IB Acquisition Corp.: Navigating the SPAC Landscape Amid Financial Strains and Strategic Uncertainty

An in-depth analysis of IB Acquisition Corp.'s SPAC journey spotlighting its operational void and financial challenges through 2025.

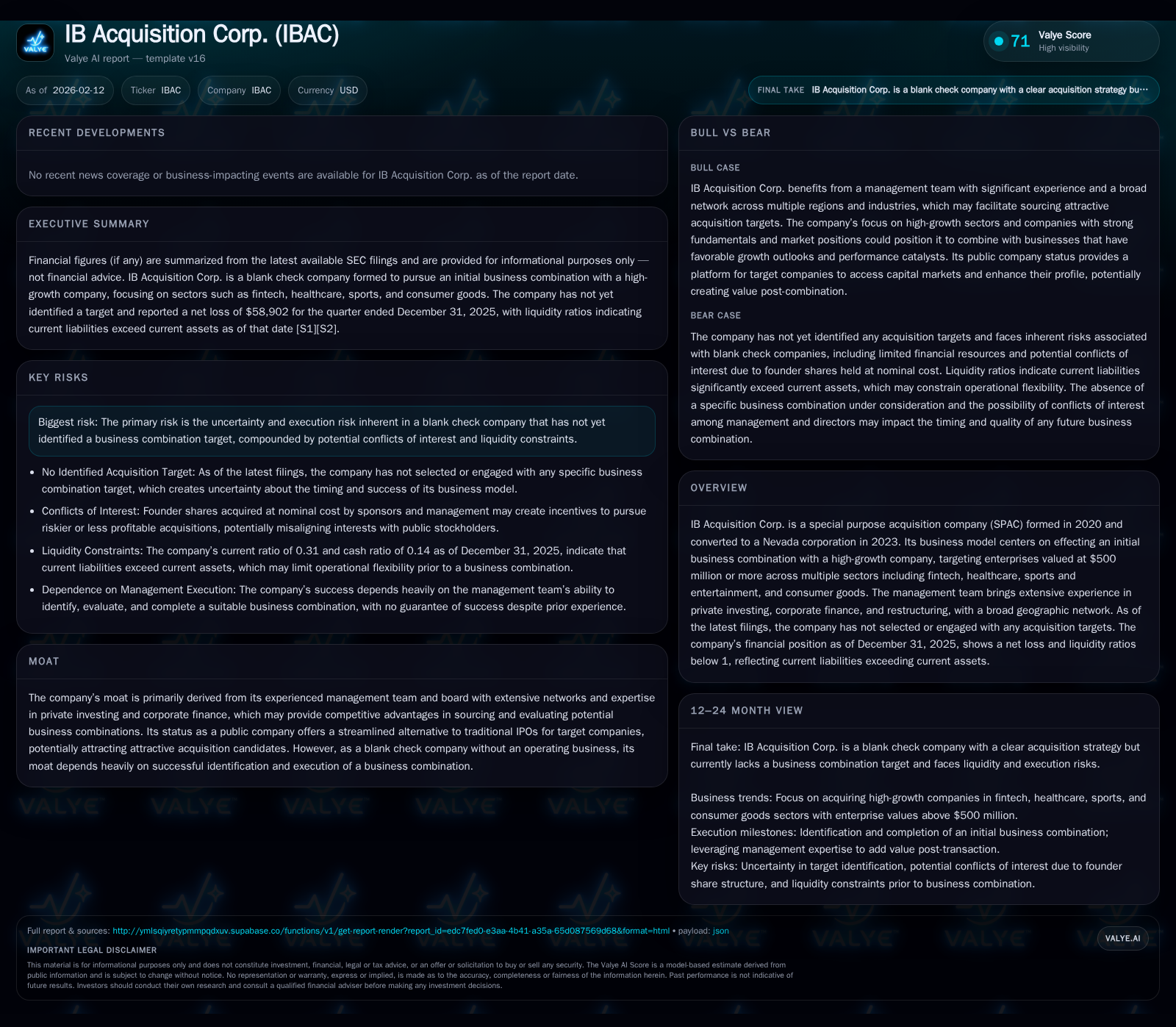

IB Acquisition Corp. was established in 2020 as a special purpose acquisition company with ambitions to acquire high-growth firms across diverse sectors. Despite an experienced leadership team and a broad investment mandate, the company has yet to identify or execute any business combination, resulting in ongoing operational losses and mounting liquidity pressures by the end of 2025. This analysis explores the paradox between the inherent promise of SPACs and IBAC’s current financial and strategic realities within a challenging macroeconomic environment.

Ambitions on Paper: The Story Behind IB Acquisition Corp.

IB Acquisition Corp. entered the burgeoning SPAC universe at a time when blank check companies were viewed as rapid conduits for taking promising private businesses public. Originally incorporated under Delaware law in mid-2020 and re-incorporated in Nevada in September 2023, IBAC laid out an ambitious multi-sector investment symmetry targeting enterprises with valuations north of $500 million.[S1] Its remit spans fintech innovation, healthcare advancements, sports and entertainment ventures, and consumer goods — sectors characterized by growth potential and investor interest. While this wide scope reflects flexibility, it also signals the challenge of mastering distinct industries.

The company's stated strategy revolves around leveraging public market access to strike transformative deals via mergers or asset acquisitions.[S1] This model is emblematic of SPACs’ core appeal: offering companies an alternative IPO path with potentially less friction. However, as we shall see, this promise contends with practical hurdles buried beneath the surface optimism.

The Team Behind the Ticker: Experience vs Execution

IBAC’s leadership consists of seasoned executives blending entrepreneurial success with deep corporate finance roots. Chairman and CEO Adelmo “Al” Lopez brings a track record encompassing founding Alma Coffee along with executive roles at Blair Corporation and Dole Fresh Fruit International.[S1] CFO Christy Albeck complements this with advisory expertise across pre-IPO consulting and outsourced CFO services — bridging financial diligence and strategic counsel critical for navigating public company demands.[S1]

Vice Chairman John Joyce adds gravitas from his former CFO tenure at IBM coupled with senior roles at SilverLake Partners.[S1] Additional board members and advisors bring diversified domain knowledge spanning biotechnology leadership (Silvia Panigone), venture capital (Jian Zhang), and Asian market insights (Feng Xiangkun).[S1] Collectively, this constellation presents a theoretically robust moat based on relationships with founders, CEOs, sponsors, and private equity stakeholders across global markets.

Yet, crucially, these credentials have yet to translate into tangible business outcomes through target identification or deal execution. With no operational revenues or acquisitions announced as of late 2025,[S1] this imbalance underscores a gap between managerial potential and realized progress.

Counting Cash & Costs: Financial Realities Beyond the SPAC Premium

Financial disclosures tell a more sobering story beneath initial capital infusions. IBAC raised approximately $115 million from its March 2024 IPO alongside roughly $6.1 million from private placement units sold to sponsors.[S1] After underwriting discounts and offering expenses exceeding $7.7 million,[S1] net proceeds intended for business combinations initially painted a promising capital base.

However, by September 30, 2025—the end of their fiscal year—the trust account balance earmarked for acquisitions dwindled to about $15.9 million,[S1] reflecting some erosion likely related to permissible withdrawals for taxes or expenses. Fast forward to December 31, 2025; cash reserves plunged dramatically to near $165 thousand with total current assets amounting to approximately $362 thousand versus current liabilities topping $1.16 million—yielding a current ratio near 0.31.[F1]

This severe working capital deficit reveals mounting operating costs linked to public company obligations—legal fees, audits, compliance—and due diligence activities without revenue offsets.[S1][F1] Moreover, net income turned negative ($-58,902) by year-end December 2025,[F1] marking an inflection from earlier modest net gains sourced solely from trust account interest income.[S1]

These figures highlight an increasingly precarious financial footing where cash burn outpaces inflows amid protracted target searches.

The Elusive Hunt: No Targets, No Revenues, No Operating Business

By definition, IBAC functions as a shell without producing operating revenues absent consummated business combinations.[S1] As of the latest filings ending December 31, 2025,[F1] no acquisition targets have been publicly disclosed or engaged. This situation entrenches several challenges:

- Absence of revenue streams makes sustaining operations dependent on cash reserves.

- Investor returns remain contingent on completing transactions yielding growth or synergies.

- Extended delays elevate risk profiles given typical SPAC lifespan constraints.

While such inertia is not unusual in many SPACs facing competitive bidding conditions or market uncertainty,[analysis] it nevertheless magnifies stress on stakeholders awaiting value creation triggers.

Risks in Focus: Liquidity Crunches and Competitive Moats That Are Not Yet Built

IBAC’s risk disclosures candidly acknowledge hazards endemic to blank check vehicles.[S1][S2] Key risks include:

- Execution risk tied to failure or delay in closing initial business combinations which underpins their entire raison d’être.

- Liquidity challenges evident from cash depletion coupled with disproportionately higher current liabilities relative to assets undermining operating flexibility.[F1]

- Potential conflicts of interest arising from sponsor roles or transaction incentives that may not align fully with public shareholders.

- Sensitivity to macroeconomic fluctuations—interest rate rises increase financing costs; inflation pressures elevate expense baselines.

The company views its "moat" primarily as managerial experience combined with expansive networks facilitating sourcing pipelines—but such competitive advantages remain theoretical until demonstrated via successful transactions.[S1]

Market Context: Economic Headwinds Against SPAC Success

Broader economic dynamics compound internal execution challenges confronting IBAC.[S1] Persisting inflation globally raises costs; rising interest rates dampen valuation multiples that underpin deal economics; geopolitical volatility impacts investor confidence broadly.

Such headwinds have notably cooled general enthusiasm for speculative investment vehicles like SPACs post their pandemic-era surge,[analysis]. Consequently, securing agreements at attractive terms has become tougher requiring more deliberate deal structuring — an obstacle for companies like IBAC that have yet to announce definitive partnerships.

What’s Next? Scenarios for IBAC’s Path Forward

Drawing exclusively from disclosed data,[S1][S2][F1], plausible near-term trajectories include:

- Successful Business Combination Completion: Leveraging remaining trust funds supplemented by capital stock or debt issuance could consummate targeted deals restoring growth prospects and addressing liquidity strains.

- Extension or Capital Raise: The company may seek shareholder approval for life extension or new capital injections critical given low cash balances relative to imminent liabilities.

- Wind Down / Liquidation: Should inability to identify viable partners persist alongside depleted resources, management might pursue orderly liquidation returning residual funds after settling obligations.

Each pathway underscores stark operational imperatives intertwined with external market receptivity — illustrating how theoretical promise morphs into tangible outcomes only upon strategic execution.

This report synthesizes publicly available SEC filings up to February 12, 2026,[S1][S2][F1] combined with contextual market analysis aimed at informing buy-side professionals considering blank check company dynamics. It is not investment advice but rather an exploration of IB Acquisition Corp.'s unique position at the intersection of SPAC opportunity sets and pragmatic financial constraints.

Comments