Dell Technologies Transforms AI Infrastructure with $51 Billion Backlog

Dell’s June 2026 quarter filing reveals a historic AI infrastructure backlog surge, reshaping revenue streams and signaling evolving enterprise hardware dynamics.

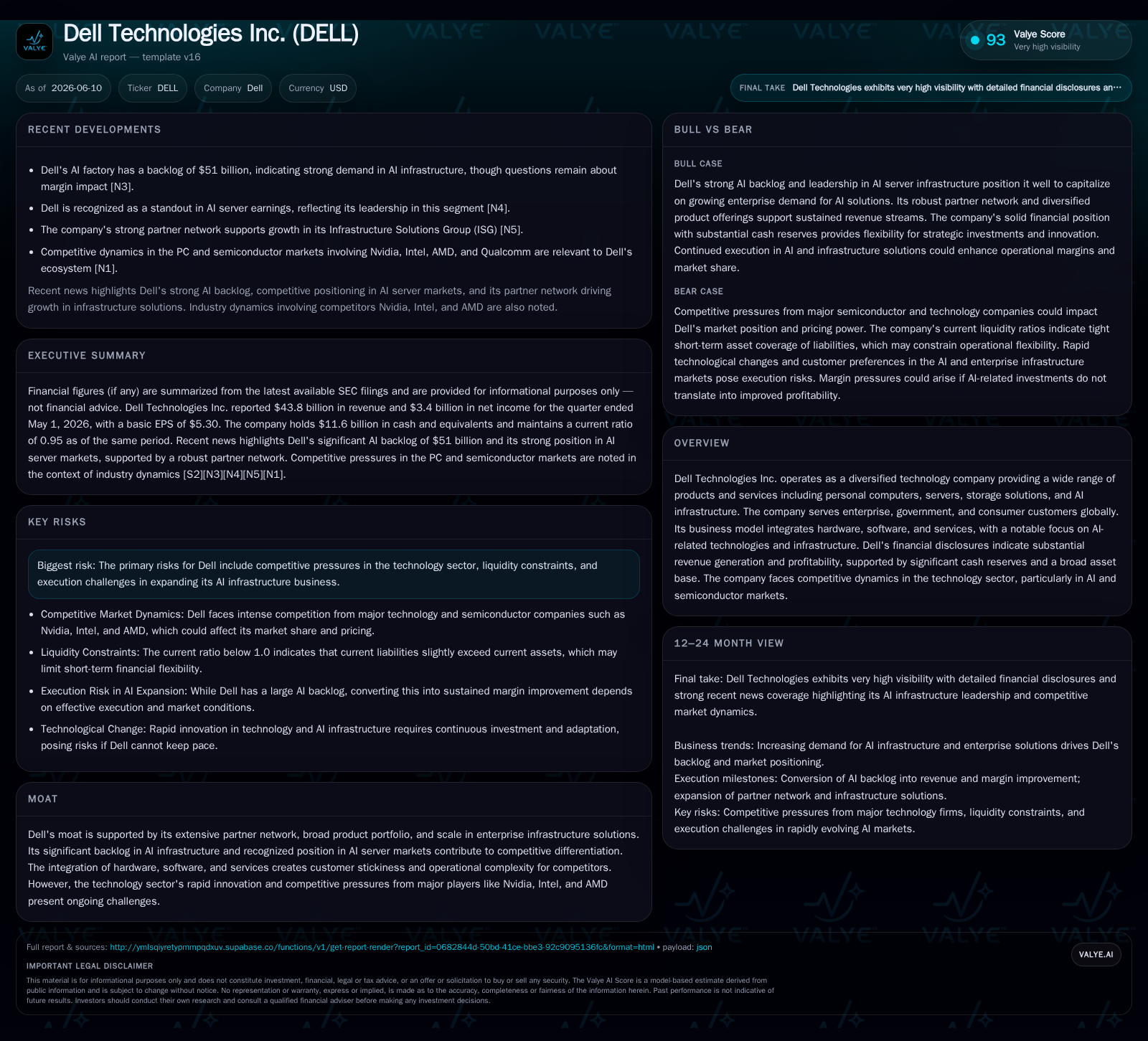

Dell Technologies’ latest quarterly 10-Q filing dated June 9, 2026, highlights a $51 billion backlog in its AI infrastructure segment, marking a pivotal inflection in demand visibility and business model evolution. This backlog expansion reflects strong enterprise and government customer adoption amid broader cloud and digital transformation trends. However, supply chain constraints, semiconductor dependencies, and margin compression present near-term operational challenges. Dell’s integrated hardware-software-services model, backed by an extensive partner network, positions it competitively against OEM peers while navigating capital intensity and execution risks. Monitoring backlog conversion rates, service contract renewals, and supply chain resiliency will be critical in assessing Dell’s trajectory through 2026.

Latest Quarterly Operating Highlights

Dell Technologies’ fiscal Q1 2027 filing for the period ended May 1, 2026, reveals a landmark $51 billion backlog in AI infrastructure orders, underscoring a significant surge in enterprise and government demand for advanced AI servers and systems optimized for machine learning workloads [S2][N3]. This backlog expansion not only enhances revenue visibility but also reflects a shift in Dell’s product mix toward higher-value, data center-centric hardware solutions. The backlog figure represents a substantial increase compared to prior quarters, signaling robust order intake and strong customer commitment in a market characterized by rapid AI adoption.

Revenue contributions are increasingly weighted toward servers and AI-optimized systems, while storage solutions maintain a steady and reliable base. The company’s partner network plays a critical role in scaling deployments, with partner channel sales materially contributing to growth by extending Dell’s reach into diverse enterprise accounts and government sectors worldwide [S2][N7]. Despite ongoing supply chain complexities, particularly related to semiconductor availability, Dell reports modest improvements in component sourcing, which is vital for timely backlog conversion.

Integrated Business Model: Hardware, Software & Services

Dell’s business model integrates hardware manufacturing with complementary software licensing and managed services contracts, creating a diversified revenue base that enhances customer retention and recurring revenue streams [S1]. The company designs and assembles servers and AI infrastructure tailored for high-performance computing, while software licenses enable advanced system functionalities such as virtualization, security, and AI workload management.

Managed services, including long-term support and consulting, contribute to recurring revenue and increase customer stickiness by embedding Dell deeper into clients’ IT operations. This integrated approach raises switching costs for large enterprise and government customers who depend on continuous system availability and vendor responsiveness. Dell’s ability to bundle hardware with software and services differentiates it from pure-play OEMs and supports a more resilient margin profile.

Competitive Positioning & Industry Dynamics

Within the enterprise IT hardware and infrastructure sector, Dell competes alongside peers such as Hewlett Packard Enterprise and Lenovo, each with broad product portfolios spanning servers, storage, and AI systems [S1]. While these competitors offer similar hardware solutions, Dell’s strength lies in its extensive partner network and vertically integrated business model that combines hardware, software, and managed services.

A critical factor influencing Dell’s operations is its reliance on semiconductor suppliers like Intel, AMD, and Nvidia, whose CPUs and GPUs power Dell’s AI infrastructure offerings. Recent market developments indicate intensifying competition among these chipmakers, affecting component pricing and availability, which in turn impacts Dell’s production schedules and operating margins [N2]. Additionally, the growth of cloud infrastructure providers such as Amazon AWS and Microsoft Azure influences enterprise purchasing patterns, driving demand for hybrid cloud solutions that Dell targets with its on-premises AI and data center hardware.

Operating margin pressures persist due to component cost inflation and competitive pricing strategies aimed at securing large AI infrastructure contracts. However, Dell leverages its scale and supplier relationships to negotiate favorable terms and mitigate some cost volatility.

Key Growth Drivers: AI Infrastructure & Partner Ecosystem

The primary growth driver is accelerating enterprise adoption of AI workloads requiring specialized compute environments with high-density GPU arrays and optimized tensor processing capabilities. Dell’s $51 billion AI infrastructure backlog reflects pre-booked deployments across multiple verticals, including financial services, healthcare, government intelligence, and telecommunications [S2][N3]

Dell’s partner ecosystem amplifies sales reach and enables value-added services such as system integration, managed hosting, and customized configurations, which increase average selling prices and foster customer loyalty [N7]. The expansion of hybrid cloud architectures further drives demand for Dell’s on-premises hardware, complementing public cloud resources and positioning Dell as a key enabler of flexible enterprise IT strategies.

Innovation in server energy efficiency aligns with growing corporate ESG priorities, influencing procurement decisions and providing Dell with a competitive edge in sustainability-conscious markets.

Risks and Execution Challenges Ahead

Execution risks include ongoing semiconductor supply chain constraints that could delay order fulfillment and increase component costs, thereby compressing gross margins [S2]. Intense competition for enterprise AI budgets exacerbates pricing pressure, challenging Dell’s margin sustainability.

Dell’s leverage profile, with net debt near $19.8 billion despite $11.6 billion in cash and equivalents, requires careful liquidity management, especially if capital expenditure needs accelerate due to rapid technology evolution [F1][S2]. Customer concentration in high-value government contracts introduces potential volatility from regulatory or budgetary shifts.

The complexity of integrating new AI infrastructure product lines demands disciplined execution across R&D, manufacturing, and channel enablement. Geopolitical risks affecting global supply chains and regulatory compliance add further uncertainty to Dell’s multinational operations.

Outlook: Milestones and Market Signals

Upcoming milestones include the next quarterly earnings release expected in September 2026, where backlog conversion rates into revenue will be a key metric to assess demand realization and growth momentum [S3]. New product launches featuring next-generation servers with improved performance-per-watt ratios are anticipated to address competitive pressures and customer requirements.

Service contract renewal rates will offer insights into the resilience of Dell’s recurring revenue streams amid evolving IT strategies. Broader macroeconomic indicators, such as corporate IT capital spending influenced by inflation and interest rates, will serve as important demand signals.

Monitoring partner network engagement and semiconductor supplier relationships will provide early warnings of potential supply chain or execution disruptions.

Concise Financial Commentary

As of May 1, 2026, Dell’s balance sheet shows $11.6 billion in cash and cash equivalents against $31.4 billion in total debt, resulting in net debt of approximately $19.8 billion and a current ratio of 0.95, reflecting a moderate liquidity cushion balanced against significant leverage typical of capital-intensive enterprise IT hardware operations [F1]

Operating income of about $8.15 billion demonstrates Dell’s capacity to internally fund growth initiatives, though free cash flow remains sensitive to capital expenditure pacing driven by rapid innovation demands [F1]. Maintaining disciplined cost control while investing strategically in new AI and data center architectures is critical to sustaining operating margins amid competitive and supply chain pressures.

In summary, Dell Technologies’ latest quarter highlights its emergence as a major AI infrastructure provider, supported by a record backlog that signals strong demand durability. Realizing this potential hinges on effective supply chain management, competitive execution, and navigating a dynamic enterprise IT landscape marked by rapid technological change.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments