PENN Entertainment’s Q1 2026 Results Signal Resilience Amid Digital Transition

Q1 2026 showed mixed financial outcomes but underscored PENN's strategic strength in retail and digital gaming integration.

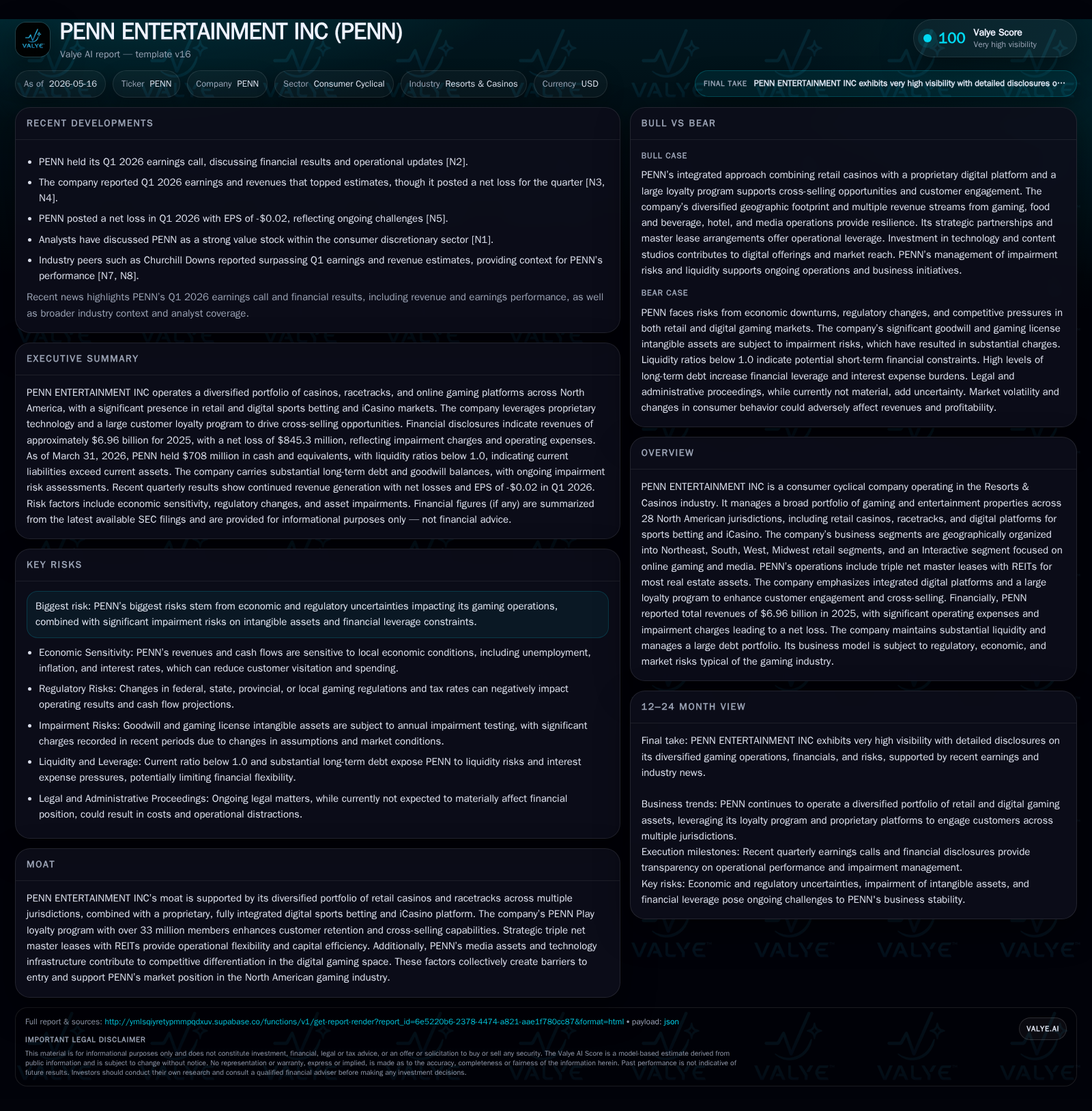

In the first quarter of 2026, PENN Entertainment demonstrated resilience with positive revenue trends in its retail segments, supported by a broad North American footprint and a growing digital interactive business. Despite ongoing impairment charges and operational cost pressures that impacted net income, the company’s triple net master lease model with REITs and its loyalty program provide competitive advantages. Regulatory complexity remains a challenge, but PENN’s integrated digital platform and cross-selling opportunities position it well for continued growth.

Q1 2026 Operating Update Reflects Mixed Signals

PENN Entertainment's Q1 2026 filing [S2] reveals a nuanced operating picture. While retail casino revenues benefited from steady demand across its geographically diversified portfolio covering Northeast, South, West, and Midwest segments, the interactive (digital) segment continues to face headwinds impacting profitability. The company reported significant impairment charges in the period consistent with prior quarters, which weighed on net results alongside elevated operating expenses. The recent 8-K event filing dated April 23, 2026 [S3] reiterated these themes and confirmed that no material changes occurred to previously disclosed risk factors [S2], maintaining focus on operational execution during these pressures.

The company's integrated approach means retail gaming brings stable cash flow generation while the interactive segment is strategically emphasized for growth despite short-term challenges. This balance underpins PENN’s near-term outlook.

Integrated Business Model Across Retail and Interactive Segments

Based on PENN’s latest annual report [S1], the company operates a comprehensive portfolio of gaming assets including casinos, racetracks, hotels, and related hospitality offerings situated within 28 jurisdictions throughout North America. The business segments organize geographically into Northeast, South, West, Midwest retail units complemented by an Interactive segment responsible for online sports betting (OSB) and iCasino operations.

A distinctive feature is PENN's reliance on triple net master leases covering most real estate assets leased predominantly from specialized REIT partners like Gaming and Leisure Properties (GLPI). This structure transfers building ownership risks to the REITs while providing PENN operational control of gaming properties—a notable element enhancing capital efficiency. These leases are long-term agreements often indexed to property values including land, buildings, racetracks, and boats where applicable [S1].

The interactive business benefits from a proprietary digital platform combined with an in-house iCasino content production studio—enabling differentiated offerings beyond mere aggregation of third-party games. This integration supports cross-channel customer engagement via PENN Play loyalty program membership exceeding 33 million users, fostering robust omni-channel retention.

Competitive Moat Fueled by Master Leases and PENN Play Loyalty Program

PENN’s competitive positioning is reinforced by several structural advantages. Most notably, the triple net master lease arrangements not only reduce real estate capital commitments but serve as significant entry barriers relative to competitors who must either own large real estate footprints or face heavy capital expenditure requirements.

Additionally, the PENN Play loyalty program provides a vital ecosystem effect; its large membership base enables personalized marketing campaigns linking physical venue visits with digital wagering behavior. This synergy elevates switching costs for consumers while optimizing lifetime value through rewards tailored across gaming verticals.

The company also maintains media assets that support promotional reach alongside proprietary technology infrastructure—further differentiating PENN’s market offer versus peers reliant on third-party platforms or pure-play operators. The combination creates moat-worthy results through deep market entrenchment both offline and online.

Industry Dynamics: Regulation, Competition, and Capacity Constraints

Operating across multiple states imposes complex regulatory dynamics that directly influence PENN’s cost structure and growth potential [S1; Valye report excerpt]. Gaming licenses are treated as indefinite-lived intangibles but require annual impairment tests due to the uncertainty surrounding regulatory renewals or potential tax escalations.

The sector remains capital intensive given physical casino expansion barriers such as limited land availability near population centers and stringent zoning restrictions. Traditional brick-and-mortar segments therefore have constrained capacity upside absent costly expansions or new licenses.

Digital wagering segments encounter intensifying competition from national operators scaling across states alongside ongoing legal/regulatory uncertainties around mobile sports betting legalization timelines and tax regimes. Pricing power is variable—subject both to promotional spend intensity online and regulated limits on house edge in various jurisdictions.

Overall PENN sits within a challenging industry environment requiring nimble regulatory navigation while leveraging scale economies through its multi-jurisdictional footprint.

Growth Catalysts: Digital Expansion and Cross-Selling Opportunities

Growth driver differentiation lies chiefly in PENN’s continued investment in its integrated digital ecosystem. Its interactive platform leverages proprietary data analytics sourced from retail consumer patterns enabling targeted promotions designed to convert casual bettors into loyal users [S1].

Expansion of iCasino offerings facilitated by the internal content studio coupled with broadened geographical market presence stand out as key catalysts supporting active user count growth as well as deeper wallet shares per player.

Complementing this is aggressive cross-selling facilitated via the loyalty program that unifies retail casino visitation incentives with online wagering bonuses—a model proving effective at increasing customer frequency everywhere from traditional casino floors to mobile app usage.

Success metrics to monitor include subscriber activations within PENN Play’s interactive verticals as well as digital gross gaming revenue per active user—both drivers toward sustainable margin improvements despite current headwinds.

Risks and Constraints: Regulatory Uncertainty and Asset Impairments

Risk assessment from latest filings underscores concerns around goodwill impairments specifically linked to the Interactive reporting unit’s valuation—the goodwill balance stood at $774.8 million at end-2025 with prior impairments recorded at $825 million due to carrying amounts exceeding fair value [S1]. These figures highlight sensitivity to future cash flow assumptions susceptible to changes in regulatory regime shifts or competitive pressures.

Economic volatility affecting discretionary consumer spending also poses downside risk exacerbated by inflationary cost inputs experienced at retail properties.

Financial leverage considerations remain critical; while covenant-compliant currently [S2], concentrated maturities over the next few years necessitate careful capital management especially given the sizeable revolving credit utilization documented in recent filings.

Altogether these risks form essential watch points but do not detract from company resilience supported by diversified operations.

Upcoming Milestones and What to Watch Next

Key near-term milestones include monitoring subsequent quarterly earnings results for updates on segment revenue mix dynamics particularly growth trajectories within the Interactive segment reflecting penetration gains or losses [S2][S3].

Master lease renewal negotiations constitute another critical milestone affecting future cost bases given their influence on rent expense profile tied back to underlying asset values.

Digital product launches or enhancements scheduled for rollout should be observed closely since technological innovation serves as a bellwether for potential accelerations in active user acquisitions or retention improvements reported during earnings calls such as those summarized around Q1 earnings day transcripts [N2][N4].

Regulatory approvals or policy changes impacting permitted gaming modalities across served jurisdictions should also figure prominently among watchlist items given their direct impact on accessible market sizes.

Latest Financial Snapshot and Capital Structure

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $708mm | |

| 2026-03-31 | ||

| Current assets | $1161mm | |

| 2026-03-31 | ||

| Current liabilities | $1416mm | |

| 2026-03-31 | ||

| Current ratio | 0.82x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value |

|---|---|

| Cash & Equivalents | $708 million |

| Current Assets | $1.16 billion |

| Current Liabilities | $1.42 billion |

| Current Ratio | 0.82 |

As of Q1 2026 end [F1], PENN retains a substantial cash reserve of $708 million providing liquidity cushion amid operational complexities.

The company remains compliant with financial covenants under amended credit facilities as indicated in its recent quarterly filings [S2]. This capital structure underpins capacity for strategic investments including digital innovation while managing legacy obligations prudently.

This analysis is based solely on publicly reported information without any consideration or incorporation of material non-public details. It aims to provide a balanced understanding of PENN Entertainment Inc.'s strategic positioning shaped by recent quarterly disclosures alongside historical context within regulated North American gaming landscapes.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments