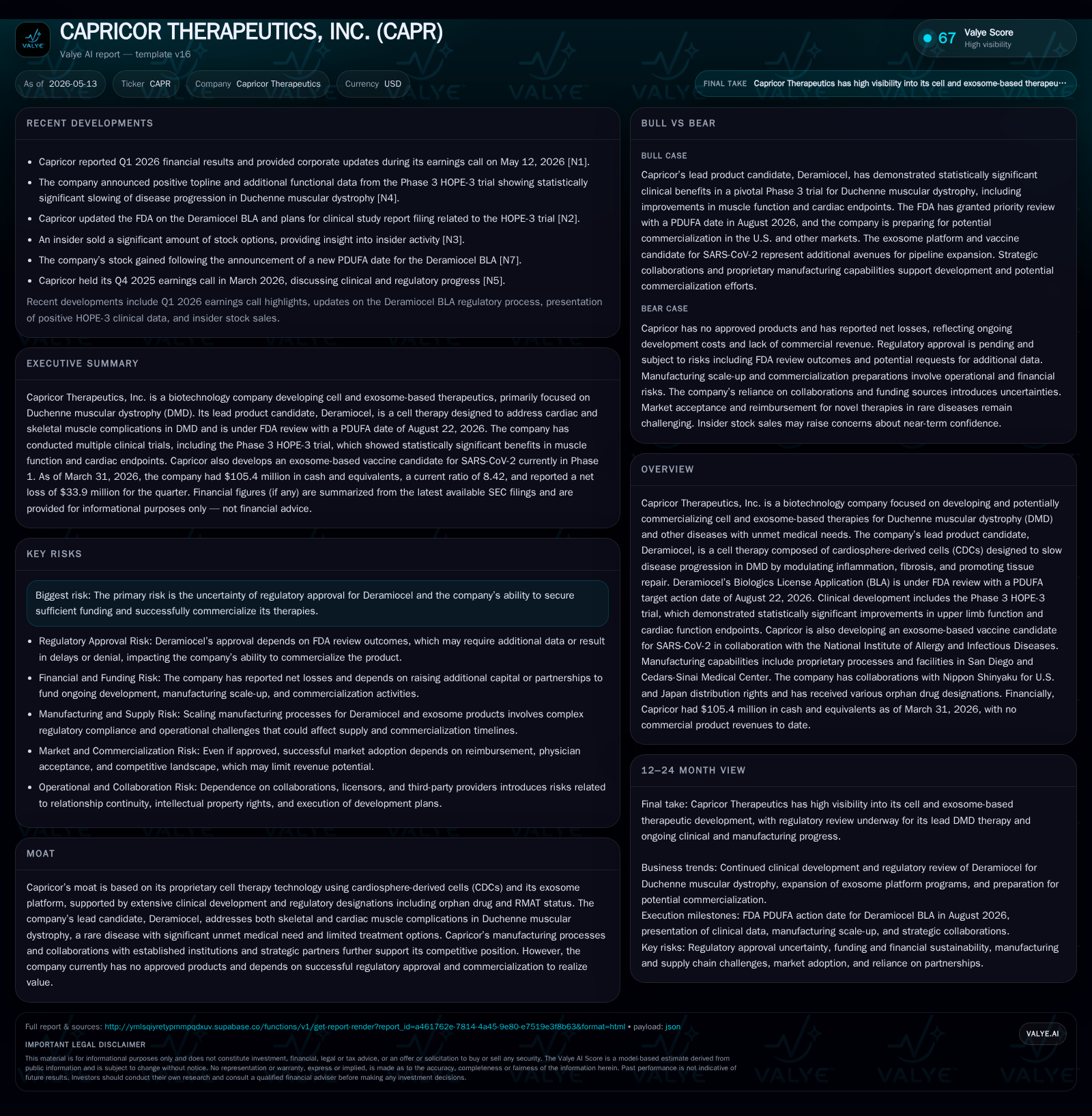

Capricor’s Cell Therapy Platform Poised for Breakthrough in Muscular Dystrophy

Capricor Therapeutics advances with FDA review of Deramiocel, leveraging proprietary cell and exosome technologies to address Duchenne muscular dystrophy.

Capricor’s latest quarterly filing details continued progress toward a pivotal FDA decision on Deramiocel, supported by strong Phase 3 clinical results demonstrating efficacy in Duchenne muscular dystrophy (DMD). The company’s business model hinges on an innovative cell therapy platform targeting muscle inflammation and fibrosis, differentiating it from gene-centric competitors. While facing regulatory and manufacturing scaling risks, Capricor’s orphan drug designations and unique product profile position it defensibly within a niche rare disease market. Upcoming catalysts include the August 2026 PDUFA date and manufacturing scale milestones.

Latest Quarterly Operating Update and Regulatory Milestones

The May 13, 2026 quarterly report [S2] marks a critical juncture for Capricor Therapeutics as the company's lead cell therapy candidate Deramiocel remains under active review by the U.S. FDA. The Biologics License Application (BLA) is on track for a Prescription Drug User Fee Act (PDUFA) target decision date set for August 22, 2026 [S2]. This positions Capricor at a near-term inflection point where regulatory consent could unlock commercial pathways and transform the operational narrative.

Recent disclosures highlight that the Phase 3 HOPE-3 trial delivered statistically significant functional improvements in DMD patients’ upper limb strength and cardiac endpoints [S2][N1]. These efficacy signals are vital in confirming the mechanistic rationale underpinning Deramiocel's immunomodulatory and anti-fibrotic activity mediated by its proprietary cardiosphere-derived cells (CDCs).

Manufacturing updates indicate ongoing process optimization to ensure scalable commercial supply that meets cGMP standards—a recognized challenge given the complexity of cell-based therapies [S3]. Concurrently, Capricor maintains an active collaborative research agenda exemplified by its exosome-based vaccine platform developed in partnership with the National Institute of Allergy and Infectious Diseases (NIAID), reflecting diversification albeit at an early stage.

This quarter's operating update distinctly improves visibility on the company’s imminent catalyst schedule while contextualizing risk exposures around regulatory verdicts and scalability hurdles.

Capricor’s Business Model and Product Differentiation

Capricor Therapeutics functions as a clinical-stage biotech innovator specializing in cell- and exosome-based therapeutics targeted primarily at Duchenne muscular dystrophy, a debilitating rare genetic disorder characterized by progressive muscle wasting including compromised cardiac function [S1].

Deramiocel represents the flagship from a mode-of-action perspective: an allogeneic cell therapy comprising CDCs isolated from donated human hearts that exert multi-layered biological effects via secretion of bioactive exosomes. These influence inflammation modulation, fibrosis reduction, angiogenesis promotion, and tissue repair facilitation—addressing both skeletal and cardiac manifestations atypical of many purely gene-targeted strategies such as exon-skipping or CRISPR gene editing aimed narrowly at dystrophin expression restoration [S1].

Revenue potential is inherently binary at this juncture; contingent unequivocally on successful regulatory greenlighting followed by effective commercial execution. Absence of any current marketable products means operational financial commitment is focused on clinical development expenditures plus investment in advanced manufacturing capability required to meet anticipated demand upon approval [S1][F1].

Notably, proprietary manufacturing expertise in handling delicate CDC cultures constitutes both a strategic moat and a bottleneck risk factor. The handling of donor tissue supply chains aligns deeply with bioprocess sophistication unique to this modality. In parallel, Capricor's exosome platform introduces an exciting adjunct pipeline avenue offering potentially more scalable products possessing favorable stability profiles analogous to established biologics yet capable of complex biological pathway modulation [S1].

Competitive Positioning and Industry Structure in Rare Disease Therapies

The therapeutic landscape for DMD is multifaceted with competitors advancing gene therapies using viral vector delivery systems to reinstate dystrophin expression or employing exon-skipping oligonucleotides that partially restore functional protein. Steroid regimens remain standard-of-care but have limited impact on disease progression particularly regarding cardiomyopathy [S1].

Capricor's dual-action approach addressing both muscle types via cellular immunomodulation situates it uniquely within this ecosystem. This differentiation is compounded by orphan drug designations that confer market exclusivity advantages alongside tax incentives [S18].

Complexities emerge in navigating payer acceptance due to high-cost biologic nature juxtaposed against limited patient populations inherent in rare diseases. Pricing power depends heavily on demonstrated clinical benefit robustness in meaningful functional endpoints coupled with health-economic justifications anchored in delaying costly disease complications such as heart failure.

Manufacturing barriers for advanced cell therapeutics create high entry costs preserving incumbent advantages yet simultaneously represent scale-up risks impacting supply continuity. Strategic collaborations—with entities like NIAID—highlight integrated external expertise infusion but partnerships will need leveraging further to support global commercialization ambitions [S1][N4].

Regulatory frameworks continue evolving especially around orphan product approvals ensuring expedited pathways albeit increased post-market scrutiny remains probable.

Growth Drivers: Regulatory, Clinical Expansion, and Commercial Readiness

Foremost growth propulsion centers on clearing the FDA hurdle at the August 22 PDUFA date where anticipated approval of Deramiocel would transition Capricor from developmental stage into revenue generation phase [S2][N1]. Positive Phase 3 trial data bolster confidence yet actual regulatory interpretation may impose label restrictions or require post-marketing commitments adding near-term compliance obligations [S21].

Pipeline expansion through additional indications or geographies represents secondary growth vectors. Further clinical trials or bridging studies might allow label broadening beyond initial skeletal/cardiac indications or international submissions leveraging established dossier components.

Scale-up of manufacturing capacity constitutes another critical driver enabling adequate commercial supply and underpinning market penetration rates. Successful navigation here can enhance margins through cost control while safeguarding product quality consistency essential for payer trust.

Parallel advancement of the exosome vaccine candidate enhances pipeline optionality although current status remains exploratory requiring time horizons beyond immediate fiscal frames to materially contribute.

Strategic partnerships to augment sales infrastructure domestically while negotiating licensing deals internationally can accelerate rollout speed reducing Capricor’s direct commercialization burden.

Risks and Growth Constraints: Regulatory Uncertainty and Commercial Execution

Primary business risk lies in FDA's final assessment outcome—an unfavorable decision would stall revenue onset indefinitely given absence of approved products currently [S2][S1]. Regulatory setbacks elsewhere globally may compound delays adding uncertainty around international deployments.

Manufacturing challenges loom large given dependency on donor heart tissue availability combined with technical complexities inherent to CDC culturing processes [S15]. Failure to successfully scale or replicate pilot runs at commercial volumes could impair launch timelines or inflate costs harming gross margin structures.

Commercial reimbursement environment presents ambiguity especially amid shifting U.S. healthcare policy landscapes emphasizing pricing reforms potentially involving most-favored-nation pricing frameworks which could introduce downward price pressures even post-approval [S19][S24].

Substantial capital will be imperative beyond this quarter for launch readiness encompassing marketing investments plus expanded R&D activities; inability to secure favorable financing terms may impair execution capability [S1]. Legal/regulatory compliance burdens also persist given extensive requirements surrounding healthcare fraud/abuse laws impacting promotional activities post-commercialization [S6][S7].

Finally, modest operating scale exposes the company to volatility related to personnel retention risks as well as cybersecurity vulnerabilities owing to sensitive health information management environments [S1].

Key Upcoming Catalysts and What Investors Should Monitor

Investors should closely track the August 22, 2026 PDUFA decision milestone which will significantly alter enterprise value dynamics either positively following approval or negatively if delayed or denied [S2][N1]. Pre-decision events such as potential FDA Advisory Committee meetings or guidance clarifications could foreshadow regulator sentiment.

Post-approval progress indicators include validation of manufacturing scale-up achievements demonstrated through lot release data or facility certifications ensuring uninterrupted supply chain continuity.

Clinical trial enrollment updates for any ongoing label expansion studies combined with pipeline advancement announcements surrounding exosome technology programs can provide insight into long-term growth sustainability.

Partnership developments or licensing contracts suggest increased external validation and resource leverage enhancing commercial footprint prospects.

Finally, monitoring changes in reimbursement discussions particularly Medicare coding assignments or payer coverage decisions will be fundamental to projecting realistic revenue ramp scenarios following market entry.

Current Financial Health and Capital Position

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $105.4 million | |

| 2026-03-31 | ||

| Current assets | $283.1 million | |

| 2026-03-31 | ||

| Current liabilities | $33.6 million | |

| 2026-03-31 | ||

| Current ratio | 8.42x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

As per the latest balance sheet dated March 31, 2026 [F1], Capricor maintains approximately $105.4 million in cash and equivalents accompanied by current assets totaling $283.1 million against comparatively modest current liabilities near $33.6 million yielding a robust current ratio of about 8.42—indicative of strong short-term liquidity positioning supporting operational liquidity through critical near-term milestones.

The absence of reported debt underscores a capital structure free from leverage constraints providing flexibility but also emphasizing reliance on equity or alternative financing sources ahead as cash burn continues driven largely by clinical development spend reflected in recent operating losses exceeding $108 million annually per last available periods [F1].

| Metric | Value |

|---|---|

| Cash & Equivalents | $105.4 million |

| Current Assets | $283.1 million |

| Current Liabilities | $33.6 million |

| Current Ratio | 8.42 |

Disclaimer: This analysis is based solely on publicly available SEC filings dated through May 13, 2026, associated news reports, company disclosures, and structured data from companyfacts. It does not constitute investment advice nor does it incorporate any non-public information.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments