Canadian Pacific Kansas City’s Q1 2026 Update Highlights Dividend Growth and Currency Headwinds

A near-term revenue decline and tightened operating ratios reflect currency and fuel cost pressures despite robust liquidity and an expanded North American rail footprint.

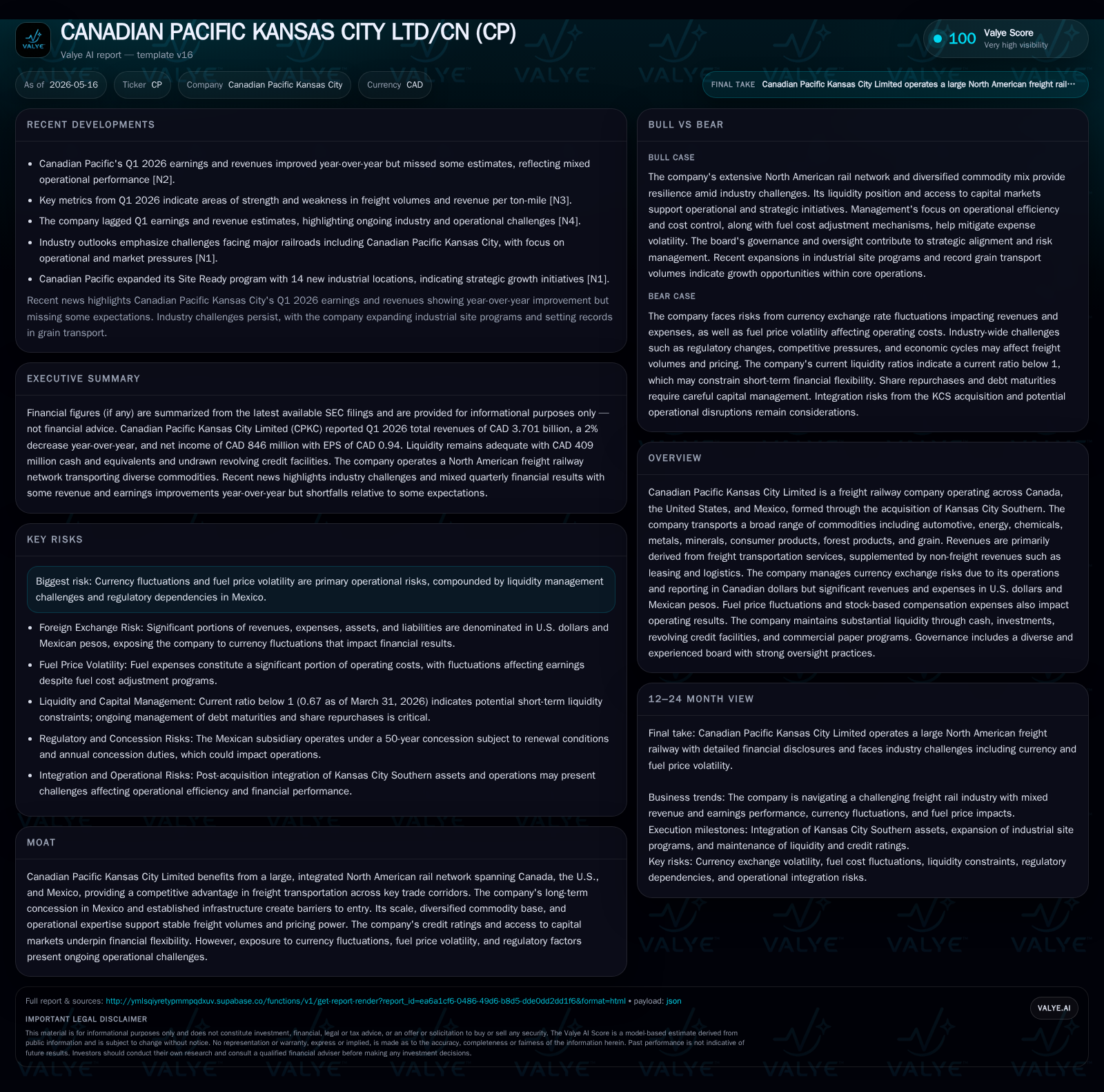

Canadian Pacific Kansas City Limited (CPKC) reported Q1 2026 revenues of CAD 3.7 billion, down 2% from the prior year, impacted by unfavorable foreign exchange movements and higher fuel expenses. The company declared a 17.5% dividend increase, signaling confidence in cash flow despite a core adjusted operating ratio that worsened by 50 basis points. CPKC’s integrated rail network spanning Canada, the U.S., and Mexico positions it strongly within key trade corridors, though currency volatility and ongoing acquisition-related costs pose operational challenges. Stable liquidity supported by cash reserves and an expanded commercial paper program buttresses the company’s financial profile amid modest volume headwinds.

Recent Operating Update

Canadian Pacific Kansas City Limited (CPKC) disclosed its Q1 2026 results on April 30, revealing total revenues of CAD 3.701 billion—down about 2% compared to CAD 3.795 billion in Q1 2025 [S2]. This decline was driven largely by foreign exchange headwinds: the U.S. dollar weakened against the Canadian dollar during this period while the Mexican peso strengthened relative to the Canadian dollar, collectively subtracting approximately CAD 82 million from reported revenues [S2]. The operational impact was further reflected in a slight deterioration in margins with the core adjusted operating ratio rising to 63.0%, up fifty basis points from last year’s comparable quarter.

Diluted EPS fell marginally by 3% to $0.94 per share with core adjusted diluted EPS— which excludes acquisition-related and purchase accounting adjustments—down by 2% to $1.04 per share [S2]. Management attributed some margin pressure to elevated fuel costs as well as stock-based compensation expenses which increased due to fluctuations in the company’s share price [S20]. Notably, CPKC announced a significant quarterly dividend hike of 17.5% to CAD $0.268 per share payable July 27, underscoring management's confidence in liquidity and long-term cash flows [S2].

Integration-related costs from the acquisition of Kansas City Southern (KCS) continue to affect GAAP figures but are excluded from core non-GAAP metrics for clearer visibility into operations [S7]. The company also highlighted ongoing management of risks inherent in currency volatility given its trilingual operational footprint across Canada (reporting currency), U.S., and Mexico [S2].

Business Model

CPKC generates revenue primarily through freight transportation services covering an extensive rail network that integrates Canadian Pacific's legacy routes with Kansas City Southern's critical corridors into Mexico—the only single-line North American railway connecting all three countries directly [S1]. Its diversified commodity mix spans automotive components, energy products like crude oil and refined fuels, various chemicals, metals/minerals, consumer packaged goods, forest products such as lumber and pulp, as well as grain shipments [S1].

Customers consist mainly of industrial shippers needing efficient bulk transportation solutions along trade corridors influenced by North American free trade agreements. Revenues depend on freight volumes transported (in carloads or tons), pricing per shipment which is influenced by commodity type and contract terms including fuel surcharges harkening market price changes [S1][S2].

The company's pricing power reflects a degree of pricing inelasticity given limited substitution alternatives for heavy or bulk cargo over continent-spanning distances where trucking is less economically viable especially over long hauls crossing borders [N9][N10]. CPKC also supplements freight revenue through ancillary offerings such as equipment leasing and logistics services enhancing customer retention via ecosystem stickiness [S1].

Currency factors complicate revenue recognition since substantial portions of income come from U.S. dollar- or Mexican peso-denominated contracts but are reported in Canadian dollars; hedging programs partially offset translation risks but residual fluctuations materially affect quarterly comparative results [S2]. Fuel cost is another key variable that significantly affects operating expenses; trending prices feed into dynamic fuel surcharge programs though timing mismatches cause interim margin variability [S2][S20].

Industry Structure and Competitive Position

Rail freight in North America combines oligopolistic dynamics with high entry barriers due to capital intensity, regulatory approvals especially for cross-border routes into Mexico governed under long-term concessions (such as CPKC's exclusive concession lasting until at least mid-century), substantial fixed infrastructure investments including tracks, terminals, and fleet maintenance facilities [S1][N9]. This backdrop limits new entrants preserving scale advantages for incumbents.

CPKC’s unique ownership of a seamless north-south corridor spanning Canada through key U.S. industrial hubs down into Mexico differentiates it strategically versus competitors like Union Pacific or BNSF who lack equivalent single-operator access across all three countries [N9][S1]. This allows CPKC to capture integrated supply chain demand flows tied to automotive manufacturing clusters across North America and agricultural export lanes.

Competitors argue on volume efficiency gains or terminal congestion; however, CPKC’s operational expertise post-acquisition focuses on synergy attainment and service reliability improvements designed to heighten competitive advantage over time [S1]. Regulatory considerations within Mexico represent notable risks affecting operational freedom but the existing concession regime currently supports stable long-term rights absent revocation [S21].

Growth Drivers

Structural growth opportunities rely on expanding North American trade volumes supported by economic fundamentals such as industrial production growth (auto assembly plants being prominent users), energy exports particularly liquefied petroleum products shipped southbound for export markets via Gulf ports, and agricultural commodities linked to rising global food demand [S1][N9].

Logistics customers increasingly seek integrated transport solutions minimizing fragmentation; CPKC can leverage its scale and geographic reach to grow ancillary services such as intermodal connections complementing truck freight networks inside metropolitan areas.

Capacity improvements afforded by ongoing capital investments enable handling higher loadings without proportional cost increases helping scale margins if volume recovers post any near-term softness seen in early 2026 [S15].

Strategic initiatives include continuous refinement of cross-border service offerings benefiting from harmonized customs procedures under USMCA rules fostering smoother rail traffic movement across contiguous nations—a durable tailwind supporting longer-haul freight economics.

Financially prudent share repurchases under current issuer bids alongside gradually increasing dividends signal disciplined capital allocation aligned with growing free cash flows once acquisition integration stabilizes [S2].

Risks / Watchpoints / Growth Constraints

Currency fluctuations remain a pivotal risk influencing both topline translation effects and expense variability; hedging mitigates but does not eliminate exposure especially when foreign exchange moves rapidly or beyond anticipated thresholds creating earnings volatility quarter-to-quarter [S2]. Fuel price volatility injects similar unpredictability given high diesel consumption relative to overall costs compounded by timing gaps between spot prices and surcharge recoveries impacting margins temporarily [S2][S20].

Acquisition-related costs from KCS integration including legal advisory fees, system migrations, employee retention incentives continue beyond initial transaction periods adding pressure on GAAP profitability even as excluded from core metrics [S7][S22]. Regulatory shifts or adverse changes in Mexico’s concession terms could hamper operational flexibility or increase duties reducing returns although no immediate threats appear disclosed [S21].

Macro sensitivity includes potential economic slowdowns dampening manufacturing output which drives railroad volumes—especially cyclical commodities like steel inputs or automotive parts—and geopolitical disruptions affecting trade flows especially given reliance on cross-border logistics corridors.

Labor relations are another latent factor common within railroad industry history; any strikes or contract disputes could disrupt network fluidity vulnerable to cascading effects across complex supply chains.

What To Watch Next

Key performance indicators will include sequential freight volume metrics broken down regionally across Canada-U.S.-Mexico lanes indicating whether industrial activity rebounds from Q1 softness noted alongside persistent FX headwinds impacting reported revenue levels. Fuel price trends relative to historical benchmarks alongside updates on fuel surcharge recoveries will be closely monitored for margin implications.

Management commentary during upcoming quarterly disclosures regarding progress toward acquisition synergy realization timelines remains critical including quantified efficiency gains or integration cost run rates narrowing clarity around normalized profitability.

Dividend payout evolution coupled with share repurchase activity offers insight into cash flow stability serving as a proxy for underlying business health especially if incremental capex remains controlled below depreciation rates supporting return on invested capital expansion.

Additionally, regulatory developments around North American trade policy or procedural enhancements impacting rail border crossings could emerge as catalysts altering operating conditions favorably or unfavorably.

Financial Profile Summary

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | 409,000,000 CAD | |

| 2026-03-31 | ||

| Total debt | $14.7bn | |

| 2025-12-31 | ||

| Net debt | $14.3bn | |

| 2025-12-31 | ||

| Current assets | 3,404,000,000 CAD | |

| 2026-03-31 | ||

| Current liabilities | 5,069,000,000 CAD | |

| 2026-03-31 | ||

| Current ratio | 0.67x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

As at March 31, 2026, CPKC held CAD 409 million in cash & equivalents with current assets totaling CAD 3.4 billion versus current liabilities of CAD 5.07 billion yielding a current ratio of approximately 0.67 indicating tight near-term liquidity coverage typical for capital-intensive carriers [F1]. Total debt stood near USD 14.69 billion at end-2025 with net debt slightly lower after accounting for cash holding approximating USD 14.28 billion reflecting substantial leverage balanced against robust cash flow generation potential post-merger scaling effects [F1].

Liquidity is bolstered by undrawn revolving credit facilities totaling USD 2.2 billion (maturing through mid-2030) plus commercial paper issuance capacity recently expanded from USD 1.5 billion to USD 2.2 billion allowing flexible short-term funding options amid working capital needs or opportunistic debt refinancing activities [S17]. Interest expense trends will reflect recent refinancings including issuance of new unsecured notes at favorable coupon rates enhancing debt maturity profile while containing borrowing costs amidst low interest rate environments.

Disclaimer

This analysis is based on reported SEC filings including the latest Form 10-Q dated April 30th, 2026 alongside supporting news sources current as of mid-May 2026 ([S1], [S2], [S3], etc.). Financial figures reflect IFRS/GAAP consolidated statements converted predominantly into Canadian dollars unless otherwise noted ([F1]). This report aims solely to provide a factual summary combined with domain-informed interpretation without offering investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments