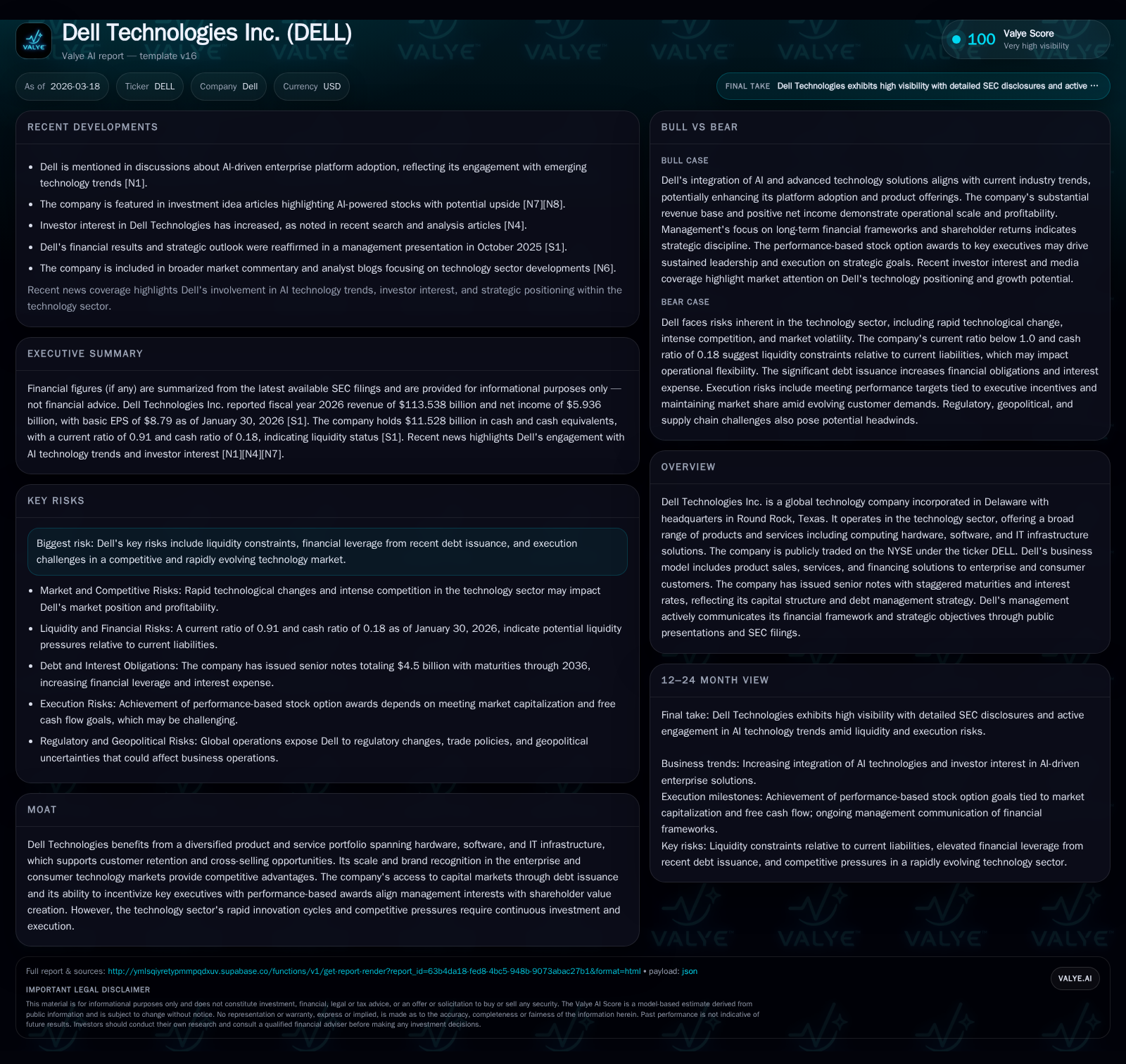

How Dell Technologies Is Balancing Debt and Growth in a Competitive Tech Market

Dell Technologies achieved extraordinary revenue growth in FY2026 while managing a complex multi-tranche debt structure that shapes its financial flexibility.

Dell Technologies posted an exceptional 374% revenue increase for fiscal year 2026, largely driven by strategic shifts in its diversified product and service portfolio. This growth surge is occurring alongside the company’s issuance of significant senior notes with maturities extending to 2036, demanding careful leverage management through cash flow generation and capital allocation. While operating cash flow expanded robustly and free cash flow remains strong, challenges persist in the form of negative equity and execution risks amid rapid industry innovation and intense competition. Monitoring upcoming debt maturities, AI adoption trends, and operational metrics will be critical to assessing Dell’s sustainable value creation going forward.

Financial Growth Trajectory: A Sharp Upswing in Revenue and Profitability

Dell Technologies demonstrated a remarkable financial surge in FY2026, reporting revenues of $113.5 billion—an increase of approximately +374% over the prior year’s $23.9 billion [F1]. This outsized jump reflects transformational business events or reclassifications within that year but confirms considerable scale expansion. Operating income more than tripled to $8.15 billion (+277%) while net income climbed sharply to $5.94 billion (+287%), underscoring effective leverage of operational efficiencies during rapid growth [F1]. Operating cash flow also surged to $11.2 billion (+147%), signaling strong cash conversion alongside rising margins.

Historical performance (annual)

| FY | Rev ($bn) | Net ($bn) | CFO ($bn) | OpInc ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2026 | 113.5 | 5.9 | 11.2 | 8.1 | +374.4% | +287.2% |

| 2025 | 23.9 | 1.5 | 4.5 | 2.2 | -72.9% | -52.3% |

| 2024 | 88.4 | 3.2 | 8.7 | 5.2 | -13.6% | +31.5% |

| 2023 | 102.3 | 2.4 | 3.6 | 5.8 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($bn) | FCF ($bn) | ROE% |

|---|---|---|---|

| 2026 | 6.0 | 8.6 | -240.3 |

| 2025 | 2.6 | 1.9 | -103.4 |

| 2024 | 2.1 | 5.9 | -133.6 |

| 2023 | 3.3 | 0.6 | -78.2 |

Source: SEC companyfacts cache [F1].

Table: Dell Technologies Annual Financial Summary Highlights (FY2023-FY2026) [F1]

The extraordinary scale change between FY2025 and FY2026 suggests transaction-driven growth or inclusion of new segments; nevertheless, sustained profitability improvements reflect operational strength.

Drivers Behind Dell’s Revenue Explosion: Product and Service Portfolio Shifts

Dell's resurgence is closely linked to its diversified portfolio encompassing computing hardware, software solutions, and integrated IT infrastructure services [S1],[S9]. The company benefits from a broad enterprise IT stack providing end-to-end lifecycle solutions—from data storage hardware to software-defined infrastructure—and consumer products with deep market penetration.

Cross-selling advantages arise from Dell's ability to bundle hardware with proprietary software stacks plus managed services, enhancing customer retention across large enterprises increasingly reliant on hybrid cloud ecosystems.

In recent years, the company has emphasized expanding its IT service offerings aligned with digital transformation trends including AI-enabled data intelligence platforms [N1],[N2],[N3]. These complementary solutions have heightened Dell’s relevance amid evolving workflows requiring integrated hardware-software deployments.

Capital Structure Complexity: Multi-Tranche Senior Notes and Leverage Considerations

Complementing the top-line surge is a sophisticated capital structure highlighted by issuance of $5.5 billion in senior unsecured notes on October 6, 2025 . This included:

- $750 million at 4.15% maturing February 2029,

- $1.25 billion at 4.50% due February 2031,

- $1.25 billion at 4.75% due October 2032,

- $1.25 billion at 5.10% due February 2036.

These notes are joint-and-several guaranteed by Dell Technologies Inc., EMC Corporation, and related subsidiaries yet structurally subordinated to any non-guarantor subsidiaries' indebtedness [S10]. The indentures incorporate standard covenants limiting liens on assets securing other indebtedness, restrictions on mergers/dispositions without consent, and customary default triggers consistent with investment-grade profiles.

The staggered maturities permit measured refinancing risk management but oblige Dell to optimize liquidity given the negative equity position and existing leverage layers evidenced on the balance sheet [F1],[S7]. Redeemable features include make-whole premiums if called before specified dates ranging from one month up to three months prior to maturity.

Cash Flow Strength and Free Cash Flow Generation Supporting Strategic Flexibility

Underlying Dell's capacity to service debt is robust cash flow generation; operating cash flow nearly doubled from FY2025's $4.52 billion to over $11 billion in FY2026 [F1]. Meanwhile, capital expenditures remained essentially flat around $2.63 billion (-0.7% YoY), reflecting disciplined investment amidst growth.

This results in strong free cash flow approximating $8.55 billion (CFO minus capex) that supports Dell’s strategic flexibility for deleveraging or shareholder returns [F1]. Maintaining CFO significantly above capex enables funding of large-scale share repurchases without liquidity strain.

Managing Returns: Equity Position, ROE, Dividends, and Share Repurchase Activity

Dell's equity balance remains negative at approximately -$2.47 billion as of January 30, 2026 [F1], partly reflecting historical financing structures including leveraged buyouts and accounting treatment impacts inherent in technology conglomerates.

This negative book equity complicates traditional ROE calculation reliability; naïve division yields an ostensibly aberrant -240% ROE figure when dividing net income by book equity [F1]. Such distortion necessitates cautious interpretation focusing instead on cash flow return metrics.

Notably, no dividends have been paid since fiscal years predating this analysis; instead, capital return strategy centers on share repurchases with $6 billion executed during FY2026 alone—more than double the prior year level [F1],[S19]. This reflects management preference for buybacks over dividends given capital structure optimization priorities.

Future Outlook and Milestones: Key Financial and Operational Metrics for Monitoring

Market attention focuses on quarterly earnings cadence throughout calendar year 2026 as transparency into ongoing AI integration initiatives emerges [N12],[N13],[N14]. Debt maturities commencing in early 2029 warrant monitoring given potential refinancing environments.

Client adoption trends of AI-enabled IT infrastructure—an area where Dell leverages its integrated stack advantage—may provide leading indicators for sustaining top-line momentum [N1],[N2],[N3]. Free cash flow targets relative to capex will signify capacity for continued shareholder value enhancement via buybacks or optional deleveraging.

Sector Nuances: Cross-Selling Advantages in IT Infrastructure Amid Rapid Innovation

The synergy among Dell’s hardware offerings, software platforms, and tailored IT services fosters ecosystem lock-in across enterprise clients navigating cloud migration challenges [S9]. This integrated solutions approach reduces switching costs while enabling lifecycle management visibility via centralized tools bolstering customer stickiness.

Such moat dynamics are critical within a sector characterized by relentless innovation waves where standalone product commoditization threatens margins absent ecosystem breadth or bundle complexity advantages common among peer conglomerates.

This analysis is based solely on publicly available information as of March 18, 2026, including SEC filings ([S#]), company facts ([F1]), and relevant news sources ([N#]). It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments