Q32 Bio Advances Autoimmune Therapy Pipeline with Strong Q1 Cash Position

Q32 Bio Inc. reported continued clinical progress alongside robust liquidity amid sustained operating losses in Q1 2026.

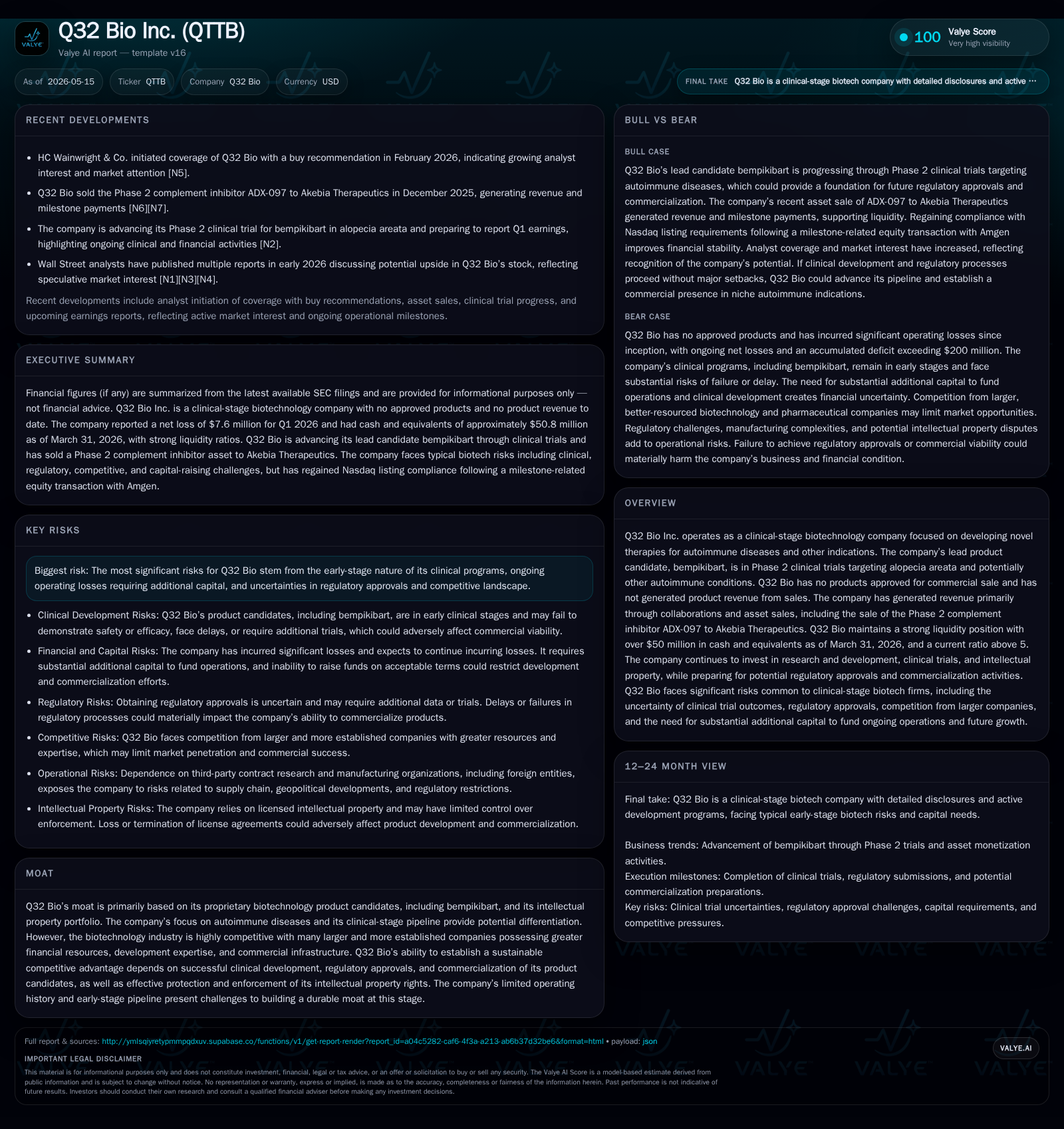

In its latest quarterly filing, Q32 Bio emphasized ongoing Phase 2 clinical trials for its lead autoimmune therapy, bempikibart, while maintaining a strong balance sheet with over $50 million in cash and equivalents. Despite no approved products or sales revenue yet, the company’s strategic focus remains on advancing its pipeline and protecting intellectual property to secure long-term differentiation. Industry risks include regulatory uncertainties and intense competition, underscoring the need for successful trial outcomes and capital management.

Recent Operating Update

Q32 Bio Inc.'s latest quarterly filing dated May 5, 2026 ([S2]) confirms continuation of its clinical-stage biotech trajectory focused primarily on autoimmune diseases. The company reported net losses of $7.6 million for Q1 2026 compared with $11.0 million in the prior year quarter ([S2]), showing a reduction in operating losses though still reflecting the heavy investment phase typical of this industry segment.

Critically, Q32 Bio has yet to generate product sales revenue as it remains in developmental stages; revenues stem from prior collaboration agreements and asset transactions such as the sale of its complement inhibitor candidate ADX-097 to Akebia Therapeutics ([S1],[S3]). Significant operating expenditures target research and development activities to advance its lead candidate, bempikibart, currently undergoing Phase 2 trials aimed at alopecia areata treatment with intended expansion into related autoimmune conditions ([S1]).

The company maintains a strong liquidity position with cash and equivalents totaling approximately $50.75 million as of March 31, 2026 ([F1]), complemented by current assets of $57.2 million against current liabilities of $10.7 million, resulting in a robust current ratio of 5.36 ([F1]). This financial cushioning underpins Q32 Bio’s capacity to sustain its pipeline investments through near-term clinical milestones without immediate financing pressures.

Business Model

Q32 Bio operates as a pure-play clinical-stage biotechnology firm focused on discovering and developing novel therapies for autoimmune diseases. Revenue to date has come mainly from milestone payments tied to licensing deals and asset sales rather than product commercialization ([S1],[S3]). The core value driver is their proprietary immunology-based platform underpinning product candidates like bempikibart.

Bempikibart exemplifies this model: it is an investigational biologic designed to interrupt immune system malfunction responsible for hair loss in alopecia areata patients—a market niche currently underserved by effective therapies. The company’s business model involves successfully navigating costly and complex clinical development phases—primarily Phase 2 at this stage—before achieving regulatory approval, which then sets the foundation for commercialization or further partnership opportunities.

Intellectual property protection plays a crucial role in securing competitive exclusivity amid numerous biotech incumbents.

Industry Structure and Competitive Position

The autoimmune therapeutic space is characterized by high scientific complexity, extended development timelines, stringent regulation, and intense competition involving several large pharmaceutical companies backed by substantial cash resources ([S1],[S15]). As a relatively small entity without approved products or commercial infrastructure, Q32 Bio faces structural challenges including:

- Dependence on successful trial outcomes for pipeline candidates like bempikibart.

- Need to maintain adequate funding given persistent operating losses.

- Navigating regulatory requirements across different jurisdictions for approval.

- Protection against patent infringement litigation common in biotech sectors ([S26],[S28]).

Despite these challenges, Q32 Bio’s focus on unmet needs within immune-mediated diseases provides strategic differentiation if late-stage efficacy data prove favorable. Its ability to enforce intellectual property rights is vital to defending market share alongside other emerging therapies.

Growth Drivers

The primary growth catalysts center on advancement of Q32 Bio’s clinical programs:

- Clinical Data Milestones: Readouts from bempikibart’s Phase 2 trials targeting alopecia areata are crucial inflection points that could validate the therapeutic hypothesis and unlock further indications.

- Regulatory Progress: Successful filings with agencies like the FDA would enable access to broader patient populations.

- Business Development: Partnerships or licensing collaborations could provide capital influxes while leveraging external commercialization expertise.

- Pipeline Expansion: Identifying additional autoimmune targets broadens future revenue potential beyond single-asset dependency.

Fundamental demand drivers in autoimmune diseases include an increasing prevalence rate globally and growing acceptance of biologic treatments as standard care for various immune dysfunctions—trends that support structural long-term growth outside cyclical healthcare spending patterns.

Risks / Watchpoints / Growth Constraints

Key risks inherent within Q32 Bio’s operating model include:

- Clinical Trial Uncertainty: Failure to demonstrate efficacy or safety can terminate programs early with material financial losses ([S2],[S26]).

- Capital Requirements: Ongoing losses necessitate external funding; disruption in capital markets or dilutive financing could impair shareholder value ([S12],[S28]).

- Regulatory Hurdles: Approval delays or restrictive indications narrow commercial opportunity. Pricing pressures exist internationally due to governmental controls affecting revenues even when approved ([S15],[S16]).

- Intellectual Property Challenges: Litigation risks both from third parties claiming infringement and potential internal disputes may consume management attention and resources ([S26],[S28]).

- Competitive Intensity: Larger competitors with established networks may dominate market adoption post-launch.

- Operational Risks: Reliance on third-party contract manufacturing organizations (CDMOs) introduces supply chain vulnerabilities ([S29]).

- Compliance Exposure: Enforcement risks around healthcare regulations including anti-bribery laws bear reputational penalties ([S19]).

Monitoring these factors remains essential as they materially influence operational execution and strategic viability.

What to Watch Next

Investors and stakeholders should observe key upcoming company milestones:

- Announcements regarding Phase 2 bempikibart data readouts expected later this year will be critical indicators of therapeutic promise ([N1]).

- Any initial regulatory submissions following positive trial results signal transition toward commercialization potential.

- Updates on collaboration deals expanding financial runway or bolstering marketing capabilities would validate strategic progress.

- Intellectual property portfolio developments including new patents granted or disputes resolved could affect competitive positioning.

Careful tracking of these KPIs offers insight into whether Q32 Bio is effectively managing developmental risks toward value creation.

Financial Profile Summary

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $51mm | |

| 2026-03-31 | ||

| Current assets | $57mm | |

| 2026-03-31 | ||

| Current liabilities | $11mm | |

| 2026-03-31 | ||

| Current ratio | 5.36x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

As supported by latest companyfacts data at quarter-end March 31, 2026 ([F1]):

- Cash & Equivalents: $50.75 million providing sufficient near-term funding cushion.

- Current Assets: $57.20 million versus Current Liabilities: $10.67 million yielding a Current Ratio of ~5.36 indicating strong short-term liquidity.

- Revenue: Historically derived from collaborations/asset sales; no product sales yet measured as it remains pre-commercial (˜$53.7 million recorded as last annual figure year-ended Dec 31, 2025).

- Net Losses: Continuing trend with $7.6 million loss for Q1 2026 reflecting heavy R&D investment phase.

Overall balance sheet strength supports operational continuity through foreseeable clinical development milestones absent unforeseen expenses or capital access issues.

Disclaimer: This analysis is based solely on publicly available information from Q32 Bio Inc.’s filings up to May 2026. It does not constitute investment advice or a recommendation regarding securities purchase or sale.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments