciences technical competencies. Management highlights continuous process enhancements aiming to boost engagement productivity reflecting acknowledgment that intellectual capital constitutes essential intangible assets supporting competitive positioning amidst asset-light business models [S1].

This ‘soft asset’ foundation could prove decisive particularly when navigating integration complexities where human cohesion frequently dictates ultimate success transcending mechanical synergy theories alone.

Future Outlook: Opportunities Amidst Integration Uncertainties

Looking forward through a lens sharpened by disclosed risk factors invites cautious yet attentive appraisal. Acquisition strategies continue driving expansion prospects—but call for prudent cadence ensuring assimilation capabilities keep pace preventing operational disruptions evident historically [S1,S2,F1].

Liquidity improvement stands equally vital; shoring up working capital buffers would better position Janel for selective opportunistic investments while insulating against interest rate fluctuations stemming from broader economic cycles.

The diversified business model offers resilience providing multiple avenues for revenue generation though venturing into new industrial lines remains unproven territory warranting heightened scrutiny before material commitments.

Absent any material shifts outlined post recent SEC filings [S2], the company appears entrenched within its existing risk framework inviting vigilant strategic oversight balancing growth ambitions harmoniously with structural safeguards protecting long-run shareholder interests.

Disclaimer: This report is for informational purposes only reflecting data available as of February 2026 extracted predominantly from publicly filed SEC documents (10-K & 10-Q). It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments