EHang Expands eVTOL Reach Despite Profitability and Supply Chain Challenges

EHang's latest quarterly results highlight continued international deliveries alongside ongoing operational and financial headwinds in the nascent autonomous aerial mobility market.

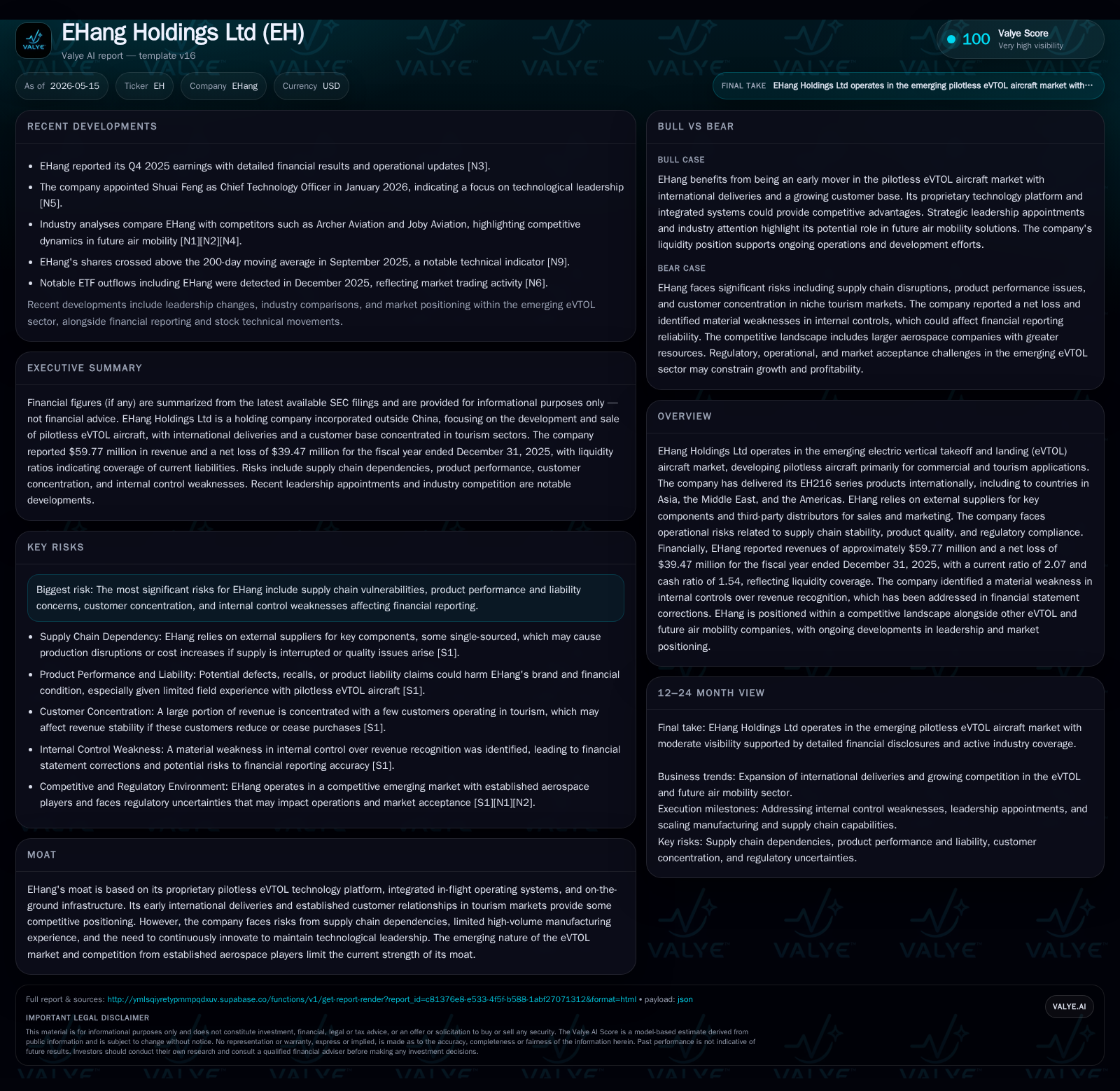

EHang Holdings Ltd reported fourth quarter and full-year 2025 results showing persistent losses amid cautious revenue growth driven by international expansion of its EH216 eVTOL aircraft. The company’s business model centers on pilotless electric vertical takeoff and landing vehicles primarily serving tourism and commercial applications, relying on third-party suppliers and distributors across multiple countries. Competitive pressures intensify as legacy aerospace players enter the emerging urban air mobility space, while EHang navigates supply chain dependencies, regulatory complexities, and evolving customer expectations. Continued R&D investment and scale-up in manufacturing capacity are vital to unlocking growth, but risks related to product liability, operational disruptions, and internal control weaknesses remain critical watchpoints.

Recent Operating Update

In its most recent quarterly filing dated March 12, 2026 ([S2]), EHang Holdings Ltd announced its unaudited financial results for the fourth quarter and full fiscal year ended December 31, 2025. During this period, the company sustained net losses amid modest revenue gains primarily fueled by increased deliveries of its EH216 pilotless eVTOL aircraft internationally. This release confirms ongoing challenges inherent in commercializing autonomous urban air mobility (AAM) products while scaling operations globally.

Specifically, revenue totaled approximately $59.77 million for full-year 2025 compared to prior years’ numbers reported previously ([F1]). The net loss stood at $39.47 million despite continued R&D investment into next-generation models and enhancing operational infrastructure such as integrated command-and-control platforms ([S1]). Although not profitable yet, management projects sufficient liquidity to fund near-term operations with a current ratio of about 2.07 supported by $36.7 million in cash relative to $13.2 million in total debt ([F1]).

Deliveries of the EH216 series increased outside China during the period — including customers in Malaysia, Thailand, South Korea, and Japan — following earlier shipments to markets such as Brazil, Colombia, Saudi Arabia, Qatar, UAE, and Dominican Republic ([S7]). However, scaling internationally introduces complexities around distribution networks relying heavily on third-party partners whose operational effectiveness can materially affect sales outcomes ([S16]).

Business Model

EHang’s core value proposition is a proprietary electric vertical takeoff and landing aircraft platform designed for autonomous operation without a human pilot onboard. The company primarily targets commercial applications like sightseeing tours in tourism hubs where corridor air traffic is less congested relative to urban commuter use cases. Revenue derives from selling these pilotless eVTOL vehicles alongside providing associated commercial solutions involving software command-and-control systems tied to cloud infrastructure.

Strategically, EHang leverages external suppliers for components (including batteries) rather than vertically integrating manufacturing. This approach reduces upfront capital intensity but exposes the company to supply chain reliability risks as well as quality control complexities ([S5],[S14]). Revenue recognition occurs largely upon transfer of physical possession to third-party distributors or end customers once delivery conditions under ASC 606 are met ([S16]). Pricing power currently appears constrained by the nascent market status where unit demand is small relative to established aviation sectors.

The company's operating ecosystem extends beyond hardware sales into post-sale services integrating fleet management through its telecommunication-enabled operating system that demands robust cybersecurity measures due to potential threats from hacking or system outages impacting safety-critical functionalities ([S1],[S18]).

Industry Structure and Competitive Position

Operating in the broader Advanced Air Mobility (AAM) industry segment characterized by emerging eVTOL innovators alongside traditional aerospace incumbents entering urban air taxi markets ([N1],[N2]), EHang faces multifaceted industry competitiveness:

- Many rivals possess materially greater financial resources facilitating advanced R&D pipelines or manufacturing scale advantages.

- Regulating authorities globally are still refining standards governing certification of autonomous flight operations posing entry barriers.

- Product reliability benchmarks including battery endurance limit technological viability for widespread adoption today.

EHang's moat centers on early proprietary software integration enabling pilotless autonomy combined with partial go-to-market first-mover advantages particularly in specialized tourism sectors across China and select international territories ([S1],[S7]). However, limited brand recognition outside core markets necessitates building distribution channels often through non-exclusive third-party partners which dilutes direct customer engagement control ([S16]). Furthermore, concentrated customer exposure heightens earnings volatility since losing a major tourism operator client could materially impair sales metrics ([S5]).

Growth Drivers

Several structural avenues underpin EHang's growth aspirations:

- International Market Expansion: Continued penetration into Asia-Pacific countries along with selective Middle Eastern and Latin American markets diversifies demand profiles beyond China’s regulatory environment ([S7]).

- Technology Development: Incremental R&D targeting extended flight range, payload capacity improvements leveraging advances in battery tech could unlock broader commercial applicability beyond tourism leisure flights ([S14],[S19]).

- Manufacturing Scale-Up: Augmenting production capability will be essential for economy-of-scale cost reductions that can support competitive pricing without eroding margins substantially ([S1],[S7]).

- Service Ecosystem Expansion: Leveraging its integrated cloud-based operating system for additional revenue streams such as fleet analytics or maintenance contracts presents monetization opportunities complementary to hardware sales ([S1]).

These growth drivers remain contingent on securing regulatory approvals across jurisdictions—some requiring lengthy validations—and managing risks inherent in new technology adoption cycles within safety-conscious markets.

Risks / Watchpoints / Growth Constraints

EHang's pathway entails attendant execution risks:

- Supply Chain Vulnerabilities: Dependence on external suppliers for key components exposes the company to delays or cost inflation especially given global semiconductor/battery shortages remain prevalent across industries ([S5],[S14]).

- Product Liability Exposure: Limited operational history elevates risks that product defects or accidents could disrupt commercialization efforts or trigger costly litigation beyond insurance coverage limits ([S14],[S19]).

- Internal Control Weaknesses: Identified material weaknesses over revenue recognition require remediation efforts that consume management bandwidth while potentially eroding investor confidence until resolved ([S18]).

- Customer Concentration: Heavy reliance on a small group of tourism-centric customers introduces demand variability tied closely to travel trends or discretionary spending patterns vulnerable to macroeconomic or geopolitical shocks ([S5]).

- Regulatory Complexity: Navigating disparate aviation authorities’ certifications adds uncertainty around timing of expansions or product launches limiting near-term order visibility ([S1],[S14]).

- Competitive Intensity: Increased activity by aerospace giants and other AAM startups elevates innovation pace thresholds needed to maintain differentiation reducing pricing flexibility over time ([N1],[N2]).

What to Watch Next

Key upcoming milestones will indicate whether EHang can convert its technological promise into sustainable growth:

- Quarterly delivery volumes especially international shipments reveal traction outside flagship Chinese markets.

- Advancement or delays in obtaining regulatory certifications pertinent to expanded operational domains.

- Progress reports on internal controls remediation provide clues on improving governance practices impacting investor risk perception.

- New commercial partnerships or expansions into adjacent sectors beyond tourism signal diversification success.

- R&D outcomes targeting product upgrades affecting performance specifications like range or payload capacity inform competitive positioning enhancements.

Management commentary during earnings releases highlighting supply chain status or capital raising strategies will also be crucial given ongoing liquidity needs articulated historically ([S8], [F1]).

Financial Profile (Brief Context)

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $37mm | |

| 2025-12-31 | ||

| Total debt | $13mm | |

| 2025-12-31 | ||

| Net debt | $-23mm | |

| 2025-12-31 | ||

| Current assets | $212mm | |

| 2025-12-31 | ||

| Current liabilities | $102mm | |

| 2025-12-31 | ||

| Current ratio | 2.07x | |

| 2025-12-31 |

Source: SEC companyfacts cache [F1].

While EHang continues investing heavily toward its strategic objectives amid steep competition and execution complexity, its capital position provides some runway though access to additional financing remains an acknowledged need subject to market conditions ([S8],[F1]).

| Metric | Value | Period End |

|---|---|---|

| Revenue | $59.77M | |

| 2025-12-31 | ||

| Operating Income | -$45.29M | |

| 2025-12-31 | ||

| Net Income | -$39.47M | |

| 2025-12-31 | ||

| Cash & Equivalents | $36.67M | |

| 2025-12-31 | ||

| Total Debt | $13.23M | |

| 2025-12-31 | ||

| Current Ratio | 2.07 | |

| 2025-12-31 |

This analysis is based solely on publicly available information from SEC filings dated through May 15, 2026 and associated news sources without any forward-looking investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments