Vertical Data Inc. Advances AI Compute Distribution with Strategic OEM Partnerships

Latest quarterly disclosures highlight Vertical Data’s execution challenges and strategic opportunities in AI-focused high-performance computing distribution.

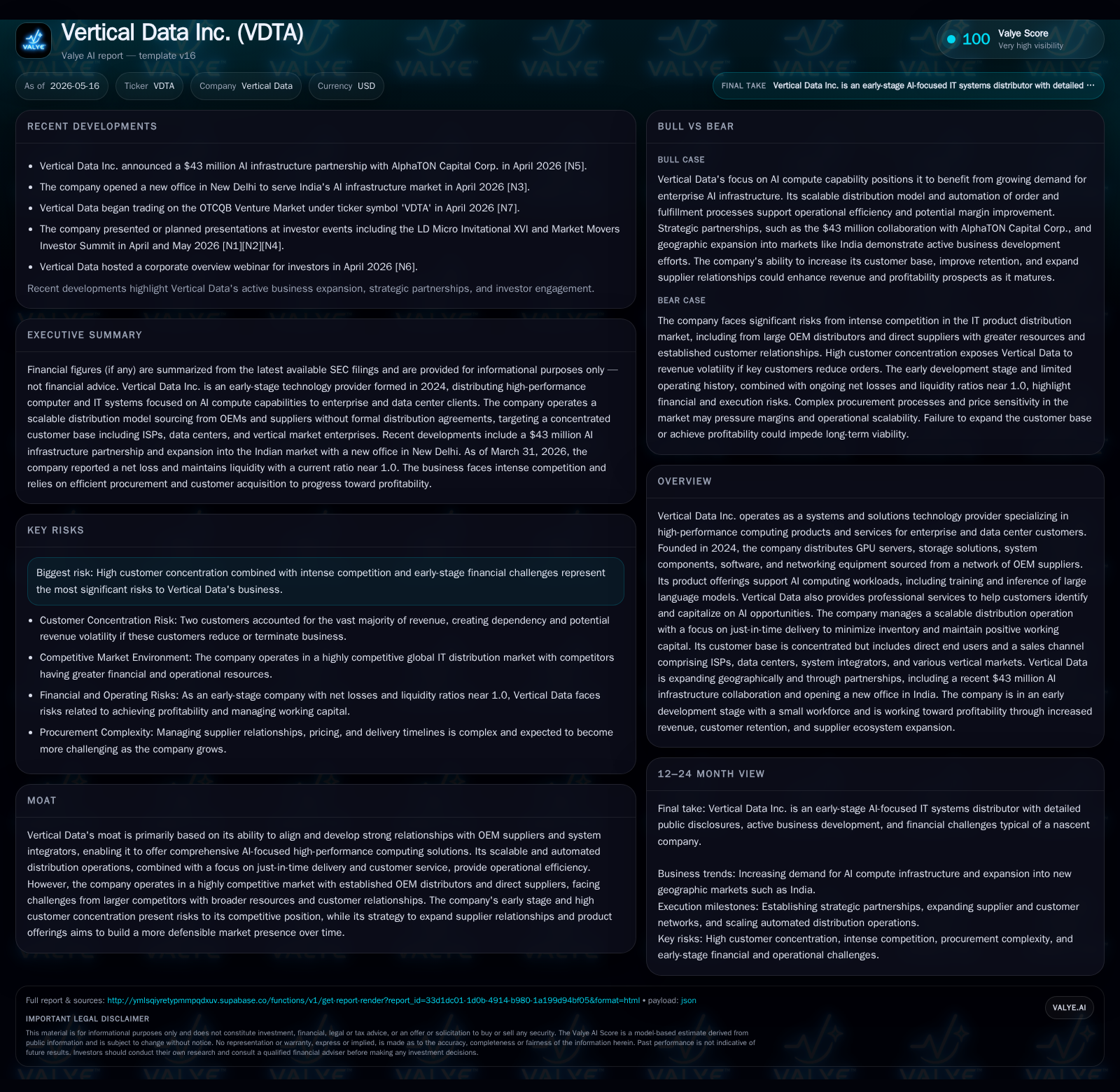

Vertical Data Inc.’s May 2026 quarterly filing reconfirms its high customer concentration and operational scale-up hurdles, amid a competitive AI hardware distribution landscape. The company’s scalable, just-in-time model centers on GPU servers and AI compute infrastructure sourced from OEM suppliers, targeting enterprise and data center customers. Growth depends on expanding supplier networks, broadening its customer base beyond two highly concentrated accounts, and leveraging emerging proprietary product development alongside professional services. Risks remain significant around competition, customer dependency, and early-stage financial stability.

Latest Quarterly Operating Update

In Vertical Data Inc.'s latest 10-Q filing dated May 15, 2026, the company's operating profile remains consistent with prior disclosures but reveals ongoing challenges that are critical to near-term performance. Revenue concentration continues to be heavily skewed toward two customers who historically account for over 90% of total revenue, underscoring heightened counterparty risk and dependence on limited buyer relationships [S2]. Meanwhile, the balance sheet snapshot as of March 31, 2026 indicates a current ratio of approximately 0.98 ([F1]), which suggests a tight liquidity position without substantial cushion—typical for an early-stage distributor managing just-in-time inventory cycles.

No material shifts in supply chain or customer diversification were evident in the quarter; however, the company reiterates its strategy to expand supplier relationships and elevate order volumes as paths to scale. Cash & equivalents stood at nearly $3.5 million as of quarter end ([F1]), providing some runway but emphasizing the necessity for growing revenue streams swiftly. Risk factors disclosed remain unchanged since the S-1/A effective July 2025, highlighting persistent risks related to competition, customer concentration, and financial stability within this nascent stage operation [S2]. This update reinforces that while Vertical Data is executing its business plan incrementally, it faces classic startup drawbacks in capital intensity linked to inventory management and concentrated sales dependencies.

Business Model and Product Portfolio

Vertical Data operates as a systems and solutions technology provider whose core business model revolves around distributing high-performance computing IT products tailored for AI workloads—chiefly GPU servers utilized in training large language models (LLMs) and their inference applications [S1], [S6]. The company sources these products through a network of OEM suppliers rather than relying on proprietary manufacturing; these encompass servers (often bare metal or fully pre-configured), storage arrays, system components, networking devices, software licenses, and related peripherals essential for state-of-the-art AI data center deployments.

Revenue derives directly from sales to enterprise customers and data centers—either directly or via a sales channel comprising ISPs, system integrators, and vertical market enterprises such as finance or government institutions. Pricing is largely dictated by prevailing market dynamics characterized by declining unit prices due to rapid innovation from chipmakers like Nvidia or AMD alongside intense vendor competition. To mitigate inventory risk inherent in the sector’s short product life cycles (~months given swift generational upgrades), Vertical Data emphasizes just-in-time delivery models aligned with order requisitions [S1], [S10].

Operationally distinctive is Vertical Data’s automation-driven IT system stack enabling an integrated quoting-to-shipment workflow that enhances response time efficiency — providing real-time visibility into order and customer status during all phases of procurement and fulfillment. This not only bolsters customer experience but supports ongoing scalability with limited incremental fixed cost increases as supplier relationships grow broader [S7].

Complementing hardware sales is burgeoning professional services focused on consulting clients to identify tangible AI infrastructure opportunities—a value-add that aims to deepen customer engagement beyond transactional equipment purchases. Concomitantly, Vertical Data invests in R&D intended to design proprietary branded hardware/software solutions targeting specific market niches. This roadmap represents a potential margin enhancement lever compared to lower-margin third-party resale products typical in the distribution arena [S11], [S12].

Industry Structure and Competitive Positioning

The high-performance computing system distribution sector operates under considerable structural complexity: rapidly evolving product lifecycles tied closely with semiconductor innovation cadence fuel continual upgrade demand yet simultaneously compress margins through price erosion. Distribution intermediaries like Vertical Data must compete not only against other resellers but also direct sales channels of major OEM manufacturers (e.g., Dell Technologies, Hewlett Packard Enterprise) who wield stronger brand recognition and extensive global reach. Furthermore, competition includes regional distributors who leverage scale or specialized services to lock-in clients.

Vertical Data’s competitive moat primarily lies in its agile supplier alignment without exclusivity agreements—a double-edged sword offering flexibility but limiting guaranteed volume discounts—and its integrated distribution operations powered by automated IT workflows streamlining quoting through shipping processes. These features enable swift procurement decisions tied closely with shifting market demands for AI compute hardware bundles while minimizing cash flow strain due to reduced inventory holdings [S4], [S7].

Nonetheless, this agility contends with notable downside risks including minimal human resources (only one full-time employee supplemented by consultants), high-customer concentration thereby amplifying revenue volatility risk if any major client reduces orders swiftly or opts for alternative suppliers. Industry consolidation trends favor larger players with deeper pockets who can absorb margin pressures better while offering end-to-end solutions integrating hardware with bespoke software stacks—areas Vertical Data is gradually targeting but has yet to fully penetrate at scale.

Growth Drivers and Expansion Path

Key levers that could catalyze expansion at Vertical Data hinge on increasing its ecosystem breadth both horizontally among suppliers and vertically along client relationships:

Supplier Network Expansion: Growing OEM supplier count could augment product breadth enabling more customized configurations suited for varied AI workloads; this would improve pricing leverage vis-à-vis existing providers while enhancing SKU diversity appealing to broader segments across cloud providers to niche data centers [S11].

Customer Base Diversification: Easing dependence away from two dominant customers through targeted business development would reduce single-customer revenue vulnerability while supporting sustained volume growth needed for operating leverage improvements.

Geographical Reach: Recent establishment of a new regional office in New Delhi signals intent to capitalize on burgeoning Indian data center market investing heavily in local AI infrastructure deployments—a promising high-growth frontier supported by favorable policies encouraging digital infrastructure investments ([N2]).

Professional Services Upsell: Vertical Data’s consultative service offerings provide an opportunity to create sticky client relationships translating into recurring revenue streams that complement hardware sales; effectively moving upstream towards full-solution provider status enhances competitive differentiation beyond mere commodity distribution.

Proprietary Product Development: Strategic R&D investments aiming at internally branded hardware/software tailored for cost-performance optimization represent a medium-term path to gross margin enhancement versus sole reliance on third-party resale margins [N1], [S12].

AI Infrastructure Replacement Cycles: The fast-replacing nature of AI compute technology driven by chipmaker upgrade timelines creates predictable demand pulses which nimble distributors can exploit if supply responsiveness is adequate; reducing procurement lead times will be pivotal here.

Risks and Challenges to Monitor

Despite promising prospects, Vertical Data faces acute risks requiring careful stewardship:

Extreme Customer Concentration: Historical revenues dominated (>90%) by two customers presents existential risk should either reduce orders materially or defect due to competitive pressures or internal strategic shifts; diversification remains a top priority yet progress remains limited so far [S1], [S4].

Price-Based Competition: Hardware distribution is a commoditized segment subject to aggressive pricing tactics from entrenched OEM distributors alongside direct manufacturer pipelines; sustaining adequate gross margins necessitates effective supplier negotiation plus value-added services counteracting pure price wars.

Early-Stage Financial Stability: With a current ratio below 1 as of March 31, 2026 ([F1]), Vertical Data faces tight liquidity conditions coupled with ongoing investment in operational ramp-up and R&D efforts amid still negligible scale economies, leaving the company exposed during volatile economic downturns when IT budgets contract or replacements delay.

Limited Human Capital: Operating with just one full-time employee supplemented by consultants imposes capacity constraints impacting speed of execution across sales expansion, supplier management, service delivery, and technology development functions.

Macroeconomic & Industry Cyclicality: Broader business activity fluctuations combined with accelerated release cycles of top-tier AI chipsets produce irregular purchase patterns complicating demand forecasting essential for optimized inventory flow management.

These factors consistently figure among the stable risk disclosures reaffirmed since mid-2025 regulatory filings emphasizing their foundational importance when evaluating enterprise viability at this stage [S18].

Key Near-Term Milestones and What to Watch Next

Investors monitoring Vertical Data’s trajectory should track several critical operational milestones:

Progress toward formalizing expanded OEM supply agreements expected to bolster portfolio depth thus improving pricing terms beyond ad hoc sourcing currently practiced.

Evidence of meaningful sales pipeline diversification away from top two customers including contract wins or renewals within new verticals or geographies.

Metrics demonstrating reduced procurement lead times such as improved order fill rates indicating enhanced supply chain responsiveness.

Updates regarding deployment timelines for proprietary hardware/software products which could materially alter margin profiles once commercialized.

Public investor engagement events including detailed presentations at the LD Micro Invitational XVI scheduled shortly after the latest quarter offering fresh disclosures on strategy execution plans ([N3], [N4]).

Additionally noteworthy is the $43 million partnership announced earlier this year with AlphaTON Capital Corp intended as dedicated financing support specifically targeting expansion of AI infrastructure initiatives—a bolstering factor that may alleviate funding constraints if effectively deployed ([N1]). Geographic footprint expansion remains highlighted by recent entry into India's rapidly growing AI infrastructure market through an office in New Delhi providing localized support essential for capturing regional growth opportunities ([N2]). These developments collectively portray Vertical Data at an inflection point oscillating between typical startup hurdles versus potential scalable growth anchored in fertile AI demand conditions.

This analysis focuses strictly on publicly disclosed information up through May 2026 filings plus contemporaneous news announcements without making forecasts or investment recommendations. It reflects acting as an informed industry observer assessing risks/opportunities inherent in Vertical Data's evolving business model within the competitive high-performance computing distribution sector specializing in AI workloads.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments