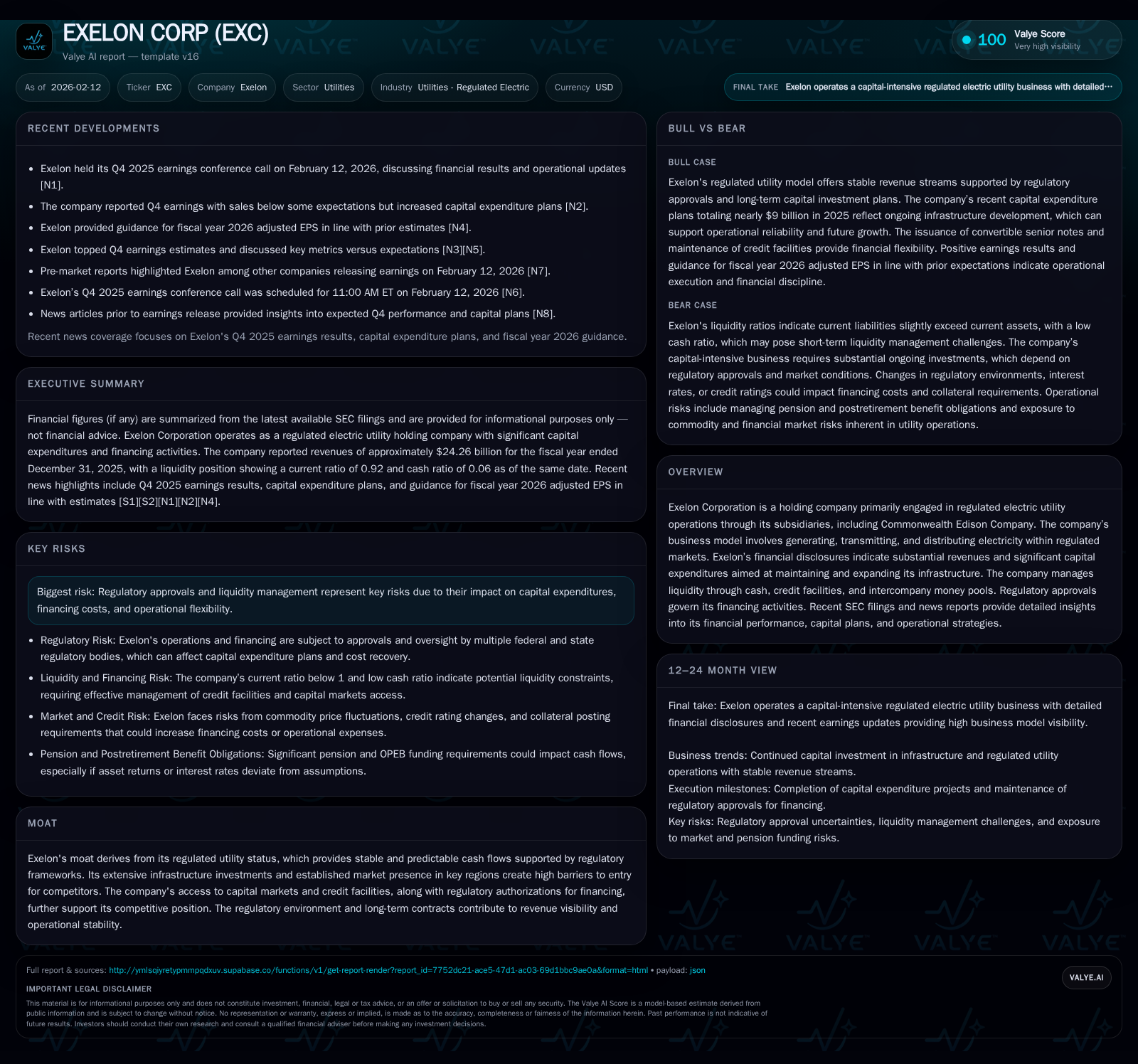

Exelon Corp’s Earnings Strength Amid Regulatory and Capital Challenges

Exelon posts a strong Q4 earnings beat while navigating tightened liquidity and regulatory rate case complexities.

Exelon Corporation delivered a better-than-expected fourth-quarter earnings performance in 2025, driven by favorable rate increases at major subsidiaries and supportive weather conditions, despite missing sales estimates amid softer demand. The utility giant's ambitious $9.95 billion capital expenditure plan for 2026 underscores its commitment to infrastructure modernization in a heavily regulated environment. However, rising operational expenses, interest costs, and regulatory uncertainties present ongoing challenges for liquidity management and financial flexibility. Exelon's moat remains firmly anchored in its regulated status, bolstered by stable cash flows and extensive infrastructure, even as it faces risks from credit market volatility and rate case outcomes.

Earnings Beat vs. Sales Miss: Decoding the Latest Quarter

Exelon’s fourth-quarter 2025 earnings report portrayed a tale of dual outcomes that reveal the nuanced dynamics of running a large regulated electric utility holding company. The consolidated net income attributable to common shareholders surged by approximately $308 million year-over-year, lifting diluted earnings per share from $2.45 in 2024 to $2.73 in 2025 on a GAAP basis. When adjusting for non-GAAP items such as severance-related cost management charges and regulatory disallowances, operating earnings stood at $2.77 per share — comfortably above consensus expectations [N1][N3][N4][S1].

This performance was primarily propelled by beneficial rate increases authorized at several key utilities within Exelon’s portfolio: Commonwealth Edison Company (ComEd), PECO Energy Company (PECO), Baltimore Gas and Electric Company (BGE), and Philadelphia Gas Works (PHI). Updated recovery rates for investments made to serve customers underpinned higher returns on regulatory assets particularly noted at ComEd. Favorable weather conditions at PECO also played a favorable role, as did lower storm costs at BGE.

However, the top-line electricity sales volumes missed analyst forecasts — mainly due to a decline in transmission peak load stemming from weakened peak demand at ComEd caused by cooler summer conditions or altered usage patterns. These variances underscore the inherent sensitivities utilities face linked to weather variability and end customer consumption behavior even within their regulated frameworks.

On the cost side, Exelon grappled with rising interest expenses charged to PECO, BGE, PHI as well as Corporate; increased depreciation tied to recent capital additions; heightened contracting costs mainly within PECO and PHI operations; plus charitable contributions from corporate operations which slightly weighed on net income figures [S1]. Despite these headwinds, the firm maintained robust profitability aided by its ability to recover costs through regulatory mechanisms.

Capital Expenditure Plans: Ambitious Investments in a Regulated Landscape

Exelon's declared capital expenditure budget of $9.95 billion for full-year 2026 signals its strategic emphasis on reinforcing and expanding its electric transmission and distribution networks as well as gas infrastructure where applicable [S1]. These investments are distributed across its principal utility subsidiaries: approximately $3.50 billion at ComEd focusing primarily on transmission ($1.10 billion) and distribution ($2.43 billion); $2.23 billion at PECO spread between transmission ($450 million), distribution ($1.38 billion), and gas ($400 million); BGE’s allocation surpassing $2.17 billion split among transmission ($1.08 billion), distribution ($575 million), and gas ($525 million); PHI plans totaling around $2.05 billion featuring substantial distribution spending [$1.25 billion] alongside gas upgrades [$50 million]; plus Pepco ($975 million) DPL ($625 million), and ACE ($450 million) contributing moderate shares [S1].

These figures reflect both routine plant additions aimed at maintaining grid reliability as well as modernization efforts addressing resiliency enhancements, renewable integration capacity expansions, and compliance with evolving environmental standards—activities that require regulatory approval for cost recovery assurances in eventual rate cases.

The scale of deployment reveals Exelon’s intention to sustain long-term operational stability while meeting increasing demand for clean energy transitions within its footprint.

Regulatory Rate Case Outcomes and Their Financial Implications

The lifeblood of Exelon's regulated business model lies in securing timely rate cases approvals that validate investments through adjusted tariff structures assuring cost recovery plus allowed returns on invested capital—a crucial revenue visibility driver [S1].

In 2025, settlements or updated recovery rates at ComEd, PECO, BGE, PHI illustrate progress but also illuminate inherent uncertainty embedded in these proceedings whereby disallowances or reconciliation adjustments can materially affect realized margins from projections.

For example, gains attributed to multi-year reconciliation plans effective at BGE helped offset previous shortfalls yet expose fiscal performance cyclicality depending on regulatory timing differences.

Furthermore, PECO experienced absence of prior Maryland multi-year plan reconciliations that negatively impacted comparative earnings results even as new approvals came into effect elsewhere.

This dynamic represents an ongoing balancing act whereby utilities like Exelon must judiciously engage regulators with transparent cost justification while anticipating challenges that could delay or dilute expected revenues.

Liquidity and Equity Distribution: Managing Cash Flow with ATM Programs

Managing liquidity amidst the sizeable capex pipeline necessitates diversified financing strategies beyond traditional debt issuance alone [S1][S2]. Exelon has harnessed At-the-Market (ATM) equity distribution programs since August 2022 developing up to $2.5 billion aggregate gross sales capacity extended through May 2028 replacing prior agreements capped at $1 billion.

During 2025 alone, approximately 16 million shares were issued under these programs yielding net proceeds of roughly $691 million dedicated broadly to general corporate purposes including growth capital needs [S1]. Accompanying these were multiple forward sale agreements totaling tens of millions of shares offering flexible settlement options—either physical delivery of stock or net cash/shares exchanges—at pre-agreed prices adjusted daily based on floating interest metrics.

Notably these forward sales introduce a nuanced consideration around potential dilution given their inclusion or exclusion from diluted EPS calculations depending on anti-dilution conditions prevailing during periods [S1][S2]. Forward transactions unrecognized until settlement reduce immediate balance sheet impact but evoke prudence concerning anticipated timing of equity raise events.

Capital markets remain critical to supporting liquidity alongside operating cash flows complemented by credit facilities which collectively underpin the company’s ability to fund investments without compromising financial stability.

Operational Challenges: Rising Expenses and Cost Management Efforts

Exelon's operational environment reflects mounting expense pressures that alongside lower energy demand shapes net profitability outcomes [S1]. Interest expense inflation is notable across most subsidiary entities plus corporate overheads linked mainly to capital structure changes or market rates shifts.

Concurrently increasing depreciation charges reflect asset base growth consistent with aggressive CAPEX activity while higher contracting fees apparently arise from outsourced services or maintenance contracts essential for system integrity.

Storm-related costs fluctuated regionally but remained contained relative to prior years — aided somewhat by mitigation strategies implemented earlier—yet still contribute variability in expenditure forecasting.

Management has pursued cost management initiatives; non-GAAP disclosures indicate severance-related restructuring charges connected to efficiency drives [S1]. Although such measures mitigate expense inflation partially they do not fully counterbalance upward trends driven by broader macroeconomic factors.

Moat Analysis: How Regulation Sustains Competitive Advantage

Exelon's enduring moat primarily stems from its regulated utility status creating significant barriers against new entrants thanks to exclusive service territories licenced by local commissions [valye_report_excerpt]. This regulation delivers stable cash flows grounded in predictable revenue streams derived from administered rate cases that adjust tariffs commensurate with prudent investments.

The company’s expansive infrastructure network dispersed across multiple regional utilities further reinforces competitive defenses making displacement prohibitively expensive for challengers.

Moreover access to capital markets along with credit facility backstops enabled by solid investment-grade ratings grants Exelon flexible financing avenues vital for sustaining large-scale capital expenditures mandated by policy shifts toward cleaner energy grids.

Long-term contracts embedded within regulatory frameworks promote revenue certainty which combined with operational efficiencies translates into defensible profitability cushions—even amidst sector transformations changing energy generation mixes.

Risk Spotlight: Credit Markets, Regulatory Uncertainty, and Capital Structure

Nevertheless Exelon confronts tangible risks tightly linked to regulatory outcomes that directly shape recovery timeliness of invested capital impacting liquidity forecasts [S1][S2]. Rate case decisions delayed or unfavorable would disrupt expected inflows constraining free cash flow generation potentially raising leverage metrics beyond thresholds tolerable for current credit ratings.

A downgrade scenario triggers heightened collateral posting obligations under PJM credit policies related mainly to power procurement contracts across subsidiaries like ComEd requiring additional liquidity buffers.[S1] Available credit facilities mitigate this risk somewhat but exposure size remains sizable relative to contingencies outlined.

Capital market volatility presents a wildcard influencing costs associated with new debt issuances or refinancing activities simultaneously complicating equity raise cadence through ATM program timing decisions.[S2]

Maintaining an optimal balance between debt leverage levels while deploying substantial growth-focused CAPEX demands vigilant financial stewardship amidst an evolving landscape fraught with policy shifts toward decarbonization targets potentially demanding heavier upfront spending before regulatory adjustments take hold fully.

Looking Ahead: Guidance, Market Expectations, and Strategic Priorities

Looking toward fiscal 2026 Exelon offers guidance aligning adjusted operating EPS around current market expectations validating the earnings trajectory modeled post Q4 release [N11][N14][valye_report_excerpt]. This steadiness provides reassurance amid ongoing execution risks yet reinforces commitment toward capital discipline balancing accelerated infrastructure renewal initiatives targeting grid resilience improvements across all major utilities.

Strategically the firm emphasizes leveraging regulatory relationships proactively ensuring alignment on reasonable cost recovery principles underpinned by transparent reporting complemented by continued efficiency gains through selective cost management strategies detailed during recent earnings calls [N2].

Investors watching this nexus appreciate how Exelon's regulated positioning affords both cyclical defense characteristics tied to stable cash flows coupled with growth opportunities driven by mandated network modernization reflecting essential societal demands transitioning energy landscapes favorably yet complexly.

Disclaimer: This analysis is intended solely for informational purposes based on publicly available data as of early 2026 without offering buy/sell/hold recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments