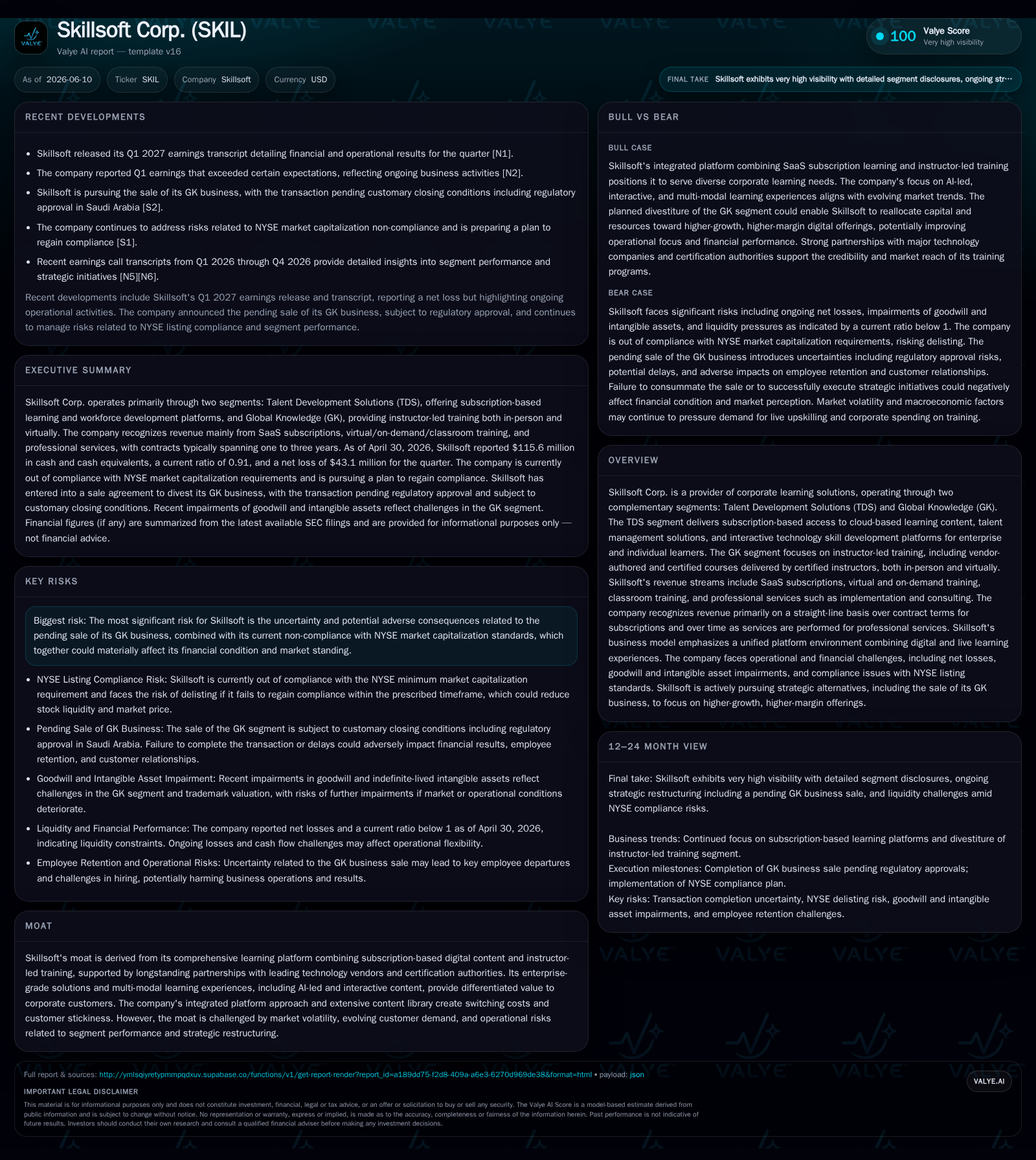

Skillsoft’s Strategic Shift and Hybrid Learning Model Under Pressure from Segment Sale and Listing Risks

Skillsoft is restructuring amid the pending sale of its Global Knowledge business, navigating NYSE compliance challenges while focusing on subscription-led talent development.

Skillsoft Corp.’s latest quarterly filing reveals a critical juncture marked by the anticipated sale of its instructor-led Global Knowledge (GK) segment and ongoing non-compliance with NYSE market capitalization requirements. These developments underscore near-term operational uncertainties and potential financial implications. Skillsoft’s core business model centers on a hybrid learning platform combining cloud-based Talent Development Solutions (TDS) subscription services with instructor-led training under GK. The planned divestiture of GK refocuses the company toward SaaS-driven growth, yet exposes risks tied to transaction execution, revenue mix shifts, and market perception. Structural growth drivers include rising corporate demand for digital upskilling and compliance training, but Skillsoft faces constraints from macroeconomic sensitivity, evolving customer preferences, and a heavily leveraged balance sheet.

Operating Update Highlights: Pending Divestiture Adds Uncertainty

Skillsoft’s Q1 Fiscal Year 2027 10-Q filing dated June 9, 2026 [S2], supplemented by a contemporaneous 8-K [S3], anchors this analysis. The company disclosed entering into an agreement on May 20, 2026, to sell its Global Knowledge (GK) business unit to EHJob GP LLC. The transaction faces customary closing conditions including an antitrust review in Saudi Arabia with expected completion in FY27 Q2 (ending July 31, 2026), but material execution risk remains.

Proceeds are estimated modestly at $5–8 million net of cash divested over approximately two years. This signals that strategic rationale is more about operational focus—shifting away from legacy instructor-led training—rather than directly improving liquidity. Skillsoft is exposed during the interim period to contractual constraints and market perception risks that could disrupt business momentum or investor confidence if the deal stalls or terms materially differ from expectations.

Concurrently, Skillsoft remains out of compliance with NYSE’s minimum market capitalization standards [S1], due largely to recent macroeconomic volatility dampening investor appetite for live upskilling offerings, which weigh on GK revenues. The company has filed a remedial Plan proposing cost reduction and capital reallocation toward higher-margin digital offerings but faces uncertainty on plan approval or implementation success.

Business Model: Hybrid Corporate Learning Focused on SaaS Subscriptions

Skillsoft operates through two core segments: Talent Development Solutions (TDS) and Global Knowledge (GK) [S22]. TDS delivers cloud-based digital learning platforms offering scalable SaaS subscriptions for enterprise customers and individuals alike—combining large content libraries with interactive learning modules suitable for workforce reskilling amidst fast-moving technical landscapes. The offering includes an enterprise-grade Skills Management Platform and a Learner Platform targeting technology skills enhancement.

The GK segment utilizes a more traditional model centered around instructor-led training—both classroom and virtual delivery—with vendor-authored certification courses backed by longstanding alliances with major tech vendors. While GK complements TDS by covering accredited professional training needs, it exhibits lower margins and has faced demand softness recently.

Revenue streams include subscription fees recognized evenly over contract terms for TDS products; for GK professional services like instructor-led sessions or consulting services, revenue is recognized as services are delivered over time [S1]. This revenue recognition aligns with SaaS industry practices but leaves exposure to churn risk as customers evaluate subscription renewals against shifting corporate budgets.

Industry Structure and Competitive Position

The corporate learning industry comprises solution providers ranging from pure SaaS platforms (e.g., Cornerstone OnDemand) to instructor-led trainers (similar to portions of Skillsoft's former GK model), certification authorities, and integrators offering holistic talent management ecosystems.

Skillsoft’s hybrid approach—integrating both subscription-based cloud services with traditional instructor-led offerings—is somewhat unique among peers focused singly on SaaS or face-to-face models. This creates competitive advantages through multi-modal learning pathways favored by large enterprises seeking comprehensive upskilling programs alongside compliance-certified education.

The company’s extensive content library paired with vendor certifications establishes switching costs by embedding users within their system ecosystems. However, evolving customer preferences towards fully digital or AI-enhanced platforms pressure traditional models like GK’s face-to-face training variants.

Growth Drivers: Digital Upskilling Demand Amid Workforce Transformation

Structural tailwinds underpinning Skillsoft’s TDS SaaS platform include accelerating requirements across industries for upskilling/reskilling driven by technological disruption (cloud migration, AI adoption), regulatory compliance expansion, and globalization concerns mandating scalable remote training solutions.

Corporate clients increasingly favor subscription models granting continuous access versus episodic instructor bookings—a shift favoring TDS growth potential post-GK divestiture. Additionally, integration of AI-driven interactive content enhances relevance amid competitive content overload in the marketplace.

However, growth levers depend critically on sustaining high renewal rates among existing customers and expanding active user bases without substantial customer acquisition cost inflation—a balance demanding persistent investment in platform innovation while managing churn risks.

Risks & Constraints: Transaction Execution & Market Compliance Pressures

Foremost among risks is the conditional nature of the GK sale closing; failure would leave Skillsoft burdened with a margin-dragging segment amid macro uncertainties. Transaction timing delays or regulatory hurdles could severely impact near-term operating clarity.

Financially, as of April 30, 2026, Skillsoft held approximately $115.6 million in cash and equivalents against $580.2 million in total debt, resulting in a net debt position near $465 million [F1]. Current assets of $287.0 million and current liabilities of $313.9 million imply a current ratio of approximately 0.91 [F1]. This balance sheet context highlights leverage and liquidity considerations amid ongoing operating challenges.

NYSE listing non-compliance adds external pressure—delisting would reduce stock liquidity impairing capital raising capacity—putting emphasis on management's ability to execute remedial measures successfully.

Further industry-wide threats include accelerating obsolescence risk for learning content if R&D fails to keep pace with technology shifts; competition from open-access educational resources driving pricing pressures; integration complexities when embedding learning platforms into enterprise HR systems; plus evolving data privacy regulations impacting cloud service deployment.

What to Watch Next

- GK Business Sale Progress: Regulatory approvals timeline particularly Saudi antitrust clearance ahead of July FY27 Q2 close target; any deviation would signal strategic continuity risk [S2].

- NYSE Compliance Plan Updates: Timing for Plan submission acceptance by NYSE along with quarterly milestones enforcement.

- Subscription Metrics: Tracking ARR evolution within TDS post-GK spiraling off signals core growth health; renewal rates highlight customer retention efficacy.

- Margin Trends: Expansion of SaaS gross margins offsetting contraction from divested instructional services informs profitability trajectory.

- Debt Servicing Ability: Cash flow sufficiency under leverage profile amid restructuring costs reflects financial stability potential.

Brief Financial Profile Context

As of April 30, 2026, Skillsoft held $115.6 million cash against $580.2 million total debt yielding a net debt position near $465 million alongside a current ratio of approximately 0.91 [F1]. Operating losses have persisted recently driven by GK margin weakness despite steady contribution from TDS licenses [S10]. Ongoing restructuring aims at controlling expenses consistent with slower revenue growth environment outlined in recent filings [S1]. Capital structure refinement may be necessary dependent upon successful execution of strategic alternatives involving the GK divestiture and NYSE compliance progress.

This analysis incorporates the latest quarterly disclosures alongside annual filings to assess Skillsoft Corp.’s operational stance amid critical structural changes within the corporate learning sector. It leverages established industry KPIs such as ARR dynamics, renewal rates, segment contribution margins, alongside market compliance considerations impacting future strategic flexibility. No forward-looking investment research views are provided herein.

Financial position in context

As of 2026-04-30, companyfacts shows $116mm in cash and equivalents and $580mm of total debt [F1]. The same snapshot implies net debt of roughly $465mm, keeping balance-sheet context relevant but secondary to the operating story [F1]. Current assets of $287mm and current liabilities of $314mm imply a current ratio near 0.91x for 2026-04-30 [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments