SHOP Unveils New Growth Catalysts in Q1 Report Amid AI Platform Expansion

SHOP's latest quarterly filing spotlights accelerating revenue growth and strategic AI-driven product enhancements amid ongoing profitability challenges.

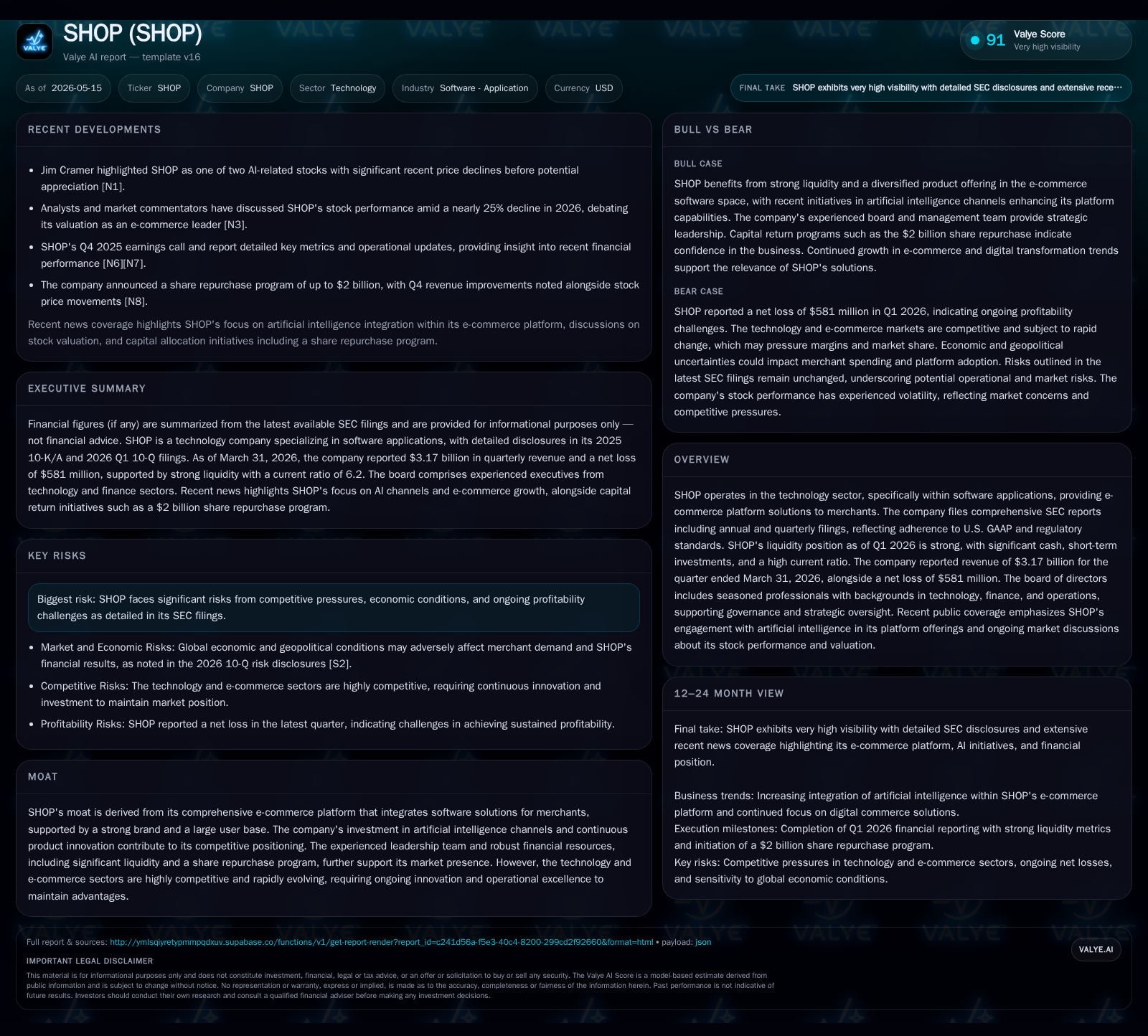

In Q1 2026, SHOP reported $3.17 billion in revenue, reflecting robust expansion driven by its integrated e-commerce platform and new artificial intelligence (AI) capabilities. Despite a net loss of $581 million, management highlights AI-powered tools and evolving merchant solutions as key levers for future growth. The company's business model centers on recurring subscriptions and transaction-based fees within a competitive landscape shaped by giants like Amazon and MercadoLibre. Near-term growth hinges on successful AI integration and increasing merchant adoption, while risks include intense competition, margin pressures, and macroeconomic uncertainties.

Latest Quarterly Operating Update and Why It Matters

SHOP's 10-Q filing dated May 5, 2026 [S2] reveals a pivotal quarter with revenue scaling to $3.17 billion for Q1, underscoring a continuation of strong top-line momentum despite persistent net losses totaling $581 million. This juxtaposition reflects SHOP’s deliberate investment in expanding its platform capabilities, particularly in artificial intelligence (AI), an emphasis outlined by management as a foundational growth catalyst going forward. The tension between top-line acceleration and bottom-line drag signals a business still operating in build-and-scale mode rather than harvesting profits.

Management commentary highlights that AI-enabled commerce tools such as "Sidekick"—an AI-powered assistant embedded within the platform—are already materially expanding merchant capabilities. This heightened functionality aims to enhance merchant retention and increase monetization through deeper engagement with the Shopify suite. While investor sentiment remains mixed, news narratives note the stock's volatility amidst these transformative technology bets [N1][N5].

SHOP’s Business Model and Value Proposition for Merchants

Shopify operates a multisided e-commerce platform that generates revenue primarily through subscription fees paid by merchants plus transaction-based service fees correlated to gross merchandise volume (GMV) flowing through its channels [S1]. Merchants ranging from small startups to large enterprises pay monthly or annual fees for access to Shopify’s software tools enabling storefront creation, payment processing, order management, marketing integrations, and increasingly AI-powered features.

The platform's strength lies in its integrated ecosystem which reduces merchant friction with onboarding, scales across sales channels (online, social commerce, POS), and facilitates third-party app extensions. This creates a high switching cost environment where merchants benefit from accumulated investments in their customized Shopify experience. Pricing power is nuanced; recurring SaaS fees provide stable revenue while transaction fees offer variable upside linked to merchant success.

Importantly, Shopify's recent infusion of AI elements—such as predictive analytics for sales trends and personalized customer recommendations—adds differentiation to its service quality. These innovations aim at structural improvements in merchant operational efficiency rather than cyclical demand spikes, signaling durable revenue enhancements if adoption continues positively.

Competitive Positioning in the E-Commerce Platform Industry

SHOP competes primarily against tech giants like Amazon (which operates a marketplace rather than pure SaaS), MercadoLibre with its Latin American dominance, and various niche vendors targeting SMB segments [N9][N8]. Unlike marketplaces that directly sell products, Shopify’s platform model positions it as an enabler rather than competitor to merchants’ own branded commerce efforts.

The company maintains competitive advantages through brand reputation, platform extensibility, API integrations, developer ecosystem vibrancy, and its commitment to embedding emerging technologies like AI early in the product lifecycle. However, the SaaS e-commerce market faces commoditization risks: competitors continue aggressive pricing strategies to capture share especially among price-sensitive users.

Regulatory scrutiny over data privacy and cross-border commerce adds complexity but also enforces barriers that may limit smaller entrants’ ability to match Shopify’s scale rapidly [S1]. Thus, while competitive intensity is acute, Shopify’s ecosystem depth grants it differentiated resilience.

Emerging Growth Drivers: AI Integration and Merchant Adoption Trends

The notable driver spotlighted in recent filings is the accelerated rollout of AI capabilities embedded across Shopify’s product suite [S2]. Tools like Sidekick provide merchants with adaptive commerce assistance including inventory optimization suggestions, targeted marketing creatives generation, and automated customer service support.

News commentary emphasizes how these innovations could incrementally boost average revenue per user (ARPU) by deepening usage intensity and facilitating upsell into higher-tier subscription plans [N4][N5]. Additionally, enhanced platform intelligence may reduce churn by improving merchants’ margins through operational cost savings.

This approach also aligns well with scalability objectives: automated AI features reduce need for extensive human support as merchant base grows globally. Hence SHОP views AI as not merely a defensive capability but a structural accelerator enabling broader market penetration into under-served segments or regions where hands-on support is less feasible.

Risks and Challenges Impacting Growth Trajectory

Despite promising technology steps, risks remain elemental. SHOP explicitly reiterates from prior filings that macroeconomic headwinds could dampen discretionary consumer spending affecting merchant volumes [S2][S9]. Also notable are sustained losses stemming from heavy research & development expenditure necessary to maintain technological leadership—a double-edged sword pressuring margins amid competitive price sensitivity.

Market skepticism persists around whether Shopify can differentiate sufficiently against entrenched rivals such as Amazon whose marketplace pull remains formidable [N6][N9]. Geopolitical tensions pose cross-border commerce uncertainty potentially constraining international expansion initiatives.

Operationally balancing rapid innovation against scaling complexity without degrading service quality or overextending costs will be critical. Any missteps may impair customer retention or stall ARPU progression undermining long-term value creation.

Upcoming Catalysts and Key Indicators to Monitor

Looking ahead, investor attention should focus on milestones tied to further phases of AI feature deployment across Shopify’s ecosystem documented in corporate disclosures [S3]. Metrics signaling success include sustained subscriber count growth within various merchant tiers, incremental ARPU increases driven by premium offerings adoption considering price elasticity nuances, and monitored churn ratios reflecting stickiness gains.

Additional events such as the Annual General Meeting scheduled post-filing (May 2026) provide forums for strategic updates from management reinforcing or recalibrating growth narratives [S3].

Tracking evolving regulatory frameworks impacting digital commerce globally will also be important given their influence on platform compliance costs and operational flexibility.

Disclaimer

This analysis is based solely on information available through May 15, 2026, including SEC filings and public news sources cited herein. It does not constitute investment advice or recommendations but aims to provide an informed industry perspective on SHOP’s operational positioning and strategic dynamics.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments