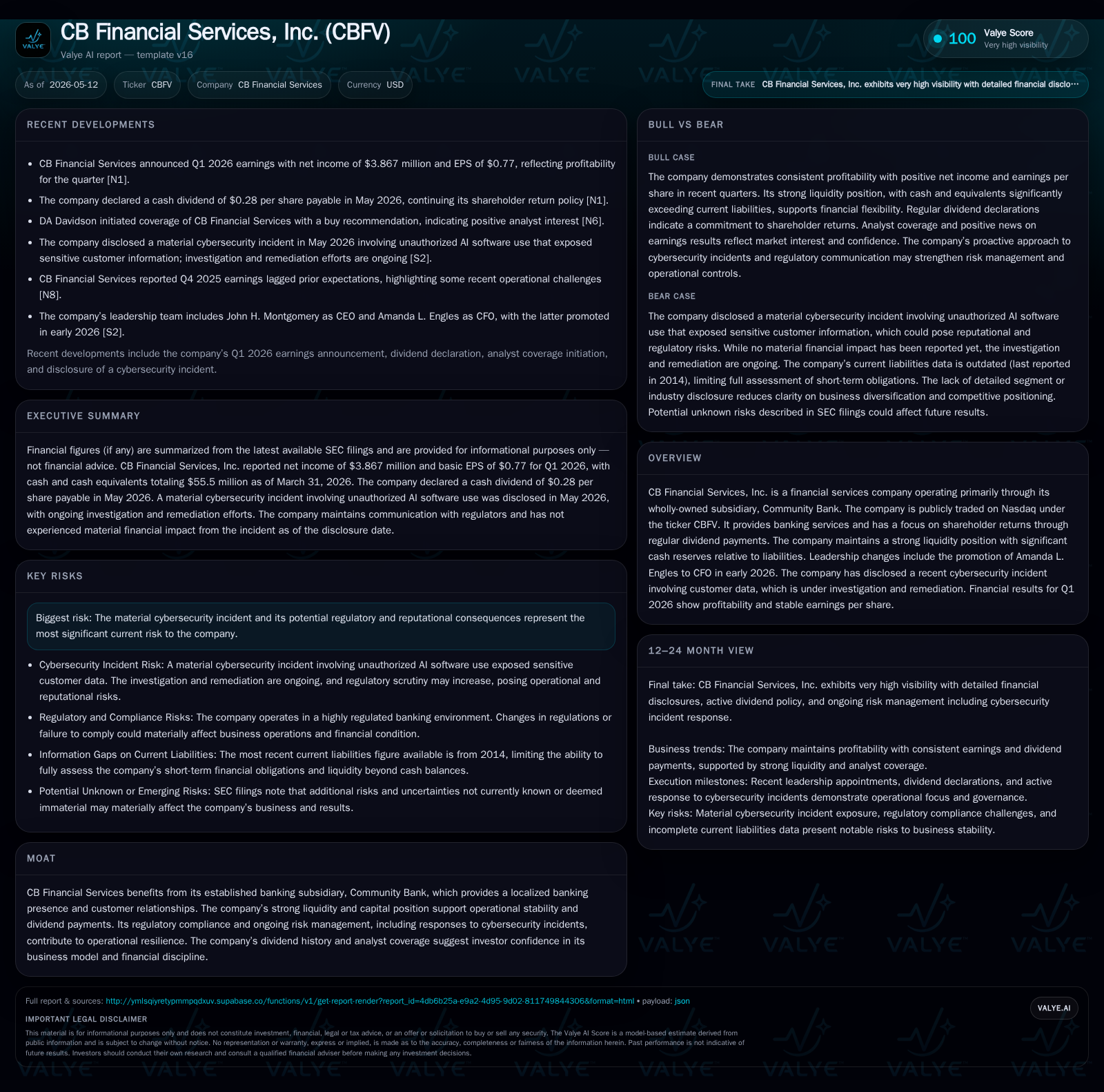

CB Financial Services Strengthens Stability Despite Cybersecurity Challenge

Q1 2026 results demonstrate solid profitability and liquidity, even as the company addresses a material cybersecurity incident.

CB Financial Services, through its wholly-owned Community Bank, reported profitability in Q1 2026 with stable earnings per share and a strong cash position. However, a May 2026 internal cybersecurity incident involving unauthorized AI software access to sensitive customer data has introduced reputational and regulatory risks. The bank's established community banking model underpins its operational resilience and dividend consistency amid evolving industry dynamics. Going forward, remediation efforts and regulatory responses will be critical near-term factors to monitor.

Q1 2026 Update: Profitability Amid New Challenges

CB Financial Services, Inc. (Nasdaq: CBFV), operating primarily through its wholly-owned Community Bank subsidiary, reported solid financial results for the first quarter of 2026. The quarterly filing dated May 12, 2026 (Form 10-Q) reveals that the company sustained profitability with stable earnings per share figures [S2]. Notably, CB Financial Services beat market Q1 earnings estimates according to recent Nasdaq reports [N1][N2]. This continued earnings track record underscores operational stability driven by Community Bank's core banking services.

However, shortly after the earnings release, CB Financial announced a material cybersecurity incident occurring at Community Bank on May 5, 2026 [S3]. The bank detected unauthorized use of an artificial intelligence-based software application accessing non-public customer information including names, social security numbers, and dates of birth. While operational disruptions were avoided—customer account access and core IT infrastructure remained intact—the sensitive nature of the exposed data prompted the company to classify the event as material.

Community Bank promptly secured affected data and engaged external cybersecurity advisors to contain the breach. Notifications are underway in accordance with federal and state laws as well as regulator guidance. At the time of disclosure on May 7, the incident’s full scope and root cause investigation were ongoing. The company does not anticipate an immediate material financial impact from this event but flags it as a salient risk factor moving forward.

Business Model and Product Offering of Community Bank

CB Financial Services generates revenue almost exclusively via its wholly-owned Community Bank subsidiary [S1]. This subsidiary operates in a regional community banking model focusing on retail deposits, commercial loans, mortgage lending, and ancillary banking services tailored to local consumers and small businesses. Revenue derives principally from net interest income generated by its loan portfolio offset by interest paid on deposits.

The bank cultivates enduring customer relationships within defined geographic territories, creating notable switching costs which support deposit stickiness and credit demand stability. Such localized market expertise also affords modest pricing power versus larger national competitors especially in specialized lending segments. Fee-based revenue from services like transaction processing adds incremental diversification.

Community Bank’s consistent profitability feeds into CB Financial’s dividend distribution policy—an important aspect of its shareholder value proposition emphasized in investor communications [S2]. Liquidity management appears conservative with substantial cash reserves aggregating to $55.5 million as of quarter-end March 31, 2026 [F1], enabling both operational stability and return of capital initiatives.

Competitive Environment and Industry Dynamics

The community banking sector where CB Financial operates is fragmented yet facing pressure from consolidation trends among regional banks alongside rapid fintech innovation disrupting traditional product delivery models [S1]. Fintechs increasingly challenge deposit acquisition and payment processing niches with technology-centric offerings.

Despite this competitive shakeup, Community Bank leverages entrenched local reputation and regulatory compliance rigor to maintain franchise strength. The absence of debt on the balance sheet as indicated in recent data further reduces refinancing or leverage-related vulnerabilities [F1]. However, regulatory oversight remains intensive post-2008 reforms especially concerning cybersecurity protocols—a domain now under acute pressure with the recent breach.

Cost pressures from compliance mandates coupled with the need for ongoing tech investments imply tighter margins unless offset by scale or efficiency gains. Community Bank’s capacity constraints inherent in community-focused institutions limit rapid growth but promote steadier returns.

Growth Catalysts: Dividend Focus and Regional Banking Trends

Dividend payments stand out as a pivotal growth enabler for CB Financial Services by reinforcing investor confidence and attracting income-focused shareholders [N3][N4]. The Board declared a $0.28 per share quarterly cash dividend payable on May 29, 2026 [S6], sustaining a multi-year payout trend that aligns with steady net income generation.

Regional economic expansion underpins credit demand within Community Bank’s local markets. Incremental loan book growth supported by favorable demographic drivers can propel revenue increase without heavy risk.[S1] Adoption of digital banking technologies enhances customer engagement efficiency enabling scalable service improvements despite limited branch network expansion.

Market share gains may accrue as smaller competitors struggle with technology complexity or regulatory costs. CB Financial’s prudent balance sheet positions it to seize such opportunities conservatively with risk controls intact.

Risks and Watchpoints: Cybersecurity Incident and Regulatory Impact

The May 2026 material cybersecurity event represents the most significant contemporary risk for CB Financial Services [S3]. Exposure of sensitive personal information via an unauthorized AI tool presents potential regulatory sanctions risk alongside reputational damage that could affect future customer trust.

While prompt containment measures are reassuring, unknown remediation costs or extended investigations could strain resources or distract management focus. Cybersecurity threat vectors continue evolving rapidly necessitating substantial investment in defense mechanisms beyond legacy systems.

Moreover, regulatory agencies overseeing banking institutions have intensified scrutiny in this area post-incident scenarios nationally—a development increasing compliance burdens for Community Bank [S3]. Vigilance over privacy laws such as GLBA (Gramm-Leach-Bliley Act) notification requirements remains critical to avoid punitive fines.

Other structural risks include regional economic downturns affecting loan performance or competitive pressures compressing interest margins despite asset quality maintenance.

What Investors Should Monitor Next

Key near-term catalysts include:

- Detailed outcomes from the ongoing cybersecurity investigation: scope definition, root cause identification, remediation milestones.

- Any formal regulatory feedback or enforcement actions related to the data exposure.

- Updates on any changes in loan portfolio credit metrics signaling economic shifts locally.

- Confirmation of continued dividend payments reflecting underlying earnings sustainability [S2][S3].

- Management commentary during upcoming earning calls or investor presentations clarifying strategic responses to operational risks.

- Effectiveness of newly implemented controls and enhanced monitoring tools intended to prevent similar breaches.

- Progress reports on technology adoption plans balancing cost efficiency with security enhancements given sector trends.

Additionally, attention should focus on how newly appointed CFO Amanda L. Engles leads financial discipline efforts amidst these evolving challenges [S5].

Latest Financial Snapshot: Liquidity and Capital Structure

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $56mm | |

| 2026-03-31 | ||

| Total debt | 0 USD | |

| 2025-12-31 | ||

| Net debt | $-56mm | |

| 2025-12-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value | Period End |

|---|---|---|

| Cash & Equivalents | $55,549,000 USD | |

| 2026-03-31 | ||

| Total Debt | $0 USD | |

| 2025-12-31 | ||

| Net Income | $4,903,000 USD | |

| 2025-12-31 |

CB Financial Services’ strong liquidity position—with cash holdings surpassing total debt levels—provides a sound foundation for weathering near-term uncertainties [F1]. Zero reported total debt negates refinancing risks commonly faced by peer regional banks which often carry moderate leverage ratios.

This conservative capital structure supports stable dividend distributions evidenced in Q1 results reflecting modest but consistent net income generation [F1]. Cash conversion appears efficient facilitating ongoing operational funding without reliance on external borrowing facilities disclosed thus far in filings.

This analysis is based solely on information publicly available from SEC filings dated up to May 12, 2026, supplemented by credible news sources referenced herein. It does not constitute investment advice or recommendations regarding securities transactions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments