TOFUTTI Brands Confronts Supply Challenges While Defending Its Plant-Based Niche

The impending closure of TOFUTTI’s primary co-packer threatens supply continuity amid ongoing competitive and margin pressures in the plant-based dairy alternatives market.

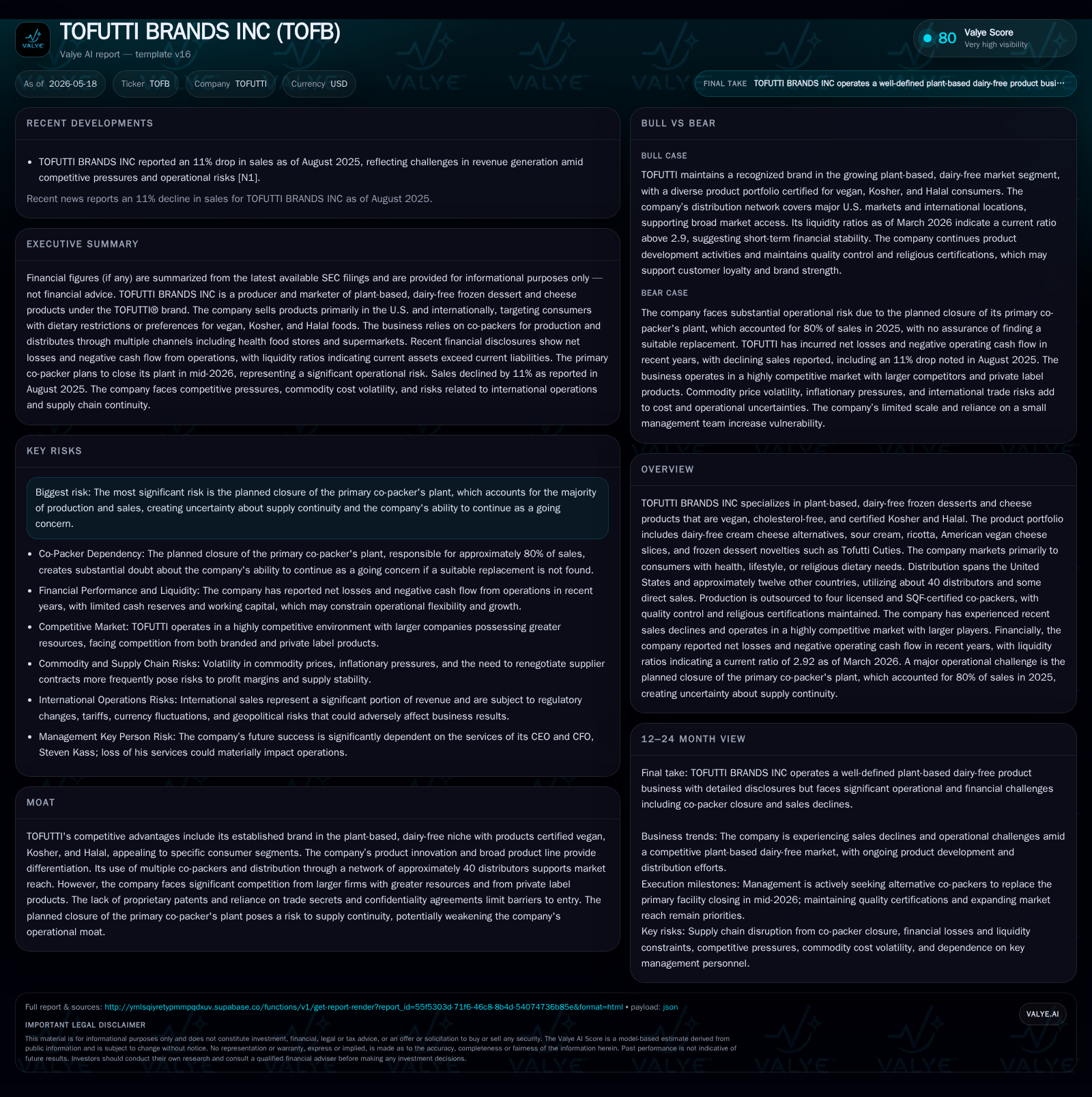

In its latest 10-Q filing, TOFUTTI Brands disclosed that its primary co-packer, responsible for approximately 80% of its sales, will close by July 31, 2026. This situation introduces significant operational risk concerning manufacturing continuity and casts doubt on the company's going concern status. TOFUTTI’s business model centers on producing certified vegan, Kosher, and Halal plant-based dairy alternatives through outsourcing to multiple SQF-certified co-packers. The firm operates in a highly competitive arena with larger players and private label pressures. Growth depends on niche product innovation, market segmentation, and broad distributor coverage, but is constrained by supply vulnerabilities and inflationary cost pressures.

Latest Quarterly Operating Update: Impacts of Primary Co-Packer Closure

TOFUTTI Brands’ May 18, 2026 10-Q filing reveals a critical near-term operational challenge: the planned closure of its primary co-packer facility effective July 31, 2026 [S2][S1]. This plant is responsible for producing approximately 80% of TOFUTTI’s sales volume, including core products like BETTER THAN CREAM CHEESE and other key vegan cheese offerings [S1]. The impending shutdown raises substantial doubt about the company’s ability to maintain supply continuity, creating acute pressure on revenue stability and casting uncertainty on its capacity to continue as a going concern.

Management is actively seeking alternative manufacturing partners but acknowledges that no assurance exists regarding finding a suitable replacement swiftly enough to avoid disruption [S1]. Given TOFUTTI’s outsourced production model relying heavily on this single vendor, substituting production poses logistical complexity. This carries potential risks of lost volume or higher costs during a transitional phase. Moreover, recurring operating losses and negative cash flow compound these risks by limiting financial flexibility to absorb short-term shocks [S1].

TOFUTTI’s Business Model and Product Differentiation

TOFUTTI’s business revolves around the development, marketing, and distribution of plant-based dairy alternatives encompassing frozen desserts accoutered under the Tofutti ® brand alongside a suite of vegan cheese products such as cream cheese analogues, sour cream alternatives, ricotta substitutes, and American vegan cheese slices – all explicitly cholesterol-free, butterfat-free, gluten-free (for cheeses), and aligned with stringent dietary certifications including Kosher-parve and Halal compliance [S1]. This positioning targets consumers whose purchase decisions are significantly influenced by health concerns, lifestyle choices (veganism), or religious dietary restrictions.

The company does not manufacture internally; instead it outsources all production to four licensed co-packers who hold Safe Quality Food (SQF) certifications—a rigorous food safety benchmark recognized industry-wide—ensuring quality control compliance requisite for acceptance by major natural and gourmet specialty distributors as well as secular supermarkets serving health-conscious consumers nationwide [S1][S4]. This strategy enables flexible capacity management but deepens dependency risk given the concentration around the primary facility

Product breadth provides some differentiation within the crowded plant-based sector: five flavors of BETTER THAN CREAM CHEESE in multiple packaging sizes serve both retail health food stores and food service customers. The frozen dessert line includes Tofutti Cuties novelties distributed domestically and internationally across approximately twelve countries via roughly forty distributors plus direct sales channels [S1][S25]

Industry Structure and Competitive Positioning within Plant-Based Dairy Alternatives

Operating within the plant-based dairy alternatives industry means TOFUTTI competes against significantly larger branded firms with access to greater capital resources for product innovation, marketing scale, and distribution penetration. Moreover, private label products from national supermarket chains represent a persistent pricing threat that compresses margins for smaller players like TOFUTTI [S1][S28]

While TOFUTTI has carved out a niche centered on specialized certification-driven consumer subsets (vegan/Kosher/Halal), barriers to entry across this category remain limited due to an absence of patent protections; the company relies on trade secrets and confidentiality agreements for intellectual property protection but cannot erect durable technological moats absent registered patents [S10][S26].

The heavy reliance on a primary co-packer contrasts with common industry practice where multi-sourcing tends to mitigate supplier risk; here it amplifies vulnerability leading into the upcoming plant closure event. Distribution infrastructure involving around forty distributors nationwide spanning natural foods chains underscores broad market access though potentially fragmented customer relationships limit pricing leverage relative to dominant brands [S25][S28]

Growth Drivers: Product Innovation, Market Segmentation, and Distribution Reach

TOFUTTI’s growth efforts hinge fundamentally on sustained innovation targeted at expanding their product lineup within defined consumer niches characterized by health needs or religious mandates. Although product development expenses remain modest ($156k in fiscal 2025), ongoing investments support packaging refreshes compliant with FDA labeling mandates like the Food Safety Modernization Act while maintaining product relevance [S4]

Geographically, while primarily U.S.-centric with penetration into about a dozen foreign markets including Canada, Australia, Israel, Egypt, France, Mexico, Panama, and the UK—the latter representing roughly 15% of revenues—international expansion presents additional complexity given tariff considerations, currency exchange risks due to transactions conducted exclusively in USD, and variable regulatory environments affecting imports/exports [S5][S6][S28].

TOFUTTI leverages its broad distributor footprint (~40 distributors) for market coverage spanning natural grocery chains, food service companies, kosher markets (which accounted for about 10% of sales in fiscal 2025), and mainstream health food retailers across diverse U.S. regions including New York metropolitan area (27% of sales), California (11%), Midwest (10%), Mid-Atlantic (10%) among others—a geographically diversified but moderate scale presence supporting stable if modest demand volumes [S19][S25]

Risks and Watchpoints: Supply Chain Vulnerabilities and Margin Pressures

The preeminent risk factor confronting TOFUTTI involves the imminent shutdown of Franklin Foods’ facility producing circa 80% of sales volume scheduled for July-end cessation with no assured immediate successor contracted yet [S1][S2]. This portends potential interruptions ranging from order delays to lost shelf space or forced price concessions if alternate suppliers command higher fees or require requalification timelines creating inventory gaps—a fragile scenario amplified by operational cash constraints attributable to recurring losses noted over recent fiscal years ($778k net loss FY2025)

Additionally problematic are rising raw material costs amid sustained inflationary trends influencing commodity pricing including corn oil, palm oil inputs underpinning fat content used across products [S2][S23]. The company acknowledges increased frequency required in renegotiating supplier contracts due to volatility thereby escalating margin unpredictability which may compress profitability further unless offset by successful price increases—though consumer resistance caps pricing power especially given competitive pressures from private label alternatives priced lower

International operations face typical cross-border risks such as tariffs or import restrictions while fluctuating currency exchange rates impose an additional layer of volatility since all export business is invoiced in USD potentially depressing foreign demand if local currencies weaken versus USD [S6][S28]. Food safety breaches or regulatory enforcement actions remain latent hazards given stringent FDA oversight over labeling claims (nutrition panels per Food Safety Modernization Act) plus certification maintenance; failures might provoke costly recalls or reputational damage jeopardizing buyer confidence crucial for repeat orders in specialty niche retail channels [S3][S6][S8].

What to Watch Next: Contract Negotiations and New Manufacturing Partnerships

Stakeholders should monitor developments tied directly to securing new or supplementary manufacturing partners capable of assuming production volumes before July 31 deadline without material interruption. Successfully concluding these negotiations will be pivotal in preserving supply chain integrity. Furthermore tracking inventory levels at distributors can signal potential tightening preceding any transition-related shortages.

Also critical will be management commentary regarding pricing strategies aimed at counterbalancing inflationary input cost hikes without eroding customer loyalty—a balance integral to sustaining margins under intensifying competition.

Operationally relevant will be announcements regarding multi-sourcing plans which could diminish previous concentration risk at Franklin Foods’ site—potentially repositioning TOFUTTI’s manufacturing footprint toward greater resilience.

Customer retention metrics encompassing key accounts servicing kosher markets or health-focused retailers will also serve as bellwethers for demand sustainability amidst uncertainty.

Financial Snapshot: Liquidity, Losses, and Working Capital Status

As of March 28, 2026 quarter-end per latest data from SEC filings complemented by Companyfacts insight: TOFUTTI held approximately $2.85 million in current assets against $978 thousand in current liabilities yielding a healthy current ratio near 2.92 indicating adequate short-term liquidity buffers despite operational stress factors [F1]. Total outstanding debt stands minimal at $165 thousand underpinning limited leverage exposure allowing some financial maneuverability [F1]. Nonetheless recurring net losses totaling $778 thousand reported for fiscal year ended December 2025 coupled with negative operating cash flows reflect ongoing profitability challenges restricting capacity for investment or cushioning shocks arising from supply disruptions or cost inflation pressures [F1][S1].

Maintaining sufficient working capital will remain essential as the company navigates contractual transitions among co-packers while attempting to preserve brand equity through innovation budgeting amidst tight resources.

Financial position in context

Current assets of $3mm and current liabilities of $978000 imply a current ratio near 2.92x for 2026-03-28 [F1]

Disclaimer: This analysis is based solely on information contained in publicly available SEC filings as of May 18, 2026 and company data snapshots dated up to March 28, 2026. It is intended for informational purposes only without any investment research view.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments