Kimberly-Clark’s Transformation and Liquidity Challenges in Consumer Staples

Exploring how Kimberly-Clark balances its iconic brand strength with current liquidity pressures amid an ongoing multi-year strategic overhaul.

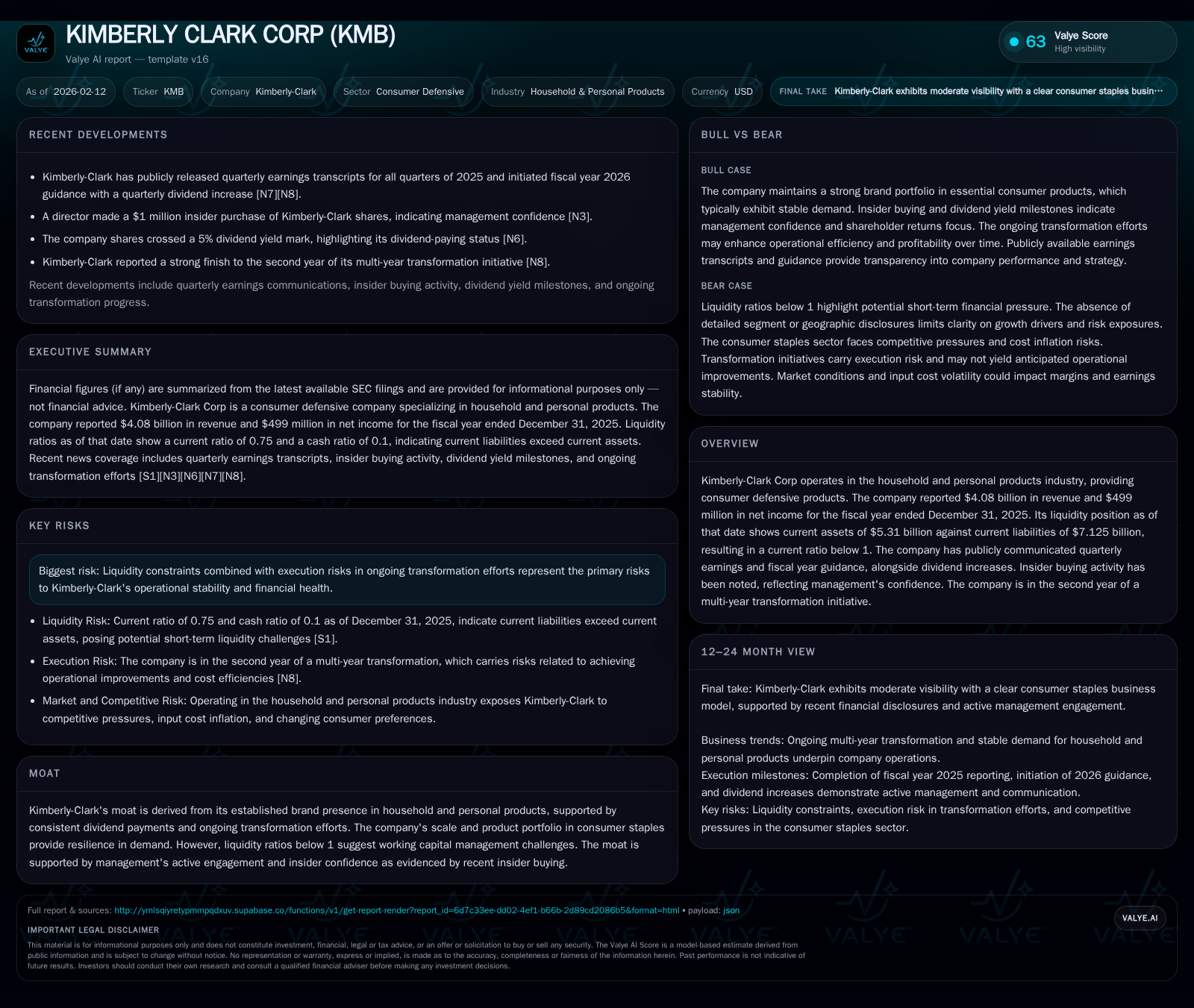

Kimberly-Clark Corp maintains a resilient market position anchored by strong brands and steady earnings, reporting $4.08 billion in revenue and $499 million in net income for fiscal 2025. Despite this, the company faces notable liquidity headwinds, reflected in a current ratio of 0.75, highlighting working capital strains. As it enters the second year of an ambitious transformation effort, management demonstrates confidence through dividend increases and insider buying, yet execution risks persist. Industry comparisons suggest Kimberly-Clark’s moat remains intact but will be tested by evolving market dynamics and financial pressures.

Legacy Strength Meets Modern Challenges

Kimberly-Clark Corporation stands as a venerable presence within the household and personal products sector, long associated with trusted brands that permeate consumers’ daily lives. In fiscal year 2025, the company generated $4.08 billion in revenue coupled with net income reaching $499 million [F1]. This financial footprint highlights entrenched demand for its consumer defensive goods despite a competitive landscape rife with product innovation and shifting buyer preferences.

Yet beneath this solid top-line performance lies a critical juxtaposition: Kimberly-Clark’s balance sheet reveals working capital pressures with current liabilities outstripping current assets ($7.125 billion vs. $5.31 billion), producing a current ratio of just 0.75 [F1]. This sub-1 metric raises immediate concerns about short-term financial flexibility—a crucial factor for companies reliant on efficient inventory and receivables management to fund operations without resorting to expensive external funding.

This tension between legacy strength supported by scale and brand equity versus emerging liquidity constraints frames the narrative context of Kimberly-Clark entering the next phase of its corporate evolution [S1].

Decoding the Latest Earnings: Beyond the Numbers

The Q4 2025 earnings report revealed nuanced aspects underscoring Kimberly-Clark’s operational landscape beyond headline figures [N4]. Revenue growth showed modest improvement driven partly by selective price adjustments in key categories amid inflationary cost headwinds. Pricing strategies appear calibrated carefully to avoid consumer backlash while preserving gross margins—a balancing act echoed in management’s commentary during the earnings call [N5].

Volume trends demonstrated mixed signals; some mature product lines saw stagnation or slight declines, offset by growth in innovative or premium segments. This dynamic underscores incremental shifts in consumer preferences forcing Kimberly-Clark to play catch-up with agile competitors.

Profitability margins reflected ongoing cost pressures tied to raw materials, logistics, and supply chain complexity, partially mitigated by efficiency gains from transformation efforts. The quarter’s results thus portray a company conditioned to incremental adaptation but vulnerable to margin compression if cost inflation persists uncontrollably.

Liquidity at a Crossroads: Current Ratios Under the Microscope

Delving into the balance sheet nuances presents a clearer picture of Kimberly-Clark's liquidity challenge. With $5.31 billion in current assets against $7.125 billion in current liabilities as of December 31, 2025, the resulting current ratio of approximately 0.75 signals working capital demands surpass available liquid resources [F1].

Analysis of management discussion highlights elevated payables levels potentially linked to extended supplier payment terms balanced against inventory build-ups needed for distribution efficiency [S1]. This scenario can create timing mismatches wherein cash outflows precede inflows more acutely than ideal.

The risk — underscored by SEC filings — revolves around sustaining day-to-day operational funding without triggering undue reliance on short-term borrowing or asset sales [S1]. Any disruption here could intensify financial strain, especially if transformation-related investments or market volatility pressure cash flows further.

Nonetheless, proactive liquidity management and incremental deleveraging remain focal points to stabilize this key financial metric moving forward.

Inside the Transformation: Progress and Pitfalls

Kimberly-Clark’s ongoing multi-year transformation initiative is designed as a fulcrum for future competitiveness—targeting operational efficiency improvements, supply chain modernization, and product portfolio rationalization [Valye_report_excerpt].

In dialogues from the Q4 earnings call, management emphasized progress milestones such as cost-saving programs capturing several hundred million dollars annually and digital enhancements aimed at consumer engagement [N5]. However, executives also cautioned about execution complexities, including integration risks associated with divestitures and shifting global trade dynamics affecting input costs.

The transformation carries dual-edged implications: if successful, it would reinforce Kimberly-Clark's moat against peers; if delayed or derailed, margin erosion and cash flow weaknesses could exacerbate present challenges [S1]. The company continues to allocate capital intelligently but within tight constraints imposed by existing liabilities.

Dividend Discipline and Insider Confidence Signals

In a notable move that underscores confidence despite liquidity headwinds, Kimberly-Clark raised its quarterly dividend alongside FY2026 guidance issuance [N6]. Maintaining dividend discipline speaks to strong free cash flow generation capabilities rooted in established brand loyalty—an essential investor appeal within consumer staples.

Simultaneously, recent insider buying activity injects an important behavioral signal reflecting management's positive outlook on intrinsic value prospects under transformation regimes [Valye_report_excerpt] [N14]. While seemingly counterintuitive given balance sheet stresses, these moves align with a long-term perspective anticipating stabilization post-transformation execution.

Yet sustainability of dividends hinges delicately on cash flow improvements addressing working capital inefficiencies without sacrificing strategic investment funding.

Competitive Landscape and Market Positioning

Comparisons with industry stalwarts such as Procter & Gamble accentuate both Kimberly-Clark's strengths and vulnerabilities [N13]. Whereas P&G has demonstrated agility through diversified product innovation and robust global scale driving double-digit stock appreciation recently, Kimberly-Clark navigates comparatively tighter margins amid less diversified exposure.

Post Holdings offers another relevant peer lens; its recent earnings beat driven largely by premium branded offerings spotlights evolving category leadership dynamics within consumer staples [N3]. Against this backdrop, Kimberly-Clark's well-known household brands benefit from entrenched consumer trust but require enhanced innovation velocity to maintain relevance.

The competitive moat remains solid primarily due to scale advantages and shelf-space dominance but is increasingly tested by nimble rivals leveraging digital channels faster and optimizing supply chains more effectively.

Risks That Could Shift the Trajectory

Key risk vectors converge on Kimberly-Clark’s near-term liquidity squeeze compounded by uncertainty around seamless transformation rollout [S1]. Execution risks include delays or higher-than-anticipated costs undermining margin recovery efforts.

Macroeconomic factors such as volatile commodity prices impacting pulp, energy costs for manufacturing facilities, transportation bottlenecks disrupting supply chains introduce further layers of unpredictability amid fragile global growth forecasts.

Additionally, unforeseen regulatory changes or shifts in consumer behavior (e.g., greater sustainability demands) could impose incremental capital expenditure needs or affect pricing power adversely.

Collectively these create a cautious risk environment that investors must monitor closely over coming quarters alongside company disclosures.

A Forward Look: Guidance and Market Expectations

Initiating FY2026 guidance concurrently with dividend increases reflects measured optimism from Kimberly-Clark’s leadership team regarding balancing growth aspirations with operational realities [N6] [N4].

Projected revenue trajectories anticipate moderate expansion supported by ongoing strategic pricing initiatives mitigating inflationary inputs—a theme consistent throughout past earnings dialogue [N5]. Net income outlook similarly assumes continued efficiency gains offsetting lingering cost pressures.

Market participants are digesting these cues cautiously; while some analysts highlight credible pathway improvements relative to prior years, skepticism persists given historical challenges executing multi-year transformations within large legacy organizations.

Hence forward-looking sentiment appears tempered yet open to upside surprises contingent upon delivery consistency.

Synthesizing Financials with Strategy for Valye Insights

Synthesizing quantitative data with strategic qualitative factors paints Kimberly-Clark as an archetype of an iconic consumer staple brand intertwined deeply into households globally yet currently navigating tight liquidity corridors.[Valye_report_excerpt][F1][S1]

Its $4+ billion revenue base coupled with near half-billion net income evidences steady though not spectacular profitability leveraged off brand equity cultivated over decades. However, suboptimal working capital metrics reveal operational frictions threatening agility necessary for sustained competitiveness.[F1]

The ongoing transformation initiative embodies both hope and hazard—holding promise if execution aligns well but posing downside risk should friction points prolong cash flow stress.[S1][N5]

Management's decision to increase dividends despite tight liquidity underscores confidence balanced with shareholder value orientation.[N6]

Relative positioning against industry giants like P&G indicates Kimberly-Clark retains a defensible moat via scale and brand but must accelerate innovation cadence alongside financial discipline to preserve market relevance.[N13][N3]

Altogether this mosaic illustrates a mature corporate athlete endeavoring not merely to endure but evolve amid structural challenges defining modern consumer staples ecosystems.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments