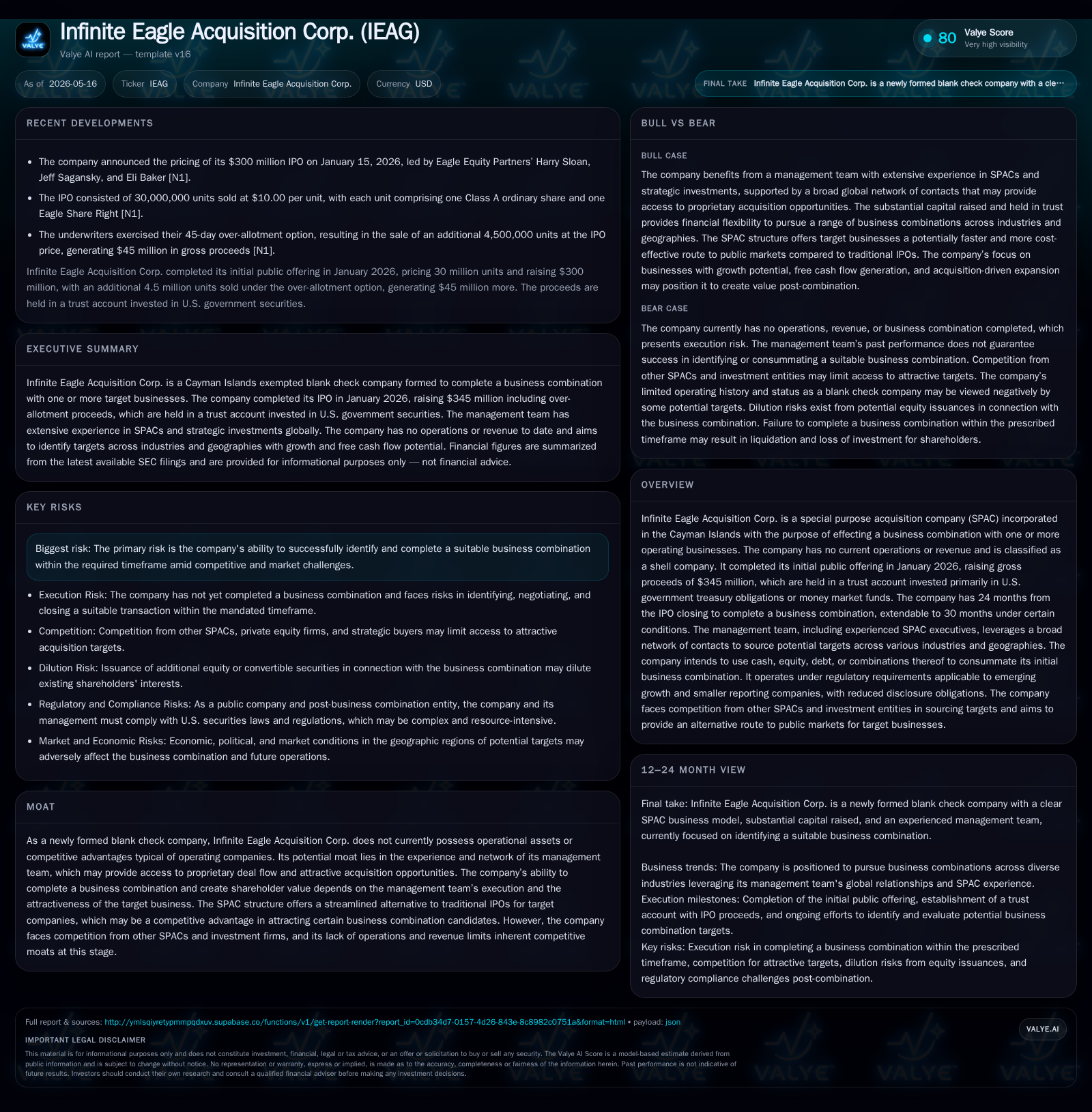

Infinite Eagle Acquisition: Assessing Momentum in the Search for a Breakout Business Combination

A new Cayman Islands SPAC with substantial capital and a veteran management team works against time constraints and market pressures to secure its initial target.

Infinite Eagle Acquisition Corp. remains a shell company as of its latest 10-Q filing, holding approximately $55 million in cash equivalents primarily invested in U.S. Treasury securities. Having completed its IPO early in 2026 and separated its units to enable independent trading of shares and rights, the SPAC now operates under a constrained timeline of up to 30 months to close an initial business combination. Its value creation potential hinges entirely on the management team's ability to leverage their extensive network to identify attractive acquisition targets in a competitive SPAC environment where redemption provisions and shareholder voting dynamics pose structural risks.

Latest Operating Update Highlights

Infinite Eagle Acquisition Corp.'s latest Form 10-Q filed May 15, 2026 [S2] reinforces its status as a blank check company: no revenues or active operations exist. The company holds $55.3 million in cash & equivalents at quarter-end March 31, 2026 [F1], primarily invested within a trust account managed through highly liquid U.S. government treasury securities and money market funds per SEC filings [S1,S15]. This trust account contains gross IPO proceeds of $345 million raised earlier this year through the offering of units composed of Class A ordinary shares combined with Eagle Share Rights [S1,S17].

A noteworthy development disclosed in an earlier March 9, 2026 Form 8-K [S3] was the separation of these units into individually tradable components: Class A ordinary shares (trading under symbol IEAG) and Eagle Share Rights (IEAGR). This structural flexibility offers investors distinct trading options ahead of any proposed business combination but requires investors to take procedural steps to split units. No material risk factor changes were reported since the annual filing [S2]. The maintained current ratio of approximately 2.9 reflects ample liquidity vs. short-term liabilities as of March [F1], positioning Infinite Eagle financially to pursue acquisition activities.

Business Model and Revenue Generation Mechanism

Infinite Eagle operates as a Cayman Islands exempted blank check company formed solely to facilitate one or more mergers or acquisitions (business combinations) with private or public operating companies across any sector or geography [S1,S4]. It does not generate traditional operational revenues; instead, capital raised via the January 2026 IPO ($345 million gross including over-allotments and private placement shares) is held almost exclusively in trust until deployed [S1,S15,S17].

The company's primary economic model depends on effecting an initial business combination that results in shareholders owning interests in an operating entity. The structure provides target companies an expedited alternative route to public markets compared with conventional IPOs due to streamlined regulatory processes and flexible deal consideration mechanisms—including all-cash deals or stock swaps using Infinite Eagle’s equity [S1,S14]. Management's role extends beyond capital provision; it leverages extensive networks spanning private equity, investment banking, legal advisors, and global industries—providing sourcing advantages that are critical given the SPAC's no-operating-assets status [S1,S4].

Competitive Context within the SPAC Ecosystem

While Infinite Eagle benefits from management's experience and contacts potentially granting access to exclusive deal flow, it operates in one of the most saturated segments of financial markets: the SPAC arena. Thousands of similar vehicles compete for high-quality targets capable of delivering shareholder value. Moreover, many competitors possess greater financial firepower or dedicated sector expertise than Infinite Eagle’s relatively modest trust size [$345M gross], limiting opportunities for very large transactions [S14].

The presence of redemption rights enables public shareholders to cash out upon transaction proposals at roughly $10 per share plus interest from trust proceeds but simultaneously reduces available cash for transaction financing if redemptions are high—a meaningful competitive disadvantage when negotiating terms [S1,S14,S16]. Furthermore, founder shares controlled by management carry disproportionate voting influence over business combination approvals regardless of public shareholder dissent [S1], which adds governance nuance but draws scrutiny regarding minority investor protections.

Growth Catalysts and Acquisition Pipeline Dynamics

Infinite Eagle’s growth narrative centers strictly on successful consummation of one or more business combinations within the Completion Window—currently set at 24 months following IPO closing with potential extension to 30 months if an agreement is entered within the initial period [S15]. The pipeline strength depends heavily on management’s ability to identify targets demonstrating revenue growth characteristics, free cash flow generation potential, and expansion capabilities either organically or via acquisition—criteria outlined broadly but promising multi-dimensional growth drivers [S8].

Management aims to capitalize on global sourcing channels derived from prior strategic investment experience—a critical factor in penetrating competitive deal arenas where typical timing pressure compresses due diligence windows and limits bargaining leverage. Deal flexibility afforded by combining SPAC cash with debt financing or PIPE investments allows structuring tailored transactions appealing to seller needs while optimizing post-merger capital structure efficiency [S14,S15].

Market appetite for de-SPAC transactions remains volatile but potentially strong depending on macroeconomic factors; hence timely announcements around identified targets will materially impact investor perception. Each milestone—from definitive agreements through proxy solicitations—will be scrutinized closely as markers of momentum toward value realization.

Key Risks and Structural Constraints on Value Creation

Completion Deadline Pressure: The statutory Completion Window imposes strict limits that can result in liquidation if no acceptable business combination closes by month 24–30 post-IPO, risking investor capital return without premium gains [S1,S15].

Redemption Risk: Public shareholders' right to redeem shares may diminish available cash needed for acquisitions, forcing financing compromises or deal term dilution detrimental to remaining investors [S1,S14].

Governance Complexity: Founder shares grant management outsized influence on votes approving transactions regardless of broader shareholder sentiment, potentially exacerbating conflicts between public holders and founders [S1].

Operational Absence: Without ongoing operations or revenue streams until a transaction consummates, valuation depends entirely on acquired assets’ quality—posing intrinsic valuation risk and limited transparency pre-combination [S1].

Competitive Landscape: Intense competition for deals from other SPACs and established private equity firms challenges management's capacity to secure attractive targets under favorable terms amid limited timeframes and capital constraints.

Regulatory Compliance: Increasing regulatory scrutiny under evolving SEC rules governing SPAC disclosures could increase costs and transactional complexity during the business combination process[S28,S24].

Upcoming Milestones and Critical Investor Watchpoints

Investors should monitor several key developments over the next quarters:

- Business Combination Announcement: Signals that Infinite Eagle has identified a target meeting its investment criteria within allowed timeframes.

- Extension Filings: Requests for extensions beyond original deadlines would indicate pursuit complexities but also intentions to remain active.

- Redemption Procedures Communication: Clear guidelines from management about redemption mechanics post-unit separation will guide investor decision-making.

- Proxy Filing Dates and Vote Scheduling: Timing of shareholder meetings reflects deal progress and consensus-building efforts.

- Capital Structure Updates: Any filings related to PIPE deals or debt structures aimed at supplementing trust proceeds will materially influence outcome feasibility.

- Investor Sentiment Post-Unit Separation: Market price action following unit splits into ordinary shares and rights may indicate confidence levels regarding potential deals.

Condensed Financial Snapshot

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $55276 | |

| 2026-03-31 | ||

| Current assets | $245424 | |

| 2026-03-31 | ||

| Current liabilities | $84765 | |

| 2026-03-31 | ||

| Current ratio | 2.9x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

As highlighted from company facts dated March 31, 2026 [F1]:

| Metric | Value (USD '000) | Date |

|---|---|---|

| Cash & Equivalents | 55,276 | |

| 2026-03-31 | ||

| Current Assets | 245,424 | |

| 2026-03-31 | ||

| Current Liabilities | 84,765 | |

| 2026-03-31 | ||

| Current Ratio | 2.9 | |

| 2026-03-31 |

This analysis presents Infinite Eagle Acquisition Corp.'s current standing as an early-stage SPAC navigating a highly competitive identification-and-close cycle under pronounced temporal constraints. Its prospects depend largely on management’s proven sourcing acumen amidst structural market challenges including redemption-related capital limitations. While financial liquidity supports transaction readiness, investors must weigh inherent uncertainties linked to deal sourcing success within defined windows alongside governance nuances.

Disclaimer: This report is intended for informational purposes only and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments