CSP Inc’s Strategic Service Pivot and AZT PROTECT Pipeline Drive Margins Amid Financial Tightrope

Despite modest recent profits, CSP Inc is reshaping its business model around service expansion and proprietary pipeline products to tackle margin pressures.

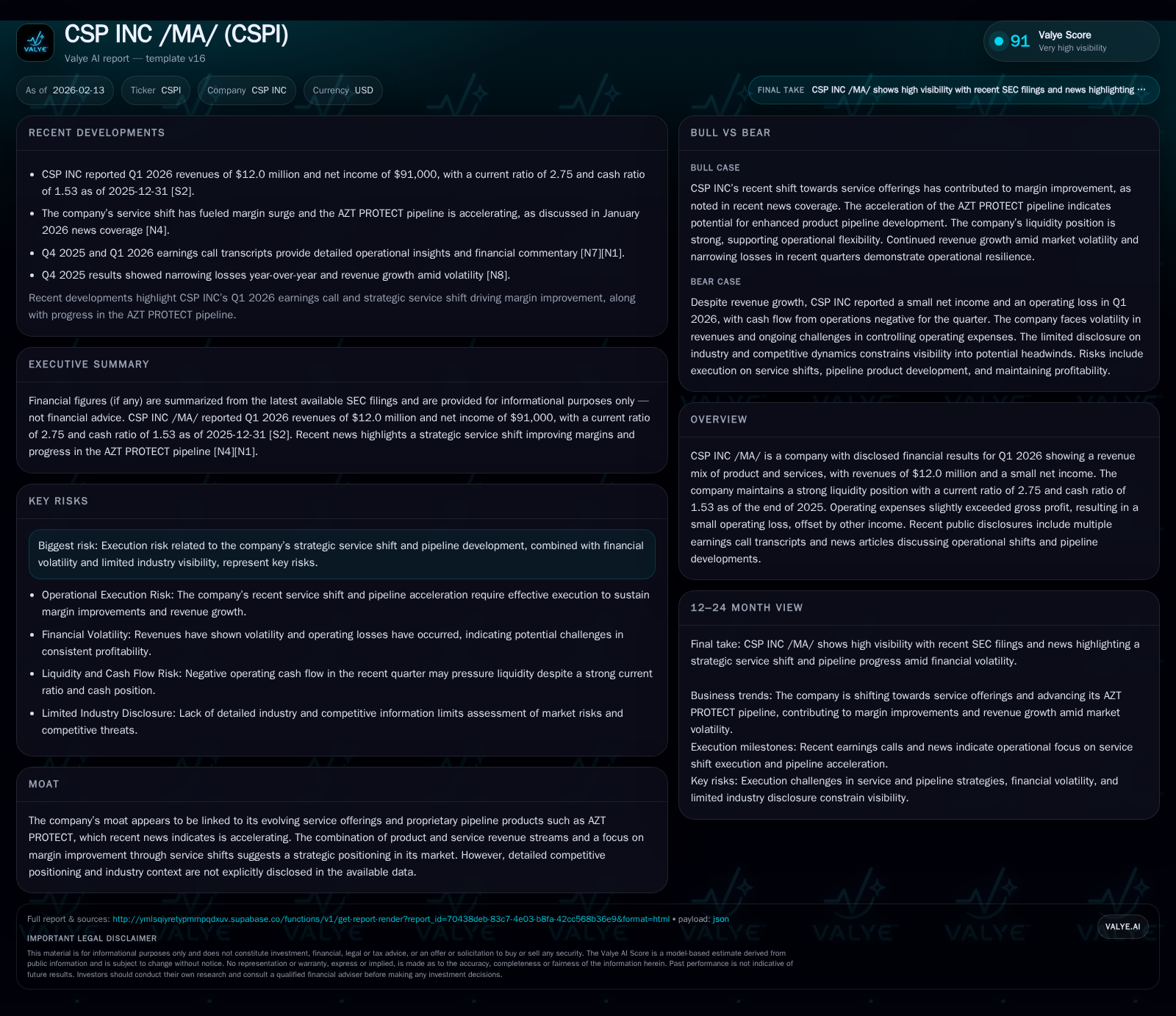

CSP Inc’s Q1 2026 financials reveal a company at an inflection point, balancing small net income against operational losses offset by other income and robust liquidity. The strategic pivot from product-heavy revenue to enhanced service offerings appears central to margin improvement efforts, coupled with the accelerating AZT PROTECT pipeline asset. However, risks tied to execution and limited public industry context underscore challenges ahead. This analysis explores how these dynamics interplay within CSP’s evolving positioning and outlook.

Turning the Page: CSP's Transition from Product Focus to Service-Driven Growth

CSP Inc's latest disclosures articulate an explicit strategic pivot—shifting emphasis from traditional product sales toward expanding its services portfolio. This transition reflects an adaptive response to margin pressures inherent in hardware or product-driven models. In the Q1 2026 earnings call, management underscored the growing contribution of service contracts and managed offerings as "central to unlocking sustainable profitability" [N1]. Complementing this narrative, a January 2026 Nasdaq feature highlights how CSP's "service shift fuels margin surge," spotlighting this ongoing evolution as a cornerstone initiative [N2]. This repositioning is not mere lip service but accompanied by structural changes detailed in filings that show increasing allocations toward service development and support capabilities [S1].

Such shifts aim to leverage recurring revenue streams that typically command better margin profiles than one-off product transactions. Indeed, the management team described services as "a platform for consistent cash flow generation" amid fluctuating demand for core products [N1]. This balance between legacy product sales and emergent services forms a dual engine propelling CSP’s growth trajectory while addressing cost inefficiencies.

Decoding the Numbers: Analyzing Q1 2026 Financials in Context

At first glance, CSP’s reported financial results paint a picture of constrained profitability with $12 million in total revenues alongside a slim net income of $91,000 for Q1 2026 [F1]. However, deeper inspection reveals nuanced dynamics underpinning this modest bottom line. Operating expenses notably surpassed gross profit during this period—an indication of ongoing investments or cost pressures within operations—yet were partially offset by other income sources such as possibly investment returns or non-core gains disclosed in the filings [S2].

The liquidity position emerges as an undeniable positive for CSP. As of December 31, 2025, current assets stood at approximately $49.15 million compared with current liabilities around $17.86 million—yielding a solid current ratio of roughly 2.75 [F1]. Such metrics demonstrate strong short-term solvency and hint at prudent balance sheet management amid operational headwinds. Moreover, cash and equivalents alone totaled nearly $25 million, affording substantial buffer for fund allocation flexibility [F1]. These figures provide reassurance that CSP can sustain its strategic pivots without immediate financing distress.

Nevertheless, the narrow profit margins juxtaposed with elevated operating expenses suggest delicate financial balancing acts are underway. Analysts must parse through these tensions when assessing CSP's near-term stability.

The Moat in the Making: AZT PROTECT’s Role and Pipeline Prospects

A defining element distinguishing CSP within its competitive set is its proprietary pipeline asset—AZT PROTECT—which recent reports assert has "accelerated considerably," fueling optimism about its role in CSP's moat-building strategy [N2]. This proprietary product appears designed not only as a revenue driver but also as a differentiation lever amid commoditized market offerings.

Filings corroborate AZT PROTECT’s strategic importance; references indicate R&D focus aligned with scaling this asset and integrating it into broader solutions portfolio [S1]. Management commentary points toward AZT PROTECT as "a critical pillar supporting revenue diversification and expanding customer value propositions" [N1]. While explicit competitive comparisons remain undisclosed publicly, the emphasis on proprietary pipeline enhancement signals management's belief in building defensible market positions rather than competing solely on price or volume.

From an industry perspective (analysis), proprietary products like AZT PROTECT can carve out sustainable advantages if supported by patents or unique technical features requiring specialized know-how—though execution quality ultimately governs realization.

Margin Dynamics: How Service Shift Fuels Profitability Gains

Margins tell the story behind revenue figures—and here CSP evidences notable margin dynamics attributable primarily to its pivot toward services. The Nasdaq coverage explicitly links "margin surges" directly to increasing portion of service revenues whose cost structures differ materially from products [N2]. Services often benefit from higher incremental margins given lower materials intensity and opportunities for scaling existing platforms.

Earnings call remarks further flesh out these operational levers: "Our team has strategically rebalanced offerings toward managed services resulting in improved gross margins even while total operating costs remain under pressure" [N1]. The slight operating loss recorded despite revenue growth serves as a reminder of transitional friction as new cost bases align with evolving business mix.

This shift illustrates typical industry patterns where companies gradually move up the value chain—from hardware sales toward integrated service ecosystems—to capture more profitable revenue streams while deepening customer relationships.

Balancing Act: Liquidity Strength Vs. Operating Losses

CSP walks a financial tightrope marked by robust liquidity yet persistent operating challenges. The strong current ratio of 2.75 accompanied by substantial cash reserves ($24.9M) provides breathing room and operational cushioning [F1]. In contrast, operating expenses marginally outpaced gross profits causing a small operating loss mitigated by additional income components—a pattern signaling subdued core business efficiency currently but manageable via liquidity buffers [S2].

Asset composition highlights moderate investments in property/equipment (~$0.5M) with intangibles related to pipeline products remaining low but stable—suggesting restrained capital expenditures aligned with strategic priorities rather than aggressive expansion this cycle [F1][S2]. Current liabilities remain controlled relative to assets though accounts payable exhibited increase likely tied to operational ramp-up or contract fulfillment demands.

Ultimately, maintaining this equilibrium between sufficient runway and optimizing operating leverage will be key for sustaining momentum without jeopardizing financial resilience.

Risk Radar: Navigating Execution and Industry Visibility Challenges

Key risks loom prominently over CSP’s transformative phase. The company candidly acknowledges execution risk tied to scaling service offerings alongside advancing the AZT PROTECT pipeline—a high-stakes endeavor requiring coordinated deployment across R&D, marketing and operations functions [S1][S2]. These internal complexities coincide with limited industry transparency; scarce detailed competitive data constrains benchmarking efforts by investors and analysts alike—a noted friction point outlined in Valye Newsbriefs reflecting on CSP’s sector opacity [valye_report_excerpt].

Financial volatility resulting from narrow margins underlines sensitivity to unexpected disruptions or protracted adoption curves for new services/products. Furthermore, dependence on relatively nascent proprietary products intensifies uncertainty regarding commercial traction timelines.

In sum, while growth opportunities exist distinctly via strategic pivots, they are tempered sharply by execution complexity and informational asymmetry challenges surrounding industry landscape interpretation.

Market and Analyst Perspectives: What Recent Commentary Reveals

Investor discourse framed around CSP has picked up nuances post recent earnings releases and news coverage. Select analyst blogs aggregated by Nasdaq highlight CSP among companies demonstrating intriguing transformation potential amidst broader market uncertainty [N6][N7]. Commentary generally portrays cautious optimism anchored in visible progress driving margin rebound possibilities but coupled with calls for vigilance given financial tightness.

Comparative analyst insights underline that while innovations such as AZT PROTECT materially differentiate CSP’s narrative relative to peers lacking similar proprietary assets, tangible evidence remains needed on scale economics realization before sentiment can shift decisively positive.

This balanced understanding among market practitioners reflects maturity recognizing growth ambitions without discounting operational realities inherent in change initiatives.

Looking Ahead: Strategic Priorities and Potential Catalysts

Looking forward into late 2026 and beyond, CSP’s management agenda coalesces around several interlinked priorities: accelerating acquisition of recurring service revenues; advancing commercialization stages of AZT PROTECT while broadening applications; optimizing cost structures aligned with new business mix; fortifying liquidity stance; and enhancing disclosure clarity to reduce informational hurdles for stakeholders [N1][N2][S2].

Potential catalysts include successful scaling milestones announced on forthcoming earnings calls or regulatory updates enhancing pipeline assets’ value proposition. Incremental margin improvements driven by expanding high-profit service contracts may create self-reinforcing momentum easing investor confidence concerns.

Yet sustaining this pathway demands executing complex transitional strategies flawlessly within competitive markets often characterized by rapid innovation cycles—a challenge CSP appears conscious of navigating carefully.

Disclaimer: This analysis synthesizes publicly available information up to February 2026 without projecting future stock performance or making investment recommendations. Readers should conduct independent due diligence considering their own risk tolerance and consult professional advisors before making any financial decisions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments