Genesco’s Omni-Channel Execution and Footprint Optimization Drive Early Fiscal 2027 Sales Growth Despite U.K. Headwinds

Genesco reports improved operating margins and comparable sales gains, offset by U.K. market softness and tariff pressures, signaling focused brand portfolio management.

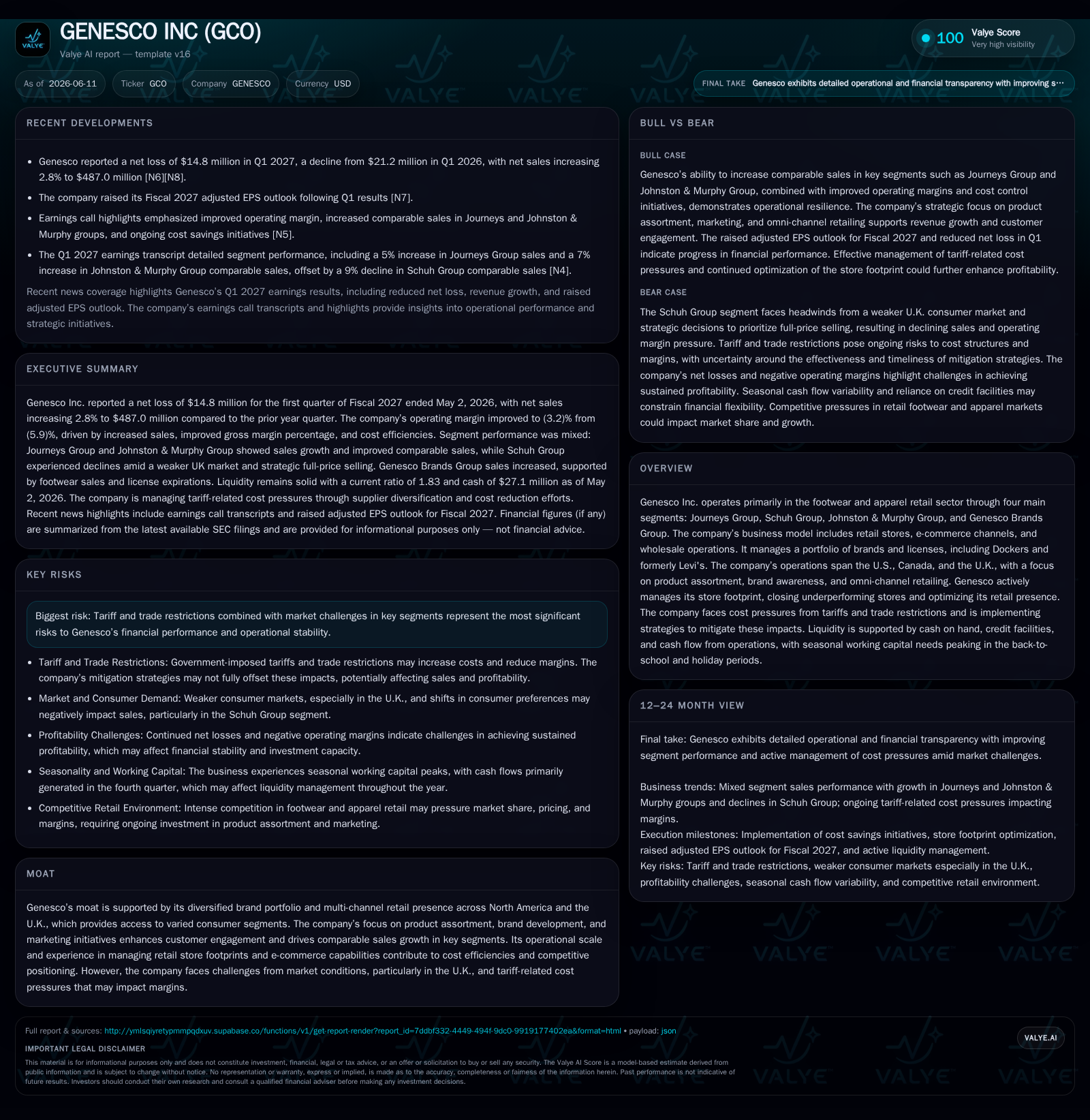

In the first quarter of fiscal 2027, Genesco achieved a 2.8% net sales increase driven primarily by strong comparable sales growth in the Journeys and Johnston & Murphy segments. The company’s ongoing footprint optimization continues to reduce store count while boosting same-store sales and online penetration, reflecting effective omni-channel retail strategies. However, Schuh Group faced declining sales due to weaker UK conditions and a strategic shift toward full-price selling. Margin improvements benefit from lower markdowns and cost efficiencies, even as tariff pressures present continued challenges. Genesco’s liquidity remains ample to support working capital needs ahead of seasonal peaks.

Recent Operating Update Anchored in Q1 Fiscal 2027 Results

Genesco Inc.’s latest quarterly filing for the period ended May 2, 2026, reveals cautious but tangible progress across its diversified retail business segments amidst complex external pressures [S2]. Net sales advanced 2.8% to $487 million, propelled primarily by increases in comparable sales (+2%) and same-store sales (+3%). These gains materialized despite an overall reduction in store count due to ongoing footprint optimization efforts designed to shutter underperforming locations and improve portfolio quality.

Notably, Journeys Group recorded a robust 5% increase in comparable sales led by strength across athletic and casual footwear categories. This segment benefited from sustained product assortment relevance paired with omni-channel retailing gains through both physical stores and e-commerce channels [S2]. Similarly, Johnston & Murphy Group witnessed a notable 7% jump in comparable sales driven by successful expansion in store traffic complemented by digital marketing initiatives enhancing brand awareness. The infusion of social media-driven campaigns bolstered consumer engagement with both apparel and footwear products [S2].

Conversely, Schuh Group experienced softness with a 9% drop in local currency comparable sales [S2]. The company attributes this decline primarily to challenging macroeconomic conditions within the UK retail market compounded by strategic inventory positioning favoring full-price selling instead of discounting promotions — an initiative aimed at protecting margin integrity amidst cost headwinds from tariffs

The Genesco Brands Group contributed positively with net sales rising nearly 4%, buoyed by increased footwear demand for Dockers and private label products following the expiration of the Levi’s licensing agreement in May 2026 [S2]. This portfolio streamlining aligns with management’s strategy to focus on proprietary brands possessing clearer growth trajectories.

Business Model: Multi-Segment Omni-Channel Retail Focused on Brand Portfolio Management

Genesco operates four primary business segments spanning specialty footwear retail via Journeys Group and Schuh Group; upscale apparel-footwear combinations via Johnston & Murphy; and brand management/licensing through Genesco Brands Group [S1]. Revenue is generated through direct-to-consumer storefronts primarily located in malls or shopping centers across North America and the U.K., alongside growing e-commerce platforms that enable consumers to shop seamlessly across channels.

A distinctive aspect of Genesco’s business model is its active management of store footprint complemented by multi-brand product assortments that appeal to diverse consumer tastes from youth athletic styles at Journeys to heritage footwear at Johnston & Murphy. The company pursues aggressive omni-channel integration including online merchandising, mobile commerce, digital marketing campaigns, loyalty programs, and fulfillment options that drive incremental volume resulting in higher same-store sales productivity despite rationalized physical presence [S1], [S2].

Wholesale distribution remains important especially for licensed brands like Dockers prior to the Levi’s exit but has been consciously de-emphasized where margins erode profitability or dilute retailer positioning.

Cost control takes center stage given industry-wide tariff pressures increasing landed costs for imported footwear components—partially visible as margin headwinds particularly at Schuh Group—but partly mitigated through supply chain efficiencies such as reduced shipping expenses noted in recent quarters [S2]. Selling and administrative expenses remain relatively stable as a percentage of revenue owing to expense discipline despite incremental investments in performance-based incentives aligned with growth objectives.

Industry Structure and Competitive Position

The global footwear and apparel retail industry is characterized by rapid shifts in consumer fashion preferences combined with intense competition from branded specialty retailers (e.g., Foot Locker), vertically integrated brand owners (e.g., Deckers Outdoor), as well as fast-growing digital-first apparel sellers.

Genesco situates itself as a multi-channel operator with moderate geographic diversification covering U.S., Canada (Journeys expansion), and U.K. markets (Schuh). Its portfolio diversity cushions exposure to localized market turbulence but also complicates operational execution especially given distinct regulatory environments impacting tariffs and currency fluctuations.

Footprint optimization aligns with an industry-wide trend toward reducing mall store saturation amid rising online penetration levels; however, maintaining customer loyalty requires balancing physical showroom utility against efficient inventory turns achieved digitally—a challenge that Genesco manages via integrated product assortments agilely adjusted for consumer demand signals.

Peer companies face similar pressures: gross margin mix depends heavily on markdown cadence controlling inventory obsolescence risks; marketing spends increasingly allocate budget between traditional displays versus social media-driven engagement; e-commerce channel penetration is critical albeit costly due to fulfillment complexity; all underpinning competitive sensitivity tied to pricing power limitations.

Growth Drivers Supporting Trajectory into Fiscal Year 2027

Key growth levers center on three thematic pillars:

- Omni-Channel Synergy: Genesco leverages connectivity between its brick-and-mortar Journeys locations and its expanding e-commerce platform to drive foot traffic increases along with higher average transaction values. Its marketing campaigns targeting youth demographic affinity for athleisure styles sustain momentum.

- Brand Portfolio Management: Discontinuation of Levi's licensing allows Genesco Brands Group to focus resources on Dockers footwear lines plus private label development which recorded measurable top-line gains (+3.9%) this quarter [S2]. This focus reduces complexity while targeting higher-margin proprietary labels.

- Footprint Optimization: Selective store closures trim unproductive assets reducing occupancy costs while concentrating efforts on high-performing Journeys stores resulted in steady same-store sales growth (+3%) despite fewer stores overall [S2]. This disciplined approach augments profitability potential when combined with improved gross margin mix driven by promotional restraint.

Additionally, Johnston & Murphy’s targeted marketing investment enhances brand equity crucial for sustainable revenue expansion through both physical retail experiences and direct-to-consumer digital channels.

Risks and Growth Constraints

Several cautionary factors remain salient:

- Tariff Impact Uncertainty: Ongoing trade restrictions inflate the textile/apparel cost base creating pricing pressure that could limit gross margin expansion particularly for segments reliant on wholesale or imported products (notably Schuh) [S2].

- UK Market Challenges: Schuh's declining sales amid UK economic softness may prolong recovery or necessitate deeper strategic changes limiting short-term profitability gains.

- Inventory Management Complexity: Balancing full-price selling against necessary markdowns involves execution risk given seasonality-driven stock accumulation preceding key gift-giving periods; inefficient turns or excessive discounting could squeeze margins.

- Competitive Intensity: High competition from digitally native brands or price-led discount retailers necessitates continuous innovation around customer experience enhancements, product assortment relevance, and cost structure advantages.

- Operational Costs: While SG&A expenses declined slightly relative to sales this quarter due to cost control measures, upward pressure from incentive compensation highlights potential volatility in fixed versus variable cost balancing.

What to Monitor Next

Investors should track several forthcoming indicators:

- Subsequent quarterly updates for trajectory of Schuh Group recovery or further contraction amid UK conditions.

- Progress on omni-channel revenue mix including e-commerce penetration rates across all segments as digital transformation initiatives mature.

- Inventory turnover ratios around midyear benchmarks indicating efficacy of merchandise planning leading into back-to-school season.

- Gross margin trends isolating tariff impact vis-à-vis promotional markdown cadence adjustments across Journeys versus Johnston & Murphy.

- Continued liquidity metrics post-Q1 including cash flow from operations during peak seasonal investment periods affecting working capital cycles [F1], [S2].

- Marketing campaign effectiveness measured via boosted average transaction values or foot traffic increases supporting top-line leverage.

Financial Profile Highlights From Latest Quarterly Data

Seasonal working capital demands typically swell midyear ahead of back-to-school and holiday spikes, aligning investment timing alongside expected Q4 cash generation cycles — critical timing points for cash flow analysis going forward [S2]

Disclaimer: This analysis presents an independent assessment based solely on publicly available SEC filings ([S1], [S2], [S3]) supplemented with contemporaneous news reports () without any forward-looking investment advice or research views regarding Genesco Inc.'s securities or operations.

Financial position in context

As of 2026-05-02, companyfacts shows $27 million in cash and equivalents and $45 million of total debt [F1]. The same snapshot implies net debt of roughly $18 million, keeping balance-sheet context relevant but secondary to the operating story [F1]. Current assets of $596 million and current liabilities of $325 million imply a current ratio near 1.83x for 2026-05-02 [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments