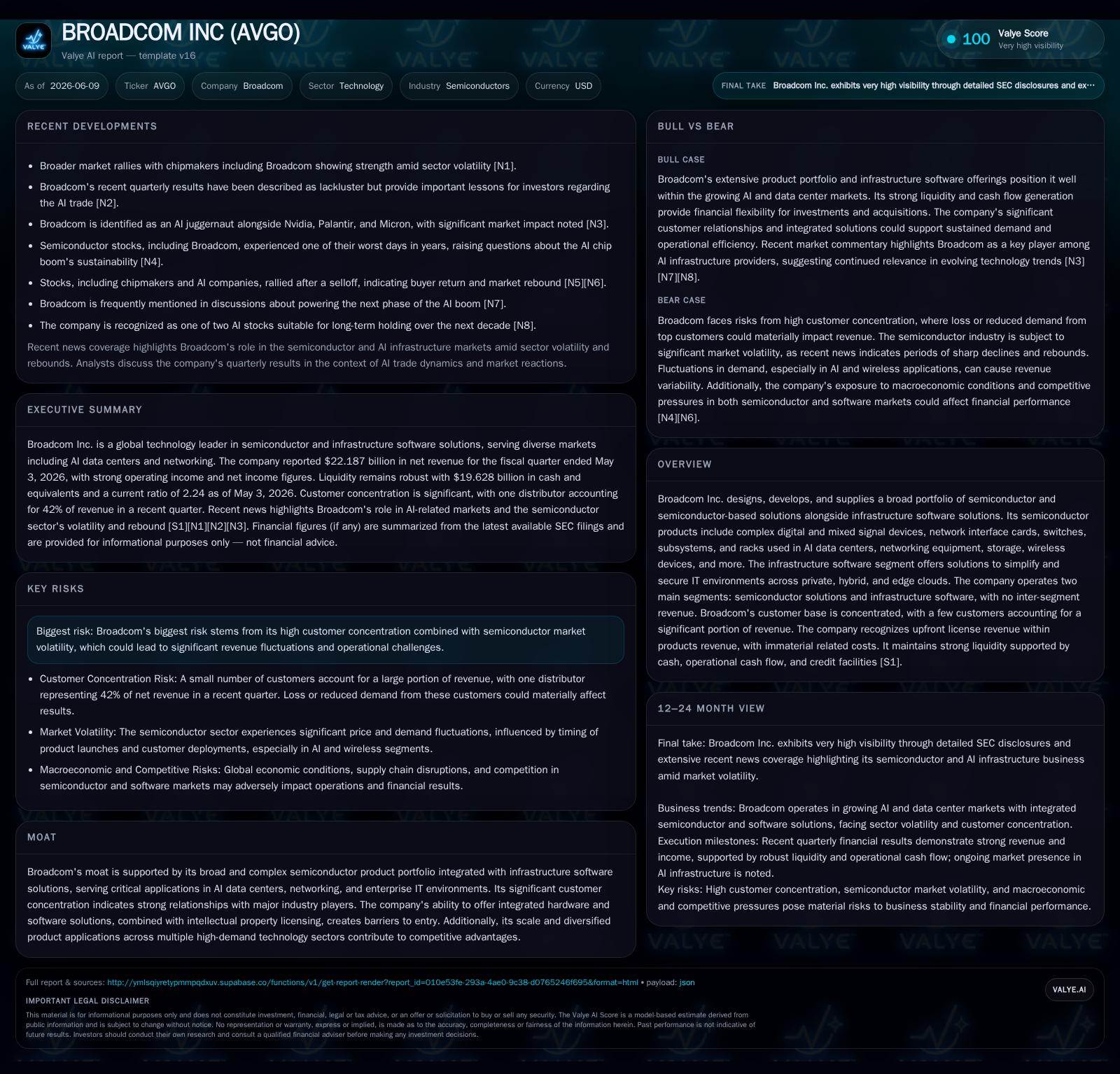

Broadcom Expands AI Exposure Amid High Customer Concentration and Debt Leverage

Latest quarter highlights Broadcom's growth in AI-capable semiconductors and infrastructure software alongside cautious balance-sheet management.

In its June 2026 quarterly filing, Broadcom Inc. showed robust revenue growth driven by semiconductor products tailored for AI data centers and networking, alongside steady infrastructure software sales. The company’s business model leverages a complex semiconductor portfolio integrated with software offerings to serve major technology customers, yet remains exposed to significant customer concentration and market cyclicality. Broadcom’s large debt position is balanced by strong liquidity and cash generation. Industry growth is anchored in structural AI adoption and cloud infrastructure expansion, but execution risks include demand volatility from key customers and lease-backed AI rack commitments.

Near-term Operating Developments Anchor Broadcom’s Strategic Position

Broadcom's latest 10-Q filing for the quarter ended May 3, 2026, reveals continued revenue acceleration driven by product innovation tailored to AI workloads and networking infrastructure [S2]. Total net revenue for the first two fiscal quarters reached $41.5 billion, up sharply from $29.9 billion year-over-year. Product revenue accounted for approximately 75% of total sales, including $3.7 billion in upfront license fees recognized within product revenue due to updated revenue recognition policies reflecting bundled semiconductor-software solutions critical for AI data centers [S2]. This shift underscores Broadcom’s strategic pivot toward integrated offerings combining hardware and software.

These results highlight Broadcom’s differentiated approach, integrating complex digital and mixed-signal ASICs with infrastructure software suites that secure and optimize hybrid cloud environments. The semiconductor portfolio includes high-performance network interface controllers, custom ASICs for AI acceleration, and storage networking chips, while the software segment delivers enterprise IT security, compliance, and cloud orchestration solutions [S1]. However, this integration also accentuates the company's significant exposure to a concentrated customer base; the top five end customers represent about 50% of net revenue, with one distributor alone accounting for over 40% of sales recently, a concentration risk typical in the semiconductor industry but requiring careful management [S19].

Business Model: Integrated Semiconductor Products with Infrastructure Software

Broadcom operates two complementary segments: Semiconductor Solutions and Infrastructure Software [S1]. The Semiconductor Solutions segment focuses on designing and supplying high-performance ASICs, network switches, and connectivity chips optimized for AI data centers, 5G wireless infrastructure, and enterprise storage. These products are typically sold directly to large technology customers or through distributors, with revenue recognized upon transfer of control. Upfront license fees, recognized as product revenue, arise from embedded intellectual property licenses within chipsets, enhancing revenue visibility and margin stability despite semiconductor market cyclicality [S2].

Margins in the semiconductor segment are influenced by advanced node manufacturing costs, wafer fabrication yields, and fab utilization rates, while the software segment benefits from higher gross margins typical of SaaS offerings. Broadcom’s ability to bundle hardware with software licenses creates a competitive moat by increasing customer switching costs and embedding its technology deeply within hyperscaler and enterprise data center architectures.

Industry Structure: High Entry Barriers and Competitive Landscape

The semiconductor industry serving AI data centers and networking infrastructure is characterized by high technical complexity, significant R&D investment, and long product development cycles. Broadcom competes with peers such as Nvidia, AMD, and Marvell, each focusing on different aspects of AI compute and networking [N2][N3]. Nvidia leads in GPU acceleration for AI training and inference, AMD offers broad CPU and GPU platforms, and Marvell specializes in networking chips. Broadcom’s unique positioning stems from its combined semiconductor and enterprise software portfolio, enabling end-to-end solutions for cloud infrastructure operators.

Customer switching costs are elevated due to proprietary ASIC designs tailored to hyperscaler specifications and the integration of Broadcom’s software into cloud management stacks. This creates a durable competitive moat but also concentrates risk among a few large customers, making order timing and volume sensitive to their capital expenditure cycles.

Growth Drivers: Structural AI Demand and Hybrid Cloud Expansion

Broadcom’s growth is anchored in the accelerating adoption of AI workloads, which drive demand for specialized semiconductors featuring high-bandwidth memory, custom interconnects, and energy-efficient architectures optimized for data center racks. The company’s lease-backed AI rack agreements, with a maximum exposure of $29 billion, represent an innovative monetization model allowing customers to access dedicated AI infrastructure without upfront capital investment, though this introduces credit and residual value risks [S22]

Simultaneously, the expansion of hybrid cloud environments fuels demand for Broadcom’s infrastructure software, which simplifies multi-cloud governance, enhances security compliance, and automates IT operations—key priorities for enterprise CIOs navigating complex cloud ecosystems post-pandemic.

Product innovation cycles focus on advancing silicon process nodes to improve performance-per-watt and increase wafer fab utilization, critical for meeting hyperscaler capacity requirements [S2]. Licensing deals tied to embedded IP within semiconductor products contribute to upfront revenue recognition, supporting margin stability amid fluctuating unit sales

Risks and Constraints: Customer Concentration and Lease-Back Exposure

Broadcom’s high dependency on a limited number of large customers exposes it to order timing volatility typical of semiconductor capital expenditure cycles. Fluctuations in wireless and AI product rollouts have recently amplified this cyclicality [S19]. The lease-backed AI rack contracts introduce additional execution and credit risks, as lessee defaults or rapid technology obsolescence could impair residual asset values. The company retains rights to repossess assets, but these arrangements complicate revenue recognition and capital allocation decisions [S22].

On the balance sheet, Broadcom carries approximately $65 billion in total debt against $19.6 billion in cash and equivalents, resulting in net debt near $47 billion as of May 3, 2026 [F1][S13]. The current ratio stands at 2.24, indicating solid short-term liquidity. Interest expense remains a significant fixed cost but is manageable given Broadcom’s investment-grade credit ratings and strong operating cash flow generation [S13]. The $7.5 billion unsecured revolving credit facility remains undrawn, providing additional liquidity buffer [S4].

What to Watch Going Forward

Key indicators to monitor include the sustainability of AI hardware bookings amid cyclical fluctuations from major customers and trends in upfront license revenue recognition, which may signal contract structure changes or demand elasticity [S2]. Execution on the lease-based AI rack deployments will be critical to commercializing this growth vector while managing associated credit risks [S22].

Continued semiconductor process technology innovation aligned with hyperscaler requirements will be essential to maintaining competitive positioning relative to peers like Nvidia and AMD, who aggressively pursue adjacent AI compute markets [N2]. Meanwhile, growth in infrastructure software adoption will help diversify revenue streams and reduce exposure to semiconductor cyclicality.

Financial Context Summary

Broadcom’s H1 FY26 net revenue of $41.5 billion was supported by a gross margin near 69%, reflecting a cost of revenue ratio around 31% [S7]. Operating expenses increased modestly, but operating income expanded due to operating leverage from topline growth. Net income rose accordingly. The company’s leverage profile includes $64.9 billion of total debt principal outstanding as of May 3, 2026, balanced by $19.6 billion in cash equivalents, maintaining covenant compliance and supporting consistent quarterly dividends [F1][S13].

Liquidity remains ample with no borrowings drawn on the revolving credit facility, allowing Broadcom to balance capital deployment between acquisitions and organic innovation [S4][S13]

Disclaimer: This analysis does not constitute investment advice or research views but aims to provide an informed perspective based on public disclosures.

Financial Position in Context

As of May 3, 2026, Broadcom held $19.6 billion in cash and equivalents against $66.7 billion in total debt, resulting in net debt of approximately $47.1 billion [F1]. Current assets of $42.2 billion and current liabilities of $18.9 billion yield a current ratio of 2.24, indicating strong short-term liquidity [F1]. This balance sheet profile supports ongoing operational needs and strategic initiatives while reflecting the company’s leveraged capital structure typical of large semiconductor and infrastructure software providers.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments