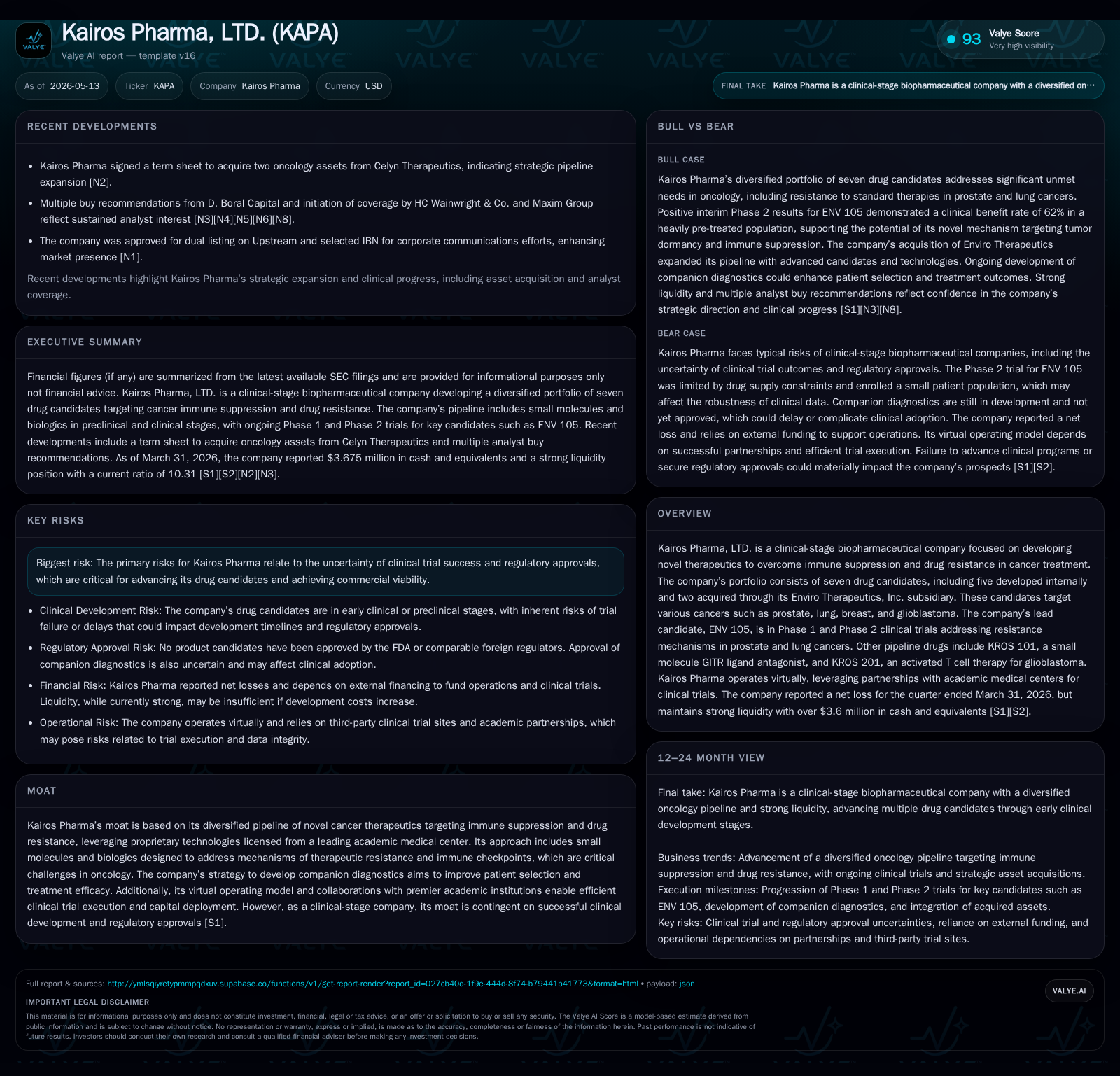

Kairos Pharma Strengthens Oncology Portfolio in Latest Quarter

Kairos Pharma’s recent 10-Q filing reveals a transformative asset acquisition and strategic progress advancing its diversified immuno-oncology development pipeline.

In the Q1 2026 10-Q, Kairos Pharma formalized a binding term sheet to acquire worldwide rights to CL-273, an investigational pan-EGFR inhibitor targeting resistant non-small cell lung cancer, via a share issuance conferring a 16.5% equity stake to the counterparty. This acquisition materially broadens Kairos’ clinical-stage oncology portfolio alongside ongoing Phase 1/2 trials of ENV105 for prostate and lung cancers. Operated as a virtual biotech, Kairos leverages academic partnerships and outsourced cGMP manufacturing, emphasizing immune checkpoint modulation and resistance reversal. Despite ongoing net losses, the company maintains strong liquidity with a current ratio exceeding 10x as of Q1 2026, enabling near-term trial progress and pipeline advancement. Key risks persist from clinical/regulatory uncertainties and equity dilution from financing requirements.

Latest Operating Update Highlights Strategic Asset Acquisition

Kairos Pharma disclosed in its May 13, 2026 quarterly report (10-Q) the significant development of entering a binding term sheet to acquire 100% of worldwide rights to CL-273 from Celyn Therapeutics. The deal consideration comprises issuing shares to Celyn representing 16.5% fully diluted ownership of Kairos upon closing, potentially combining common stock and non-voting convertible preferred shares to comply with NYSE American rules and secure shareholder approval. Furthermore, milestone payments up to $15 million are due at NDA/BLA approval alongside ongoing royalties set at 2% of U.S. net sales revenue for CL-273.

CL-273 is described as a reversible wild-type sparing pan-EGFR small-molecule inhibitor aimed at targeting EGFR mutant-driven non-small cell lung cancer (NSCLC), where resistance to standard therapies is prevalent — complementing Kairos' existing focus in lung and prostate oncology therapeutics [S2][S3][S6]. The acquisition also brings related intellectual property rights, manufacturing control, and commercialization potential under Kairos' umbrella.

Parallel to this strategic expansion, Kairos extended its manufacturing collaboration with Lonza Sales AG by adding an amendment covering standards testing and manufacturing preparations for its ENV105 antibody candidate's Phase 2 trial. This staged development agreement involves payments totaling approximately $2 million aligned with thirteen progressive milestones relating to process validation reflecting the cGMP-compliant supply chain rigor vital to regulatory adherence in biopharma [S6].

These developments signal a deliberate pivot from purely internal R&D assets towards bolstering clinical-stage breadth through external acquisitions while maintaining disciplined capital deployment within its virtual operating model.

Business Model: Diversified Oncology Pipeline Focused on Immune Evasion

Kairos Pharma operates as a clinical-stage biopharmaceutical company pioneering therapeutics that target immune suppression and drug resistance pathways common in solid tumors such as prostate cancer, lung cancer, breast cancer, and glioblastoma. Their portfolio features seven drug candidates — five internally developed plus two integrated via their Enviro Therapeutics subsidiary acquisition — leveraging licensed proprietary technologies primarily sourced from Cedars-Sinai Medical Center.

The company advances small molecules acting on immune checkpoints (like GITR ligand antagonists) as well as biologics including activated T cell therapies designed to attack cancer stem cells or modulate tumor microenvironments that contribute to therapeutic resistance. The mission is explicitly centered on reversing molecular mechanisms allowing tumor cells to evade immune surveillance or standard chemotherapeutic effects.

Significantly, Kairos employs a 'virtual operating model,' outsourcing all manufacturing activities to third-party vendors compliant with current Good Manufacturing Practices (cGMP), notably exemplified by agreements with Lonza for production support. Clinical trials themselves are conducted in partnership with leading academic medical institutions that also co-develop companion diagnostics—tools intended to refine patient selection by identifying biomarker profiles predictive of treatment efficacy.

Revenue generation is currently non-existent given all candidates remain unapproved; future income streams depend on successful regulatory approvals followed by potential direct commercialization or licensing collaborations. Milestone payments and royalties represent secondary revenue avenues tied to partnered assets transitioning onto market [S1][S6][S18].

Industry Structure and Competitive Positioning in Immune-Modulatory Therapies

Within the competitive milieu of immuno-oncology biotechs tackling immune suppression checkpoints and drug resistance pathways, Kairos differentiates itself through both breadth—covering multiple cancers—and modality diversity—including small molecules alongside cell therapies.

Their dependence on academic partnerships aligns with norms among clinical-stage biotechs aiming for nimble R&D without fixed infrastructure burdens. However, this virtual structure introduces constraints in manufacturing scalability control because production capacity hinges on vendor capabilities under third-party contracts—an industry-wide challenge impacting timing predictability especially in transitioning from early-phase trials to pivotal studies or commercialization.

Regulatory complexity remains high: obtaining FDA clearance involves stringent requirements not only for safety/efficacy data but also verification that manufacturing complies with Good Laboratory Practice (GLP) and cGMP standards throughout all phases.

Among peers focusing on similar immune checkpoint targets or resistance pathways (e.g., companies developing PD-1/PD-L1 inhibitors or novel T cell engagement platforms), Kairos occupies an early stage but strategically diversified position that mitigates pipeline risk yet requires material capital investment before product revenues arise [S1][S6]. Pricing power assumptions will depend heavily on clinical proof points demonstrating superiority or additive benefit over existing therapies addressing unmet needs caused by treatment-refractory tumors.

Growth Drivers: Clinical Milestones, Partnership Ecosystem, and Therapeutic Innovation

Three principal levers underlie near-term growth potential:

Clinical Trial Progress: ENV105’s advancement through Phase 1 and Phase 2 trials targeting resistance mechanisms in prostate and lung cancer stands central. Successful enrollment completion, safety/tolerability data release, and efficacy markers will be critical KPIs influencing investor sentiment and strategic partner interest.

Integration of CL-273 Acquisition: Following definitive agreement finalization contingent on shareholder approvals and customary closing conditions, ramping up IND-enabling studies or initiating first-in-human trials for CL-273 establishes an expanded lung cancer franchise addressing EGFR mutant variants resistant to current targeted agents.

Companion Diagnostic Development: Enhancing precision medicine approaches via diagnostics tied directly to molecular mechanisms supports better patient stratification — improving trial success probability while creating differentiation barriers vis-à-vis competitors.

Additionally, expansion of relationships with academic centers facilitates trial site access while mitigating overhead costs inherent in direct clinical management. Internal innovation led by scientists closely affiliated with Cedars-Sinai Medical Center fosters proprietary technology generating new therapeutic candidates enhancing future pipeline depth [S1][S3][S6].

Risks and Constraints: Clinical, Regulatory, and Financing Challenges

Kairos’ clear dependence on positive clinical outcomes creates inherent volatility; failure at any pivotal trial phase could significantly impair valuation absent revenue streams or diversified approved products. Multiple candidates undergoing early-stage development amplify compound program risk.

Regulatory risk remains pronounced given evolving FDA expectations around immuno-oncology agents particularly when novel mechanisms or combination regimens are involved.

Financing constraints constitute material risk vectors: net losses exceed $5 million (reported for FY2025), necessitating ongoing capital raises through equity offerings which have historically caused dilution pressures on existing shareholders given lack of sale revenues. The recent acquisition deal terms accentuate this dynamic by issuing substantial equity (~16.5%) potentially diluting both voting power and economic share proportionally unless offset by significant value accretion post-integration.

Operationally, reliance on outsourced manufacturing demands precise coordination; any vendor delays or compliance shortfalls might defer key milestones causing cash burn beyond forecasts. The company’s tight cash runway also elevates fundraising execution risks amid challenging biotech capital markets conditions lacking near-term commercial revenue visibility [S2][S12].

Upcoming Catalysts: Trial Readouts, Regulatory Milestones, and Capital Strategy

Crucial upcoming inflection points include:

- Official closing of the CL-273 acquisition post customary due diligence completion and shareholder votes anticipated within H1/H2 2026 timeline.

- Enrollment status updates along with interim results from ENV105’s Phase 2 studies potentially reported late 2026 or early 2027.

- Establishment of manufacturing batches per Lonza staging schedule facilitating transition from Phase 1 into confirmatory trials.

- Progress toward companion diagnostic validation enabling regulatory submission support documents enhancing label claims.

- Continued capital raising efforts possibly under existing ATM facility providing flexibility but contingent on investor appetite amidst equity dilution concerns. Monitoring these landmarks will be critical gauges of execution cadence relative to stated growth plans [S2][S3][S6].

Financial Snapshot: Healthy Liquidity Supports Near-Term Development

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $4mm | |

| 2026-03-31 | ||

| Current assets | $4mm | |

| 2026-03-31 | ||

| Current liabilities | $431000 | |

| 2026-03-31 | ||

| Current ratio | 10.31x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

As per the latest available data ending March 31, 2026 ([F1]), Kairos maintained $3.675 million cash & equivalents against total current assets of $4.443 million versus current liabilities tightly controlled at $0.431 million showing operational discipline reflected in a very strong current ratio of approximately 10.31x supporting short-term liquidity needs despite continued net loss generation documented at ($5.447) million year-end FY2025.

While this liquidity base underpins ongoing R&D spending including clinical trials progression post-acquisition commitments (notably $15 million NDA milestone deferred beyond immediate horizon), sustained access to capital markets remains indispensable given absence of product revenues currently impeding self-sustaining free cash flows [F1][S2].

| Metric | Amount (USD) | Date |

| --- | --- | --- | | Cash & Equivalents | 3,675,000 | 2026-03-31 | | Current Assets | 4,443,000 | 2026-03-31 | | Current Liabilities | 431,000 | 2026-03-31 | | Current Ratio | 10.31 | 2026-03-31 |

This analysis is based solely on publicly available filings as of May 2026 without offering investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments