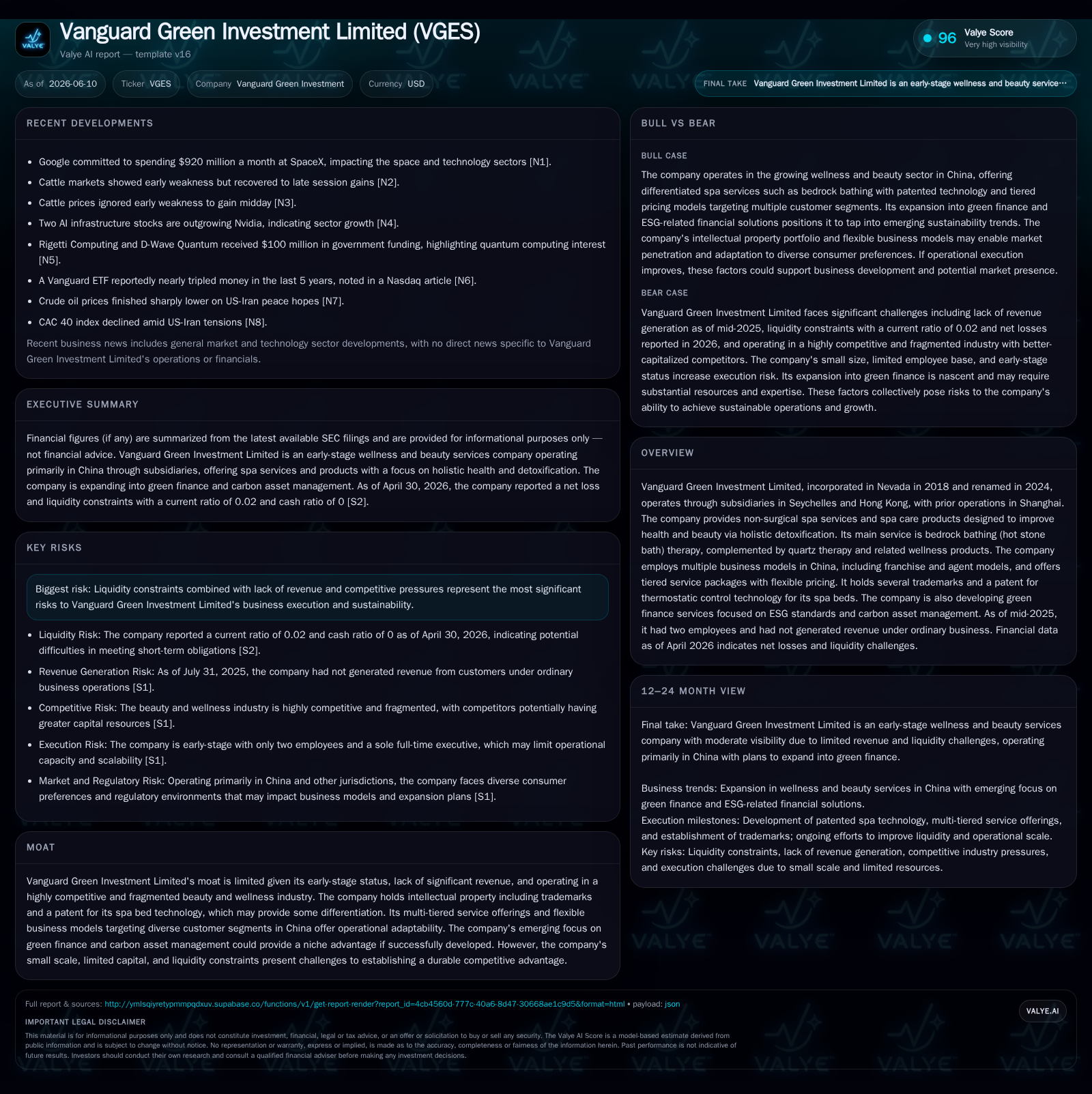

Vanguard Green Investment Advances Spa Services Amid Liquidity Challenges and Early-Stage Growth

Latest quarterly update highlights operational status of Vanguard Green Investment Ltd as it pursues scalable spa-based wellness and emerging green finance solutions.

Vanguard Green Investment Ltd remains an early-stage player within the fragmented beauty and wellness services sector, focusing on non-surgical spa treatments such as hot stone bedrock bathing complemented by quartz therapy products. The company’s flexible multi-tiered pricing and franchise-agent business models target diverse consumer segments, especially within China. Despite holding intellectual property including a thermostatic control patent and several trademarks, Vanguard faces significant liquidity constraints and has yet to generate substantial revenue under ordinary operations. Its strategic pivot into green finance and ESG-related carbon asset management represents a potential niche expansion but remains nascent. Competitive pressures, limited scale, and cash flow challenges are critical headwinds in the near term.

Latest Operating Update and Its Significance

Vanguard Green Investment Limited's most recent quarterly filing on June 10, 2026 ([S2]) largely reaffirms its continued status as an early-stage operator in the beauty and wellness space without significant new revenue or operational milestones reported. This latest 10-Q does not disclose material changes in business activity or financial improvement relative to prior periods. Instead, the company's operational narrative remains anchored around its foundational non-surgical spa services delivered primarily through franchises and agent-operated locations across China via subsidiaries based in Seychelles and Hong Kong ([S1],[S6]).

Liquidity pressures emerge as the most immediate concern: Vanguard reported only $55 in cash equivalents at quarter-end April 2026 against current liabilities exceeding $800,000 ([F1]). The lack of new revenue generation since fiscal year 2025 further constrains cash flow prospects ([F1],[S1]). Consequently, funding runway is critically tight for scaling investments or marketing initiatives.

Business Model Analysis

Vanguard’s core offering centers on holistic health improvement via spa services and wellness products designed to detoxify and enhance bodily functions ([S1],[S7]). The flagship service is "bedrock bathing" or hot stone bath therapy—a centuries-old Japanese-inspired modality involving lying on heated stone slabs embedded with specialized rocks such as Black Silica, Radium Stone, Far Infrared Stone, Negative Ion Stone, and Beitou Stone ([S7],[S17]). This non-invasive treatment is intended to promote blood circulation, immune system strengthening, metabolic enhancement, weight management, skin improvement, and anti-aging effects.

Complementing this are quartz therapies aimed at restoring chakra balance—an alternative wellness philosophy emphasizing physical-spiritual harmony—and proprietary care products like essential oil diffusers with antibacterial features and mini water purifiers utilizing advanced filtration technology ([S16],[S18]).

The company employs a three-pronged business model tailored to the complex Chinese consumer market:

- Franchise & Tripartite Cooperation Model: Collaborates with local partners who deploy spa beds and operate branded locations under shared profit arrangements.

- Large-scale Chain Agent Model: Deploys equipment across networks operated by third-party agents leveraging local market insight.

- Direct Service Store Model: Company-run outlets providing end-consumer access to bedrock bathing and ancillary wellness services ([S7]).

Pricing aligns with a three-tier tiered packaging:

- Flagship: High-end premium experience targeting affluent consumers.

- Luxury: Mid-market segment aiming at middle-class buyers.

- Refined: Entry-level pricing for budget-conscious customers seeking quality treatments ([S7],[S16]).

This flexible tiered pricing strategy incorporates subscription packages (10-, 20-, or 30-visit bundles), pay-per-service options, membership programs facilitated via online platforms including WeChat channels—embracing omni-channel marketing critical for rapid penetration in disparate regional markets ([S7],[S16]).

A proprietary patented thermostatic control setting for their stone spa beds (patent granted Singapore 2021) enables user-customized heating profiles that can reduce electricity consumption while maintaining treatment efficacy ([S5]). This technology potentially lowers operating costs for providers and offers differentiation amid commoditized equipment competition.

Adding complexity is Vanguard’s nascent expansion into green finance targeting Environmental, Social, & Governance (ESG) investment frameworks alongside carbon asset management capabilities such as carbon pledge financing and custody services ([S4],[S5]). Although adjacent to the core wellness value chain, these services could open growth avenues if regulatory trends favor sustainability-oriented capital allocation. However, these remain early-stage initiatives without explicit scale or monetization clarity thus far.

Industry Structure and Competitive Positioning

The beauty and wellness industry is highly fragmented with many local operators competing on price, product range, brand recognition, and location convenience. Vanguard operates amid intensified rivalry accelerated by technological adoption of omni-channel sales strategies across social media and direct-to-consumer platforms. While companies like Massage Envy illustrate successful franchise-driven growth elsewhere in wellness services, Vanguard's relatively small footprint—indicated by only two employees reported mid-2025—and limited capitalization handicaps rapid scale-up ([S1],[F1]).

Trademarks spanning multiple jurisdictions including Hong Kong, UAE, Saudi Arabia bolster intellectual property protection mainly for branding nuances rather than broad industry exclusivity ([S18]). The patented thermostatic control device endows some product-level differentiation but faces potential challenges scaling widespread adoption due to incumbent competitors’ brand strength or broader equipment alternatives.

China’s vast geography coupled with heterogeneous urban-rural consumer behaviors demand agile localized market entry approaches—a factor Vanguard attempts to address through franchisee/agent partnerships imbued with local expertise ([S7]). Yet sustaining consistent quality control across these dispersed networks represents typical industry risk leading to variable customer experiences affecting retention rates.

Growth Drivers

Structural tailwinds underpinning long-term sector growth include rising disposable incomes among China’s expanding middle class elevating personal discretionary spending on health-enhancing treatments. Post-pandemic shifts exhibit heightened consumer prioritization of holistic well-being following extended lockdown isolation periods ([S8]). Wellness market estimates topping $1.5 trillion globally with projected annual growth of 5-10% underpin macro opportunity ([S8]).

Vanguard’s multi-tier pricing model potentially facilitates wider social penetration by accommodating diverse budgets while leveraging franchise/agent networks hastens geographic coverage extension ([S7]). Technology-enabled omni-channel distribution reduces customer acquisition costs compared to traditional brick-and-mortar channels alone.

Meanwhile, emergent interest in sustainable investing magnifies relevance of Vanguard’s ESG advisory ambitions aligning corporate responsibility with investor demands. If effectively integrated with core wellness brand propositions—perhaps facilitating carbon neutral facility certifications—this dual-focus could carve out unique competitive positioning over typical spas lacking sustainability credentials.

Risks and Constraints

Principal risks revolve around liquidity shortages evidenced by minimal cash reserves of only $55 against current liabilities exceeding $800,000 as of April 2026 ([F1],[S2]). Without substantive capital raises or meaningful operating cash flow generation from commercialized service locations or product sales still unrealized at scale ([F1],[S1]), ongoing business continuity poses material threat.

Intense fragmentation dilutes pricing power—with low market entry barriers inviting new competitors incentivized by growing wellness demand—undermining margin sustainability especially for smaller players needing elevated marketing spend to gain visibility.[S4][S7] Dependence on franchisee or agent performance supplements operational risk if inconsistent service delivery damages brand reputation or compromises customer loyalty.

Regulatory uncertainties around spa service licensing vary regionally; adherence costs might escalate compliance burdens while green finance initiatives contend with evolving standards complicating go-to-market timing.[S9] Intellectual property infringement risks exist but litigation absence currently limits disruption concerns.[S3] Supply chain disruptions could impair delivery of patented spa beds or related products delaying expansion plans.[S4]

What to Watch Next

Key indicators to monitor include:

- Evidence of initial revenue traction from franchise or direct-service outlets demonstrating accelerating utilization rates or average revenue per customer.

- Capital raises or debt restructuring events alleviating liquidity constraints vital for meeting growing working capital needs.

- Adoption milestones for patented thermostatic control-enabled spa beds signaling commercialization success.

- Launch progress or client wins within ESG green finance vertical validating strategic diversification effectiveness.

- Expansion of agent/franchise network count across mainland China indicating market penetration progress.

- Regulatory developments impacting licensing frameworks for spa health services or carbon asset management regulations affecting green finance activities.

Any quarterly filings offering updated operating cash flows or profitability metrics would significantly clarify whether Vanguard is transitioning beyond its pre-revenue development phase towards sustainable commercial scale.

Financial Profile Summary

As of April 30, 2026 financial data reveals minimal operational scale: cash & equivalents stood at a mere $55 while total current assets were just $16.6k against burdensome current liabilities north of $801k resulting in dangerously negative working capital conditions ([F1]). Total debt was approximately $135k dating back to April 2025 without reduction seen since then ([F1]).

No recent revenue specified beyond small historical figures suggests very limited service monetization ([F1]; last material revenue $19k recorded four years prior). Operating losses continue reflecting high fixed cost basis vis-à-vis negligible top-line inflows—the classic hallmarks of an early-stage enterprise struggling for commercial viability.[S1]

These financial constraints underscore urgent capital requirement imperatives if the company intends to fund planned multi-channel marketing execution supporting franchising models or roll out energy-efficient thermostatic technology broadly.[F1][S2]

This analysis synthesizes disclosures from Vanguard Green Investment Limited's latest SEC filings alongside pertinent industry knowledge relevant to beauty and wellness services markets. It does not constitute investment advice or valuations.

Financial position in context

As of 2026-04-30, companyfacts shows $55 in cash and equivalents [F1]. Current assets of $16,555 and current liabilities of $801,069 imply a current ratio near 0.02x for 2026-04-30 [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments