Sino Green Land Corp.: Operational Depth Amidst Liquidity Struggles in the Global PET Recycling Arena

A detailed dive into Sino Green Land’s operational fundamentals and strategic challenges as it contends with severe financial constraints and complex corporate restructuring within the recycled plastics sector.

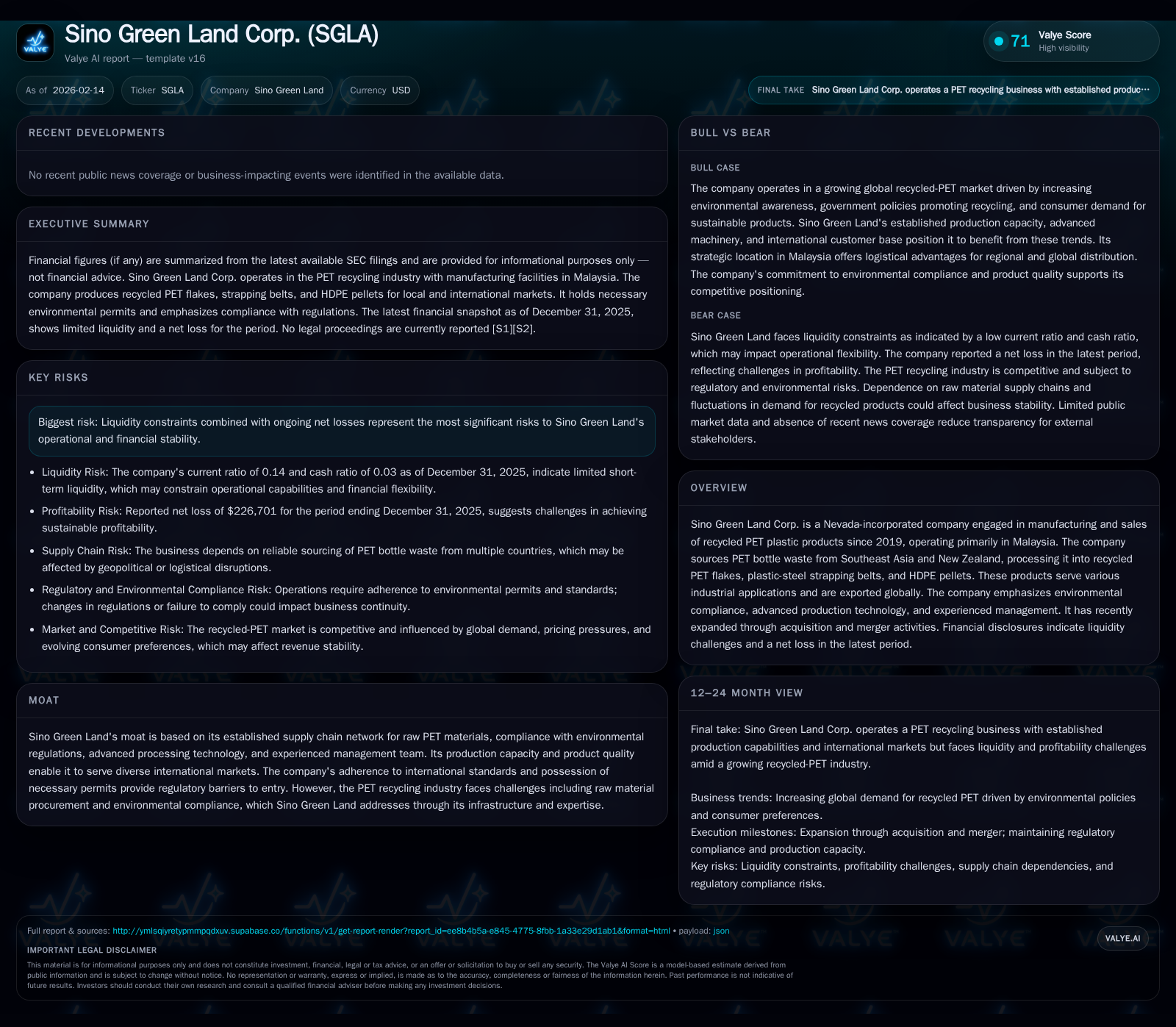

Sino Green Land Corporation, a Nevada-registered entity specializing in manufacturing recycled PET products from Southeast Asian and New Zealand plastic waste, operates primarily through its two factories in Malaysia. While its advanced processing capabilities and established sourcing networks create operational resilience, the company faces acute liquidity pressures evidenced by cumulative losses exceeding $6.5 million over recent years and a critically low current ratio of 0.14. Historical governance disruptions and recent corporate consolidations further complicate Sino Green Land's path forward. The limited working capital and identified internal control weaknesses underscore significant challenges to maintaining uninterrupted operations and meeting financial obligations, placing the company at a critical crossroads reliant on securing additional financing or strategic partnerships.

Navigating a Challenging Industry: Sino Green Land’s Core Business and Market Footprint

Sino Green Land Corp. operates within the highly specialized niche of recycled polyethylene terephthalate (PET) product manufacturing. Since shifting to this sector in 2019, the company has focused on processing post-consumer PET bottle waste—sourced predominantly from Southeast Asia and New Zealand—into usable industrial materials including recycled PET flakes, plastic-steel strapping belts, and high-density polyethylene (HDPE) pellets. These intermediate products serve various industrial applications globally through export channels.

The firm’s two Malaysian factories cover approximately 8,760 square meters combined — a modest industrial footprint that nevertheless supports diverse processed product lines. The choice of Malaysia as operational base leverages proximity to abundant raw material sources while also maintaining access to shipping lanes vital for global exports [valye_report_excerpt].

This operational model positions Sino Green Land distinctly within global recycling supply chains: it is not merely a local recycler but an international supplier dependent on seamless cross-border material flows. Its market footprint thus inherently involves managing complexities such as regional regulatory standards for recycled plastics, export compliance requirements, and varying raw material quality.

Unearthing the Company’s History: From Fruit Distribution to Plastic Recycling Revival

The company's corporate lineage reveals a tumultuous history impacting stakeholder perceptions and operational stability. Originally incorporated in Nevada in 2008 as Henry County Plywood Corporation, it initially engaged in plywood-related enterprises before undergoing strategic redirection.

Between 2009 and 2011, Sino Green Land pivoted sharply to wholesale distribution of premium fruits within China—a significant departure from its traditional business models. However, poor compliance with statutory filings led to a period of dormancy and regulatory scrutiny beginning around late 2011.

In late 2019, due to ineffective governance marked by an abandoned board of directors and revoked corporate charter status, the Eighth District Court of Clark County appointed Custodian Ventures LLC to take control. This custodianship brought Mr. David Lazar as sole officer/director but was dissolved by mid-2020 after settlement agreements enabled prior management's reappointment [S1].

The subsequent renaming episodes—from Henry County Plywood to Sino Green Land Corporation, temporary rebranding as Go Silver Toprich Inc., then reverting back—reflect instability but also an effort to consolidate focus on sustainability ventures.

This historical backdrop is not trivial: prolonged governance lapses affect investor confidence and operational credibility which are critical when navigating heavily regulated environmental sectors.

Moat in Practice: Supply Chain Mastery and Regulatory Compliance as Defenses

Despite financial headwinds, Sino Green Land demonstrates competitive strengths anchored in its procurement networks for raw PET materials across multiple countries — a facet few competitors can replicate with similar scale or consistency.

The company's commitment to environmental compliance manifests through securing necessary permits aligned with international standards—no small feat given varied regulatory landscapes across Southeast Asia—and investing in advanced recycling technologies designed for efficiency and product quality enhancement [valye_report_excerpt].

These capabilities collectively form barriers to entry: new market entrants face not only logistical hurdles in establishing PET waste sourcing channels but also steep costs in meeting environmental criteria critical for sustainable operations.

Moreover, Sino Green Land’s diverse product portfolio from flakes to specialty strapping belts reinforces operational flexibility allowing adaptation to fluctuating demand patterns internationally.

Liquidity Crisis Under the Microscope: Financial Data Reveals Operational Strain

The company's financial disclosures from fiscal year ending June 30, 2025, through December 31, 2025 paint a stark image of near-term survival challenges:

- A net loss totaling $1.81 million for FY2025 compounded by an incremental loss of $226,701 during Q2 FY2026 [F1][S1][S2].

- Operating cash outflows approaching $846k during FY2025 evidence limited internal cash generation capacity.

- Working capital deficits exceeding $4.44 million with current assets at $795k sharply overshadowed by current liabilities near $5.69 million translate into a current ratio of approximately 0.14—well below standard liquidity thresholds [F1].

- Accumulated deficit surpassing $4.7 million cumulatively erodes retained earnings base; shareholder equity sits at negative $2.39 million indicating insolvency pressures.

These metrics collectively triggered emphatic going concern warnings from both management disclosures and independent auditors.[S1] Such levels of net losses alongside restricted cash balances severely constrain the company’s ability to fund daily operations without external capital injections or debt restructuring.

In addition to jeopardizing operational continuity, this liquidity shortfall risks contract fulfillment delays—potentially damaging longstanding supplier/client relationships crucial to its moat.

Governance Overhaul and Control Weaknesses: Risk Factors Amplified

Underpinning these financial challenges are documented material weaknesses exposing vulnerabilities in internal controls over financial reporting — key among them:[S1]

- Absence of an independent audit committee coupled with a non-independent board structure undermining oversight integrity.

- Inadequate segregation of duties increasing risk exposure for errors or misstatements.

- Shortage of accounting personnel possessing requisite U.S. GAAP knowledge alongside insufficient training programs impairing timely compliance with SEC disclosure norms.

To address these deficiencies, management has proposed measures including appointing independent directors to establish a functional audit committee; redistributing responsibilities among finance staff; amplifying IT control systems; hiring qualified accounting professionals; and instituting ongoing specialized training initiatives.[S1]

While these plans represent needed remediation steps acknowledging governance gaps — their successful implementation depends heavily on available resources amidst ongoing liquidity constraints.

Importantly, unresolved control weaknesses heighten risk profiles regarding potential misstatements or reporting delays that could erode investor trust further.

Operational Vulnerabilities: Risks From Production Interruptions in Malaysia Operations

Operationally Sino Green Land's business model presupposes stable factory functioning given heavy reliance on continuous inputs like electricity and water essential for recycling processes.[S1]

Any interruption such as machinery breakdowns or utility shortages not only stalls production but risks breaching contract delivery commitments—with cascading effects on revenue generation.[valye_report_excerpt]

Additionally, limited immediate availability of replacement machinery parts exacerbates recovery timelines following equipment failures documented by management disclosures.[S1]

Given existing financial fragility limiting spare capacity investments or buffering mechanisms—inherent risks around factory downtime materially threaten ongoing viability.

Recent Corporate Consolidations: Merger Dynamics and Expansion Strategy

Notably expanding footprint through consolidation maneuvers occurred mid-2023 when Sunshine Green Land Corp., affiliated via controlling relationships with SGLA management teams, acquired Tian Li Eco Holdings Sdn. Bhd., a Malaysian eco-friendly enterprise.[S1]

Subsequent merger transactions folded Sunshine Green Land into Sino Green Land Corp., exchanging shares valued at over 160 million common stock units—maneuvers intended ostensibly to scale operations or streamline asset ownership structures.[S1]

While mergers typically imply growth or operational synergies potential—the timing amid acute cash flow deficits introduces execution risks especially related to integrating systems amidst strained resources.

The strategy may reflect bidirectional goals: diversification of product lines or geographic market depth versus managing distressed balance sheet issues through corporate restructuring.

Nonetheless these consolidations carry complexity burdens compounded by existing governance hurdles needing cautious navigation moving forward.

Long-Term Outlook: Potential Paths Through Financing Needs and Market Headwinds

Drawing from all tangible disclosures,[S1][F1][S2] Sino Green Land faces an uncertain trail ahead shaped largely by its ability to secure additional capital under reasonable terms—an element management itself underscores without assurance about future financings availability.

Several scenarios materialize:

- Success in raising equity or debt financing might stabilize operations temporarily but likely causes dilution or restrictive covenants impacting strategic flexibility.

- Failure leads inevitably towards asset liquidations or bankruptcy considerations given working capital deficits paired with recurring losses).

- Alternatively prolonged operational improvements implementing cost efficiencies coupled with partial resolution of governance issues might attract strategic partnerships offering balance sheet relief.

Industry-wide factors such as evolving global regulations around plastic recycling favor firms compliant with sustainability mandates but also increase compliance costs requiring robust capitalization—SGLA must reconcile these realities amid constrained funds.[valye_report_excerpt]

Thus while the operational foundation rooted in supply chain mastery provides essential footing—the interplay between financial distress signals management challenges critical junctures where decisive financing actions align closely with future viability chances.

This analysis is derived exclusively from publicly filed disclosures up to February 2026 without predictive commentary or investment recommendations. Readers should consider company filings alongside broader industry dynamics when assessing Sino Green Land's profile.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments