Smith-Midland Strengthens Project Pipeline with Strategic Leadership and Product Innovation

Q1 2026 results highlight revenue growth momentum and enhanced margin performance amid management changes.

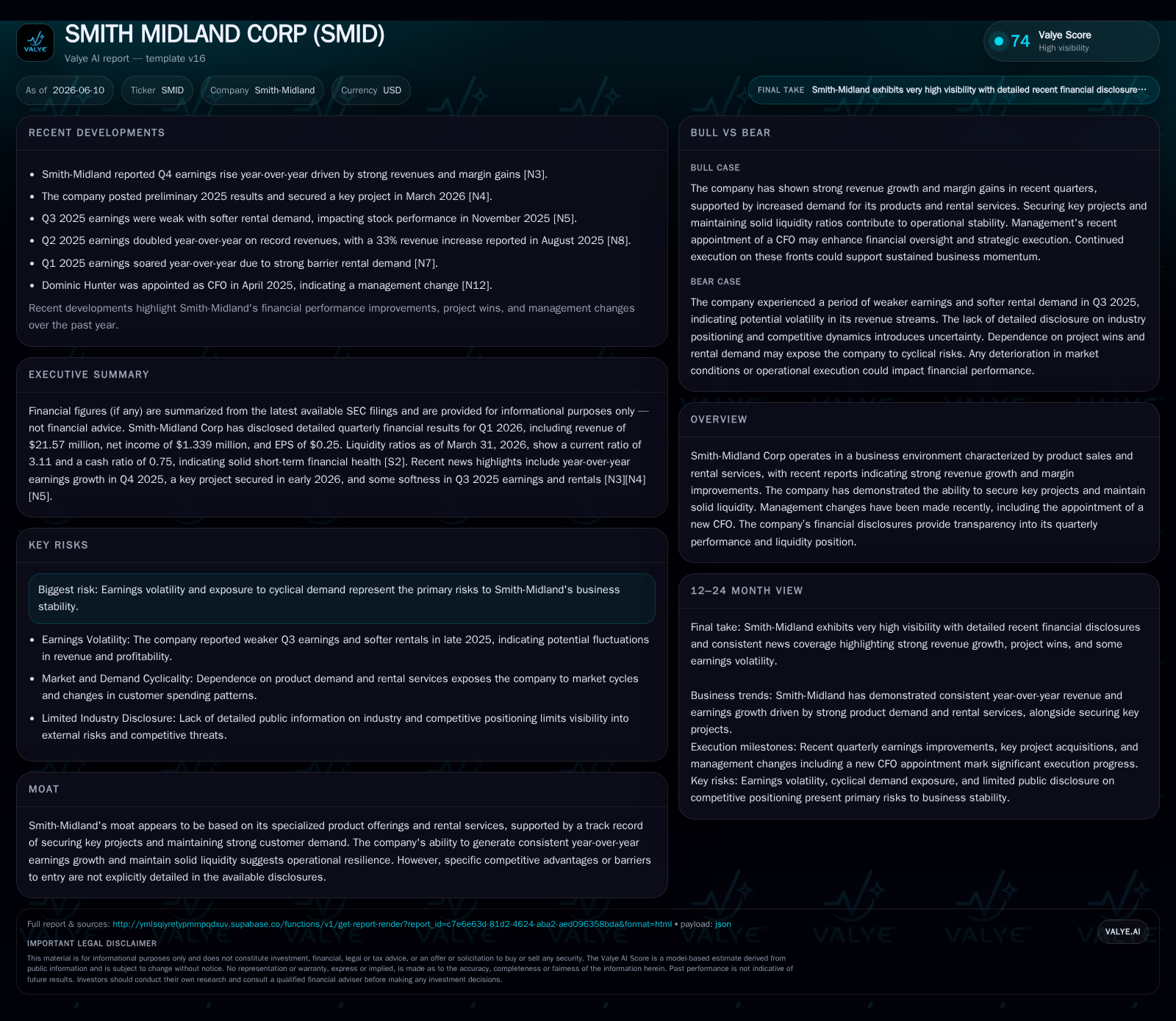

Smith-Midland Corporation's Q1 2026 filing reveals continuing strength in its precast concrete product sales and rental services, with improvements in operating margins supported by a robust project pipeline. The company has strategically appointed a new CFO to bolster financial oversight as it pursues growth through proprietary product innovation and targeted regional expansion. Exposure to cyclical infrastructure spending remains a key risk factor, counterbalanced by recurring demand from highway safety barrier rentals and patented product lines. The company maintains solid liquidity with a strong current ratio, positioning it well for near-term operational needs.

Recent Operating Update: Q1 2026 Progress

Smith-Midland Corporation’s Q1 2026 10-Q filing dated June 10, 2026, along with the June 9 event filing, highlights sustained operational momentum in its precast concrete business ([S2][S3]). The company reported revenue growth driven by both sales of proprietary precast products and recurring rental income from highway safety barriers. Gross margin improvement was noted, reflecting a favorable product mix shift toward higher-margin proprietary lines such as SlenderWall® exterior wall panels and J-J Hooks® highway safety barriers. The appointment of Dominic L. Hunter as Chief Financial Officer during this period underscores a strategic emphasis on financial discipline to support growth initiatives and capital allocation ([S3]).

The company’s project pipeline expanded, supported by a growing backlog of orders across its core Mid-Atlantic and Southeastern U.S. markets. This geographic focus aligns with Smith-Midland’s strategy to leverage patented precast systems and installation services, enhancing competitive differentiation within the regional precast concrete sector.

Business Model: Revenue Mechanics and Strategic Position

Smith-Midland operates a vertically integrated model encompassing the invention, manufacturing, marketing, leasing, licensing, sale, and installation of precast concrete products primarily serving construction contractors and transportation authorities ([S1]). The company’s revenue streams include:

- Product Sales: Specialized precast concrete products such as SlenderWall® lightweight, energy-efficient exterior wall panels; J-J Hooks® positive-connected highway safety barriers; SoftSound™ sound absorptive finishes; transportable concrete buildings under the Easi-Set® and Easi-Span® brands; as well as utility vaults, retaining walls, and farm-specific products like cattleguards ([S1]).

- Barrier Rental Services: Recurring rental income from highway safety barriers provides a stable cash flow base, mitigating earnings volatility associated with the cyclical nature of construction contracting.

- Licensing of Proprietary Technologies: Patented designs and regulatory approvals underpin unique product offerings, generating licensing fees and reinforcing pricing power.

- Installation Services: Onsite product installation complements sales and rental activities, adding value and supporting customer retention.

This diversified revenue mix balances volume-driven sales with recurring rental and licensing income, reducing exposure to construction cycle fluctuations. Pricing power is reinforced by patents, crash safety certifications, and state and federal approvals, creating high switching costs for customers such as federal, state, and local transportation agencies and major contractors.

Industry Structure & Competitive Landscape

Smith-Midland operates within the precast concrete construction materials sector, which is characterized by regional competition due to logistics and transportation cost sensitivities. The company’s competitive set includes larger peers such as Oldcastle Infrastructure and Forterra, which offer similar product portfolios but operate at greater scale.

Smith-Midland’s competitive moat derives from its portfolio of patented and proprietary products, including positive-connected highway safety barriers that have undergone rigorous crash testing and regulatory approval ([S1]). Its barrier rental business further differentiates the company by addressing ongoing maintenance and replacement needs in highway infrastructure projects.

The customer base primarily comprises government transportation authorities and general contractors engaged in public and private infrastructure projects, which typically involve multi-year contracts but are subject to funding cycles and budgetary constraints. The company’s geographic footprint across the Mid-Atlantic, Northeastern, Midwestern, and Southeastern U.S. provides some regional diversification but also exposes it to localized infrastructure spending fluctuations.

Growth Drivers

Federal and state infrastructure investment increases remain a key growth driver, supporting demand for precast concrete products used in roadways, utilities modernization, and commercial construction. Smith-Midland’s focus on innovative, energy-efficient products such as SlenderWall®, which combines lightweight concrete with steel framing for enhanced thermal performance and structural integrity, positions it well to capitalize on green building trends and evolving regulatory standards ([S1]).

The highway safety barrier rental segment generates stable, annuity-like revenue streams that help smooth cash flow during downturns in construction activity. Additionally, rising adoption of modular and prefabricated construction methods expands opportunities for transportable concrete buildings (Easi-Set®), broadening end-market applications beyond traditional site-built structures.

Further growth potential exists through geographic expansion into adjacent regions and enhanced licensing arrangements for proprietary products. Continued research and development investments in sound absorptive finishes (SoftSound™) address regulatory requirements related to noise pollution mitigation, representing another structural growth avenue.

Risks & Constraints

Smith-Midland faces typical industry risks including demand cyclicality tied to government infrastructure budgets and project timing uncertainties ([S17]). Earnings volatility can arise from delays or cancellations of contract awards and fluctuations in raw material costs, particularly cement and steel, which impact production expenses and margins.

Supply chain disruptions pose operational risks given the capital-intensive nature of precast manufacturing. Competitive pressures from other precast concrete manufacturers and alternative materials suppliers remain moderate but require ongoing innovation and regulatory compliance to maintain differentiation.

Installation services introduce execution complexity, necessitating skilled project management to avoid reputational and financial impacts. Liquidity management remains critical; however, the company’s strong current ratio of 3.11 and net cash position provide a solid buffer against cyclical headwinds ([F1]).

What To Watch Next

Upcoming quarterly disclosures will be important to assess whether Smith-Midland can sustain margin improvements alongside order backlog growth, which serves as a key indicator of demand health. Market reception to new proprietary systems, particularly in energy-efficient panels and barrier technologies, will provide insight into potential pricing leverage.

Announcements regarding contract awards or geographic market expansion could offer further visibility into pipeline strength. Monitoring raw material cost trends and government infrastructure spending signals will be essential to gauge volume and margin outlooks.

Management commentary following the new CFO appointment will be closely watched for strategic priorities, including capital expenditure plans and innovation focus areas that may influence medium-term growth trajectories.

Financial Profile Highlights

Smith-Midland maintains a strong liquidity position, with a current ratio of approximately 3.11 as of March 31, 2026, reflecting current assets of $51.6 million against current liabilities of $16.6 million ([F1]). Total debt remains minimal at $648,000, resulting in a net cash position that supports operational flexibility ([F1]).

Based on the latest full-year data ending December 31, 2025, the company reported net income of $12.5 million and operating income of $17.0 million on revenues near $93.4 million, demonstrating solid profitability margins ([F1]). The steady rental revenue stream contributes to cash flow stability, balancing the variability inherent in project-based product sales.

These financial metrics underscore Smith-Midland’s operational resilience and capacity to manage working capital effectively amid the cyclical precast concrete industry dynamics.

This analysis integrates the latest SEC filings with sector-specific context to provide a comprehensive view of Smith-Midland Corporation’s operational and financial position as of mid-2026, without projecting future financial outcomes or offering investment research views.

Disclaimer: This is research-only, informational analysis and not investment advice. It includes AI-generated interpretation and general industry context. Verify important details using primary sources.

Comments