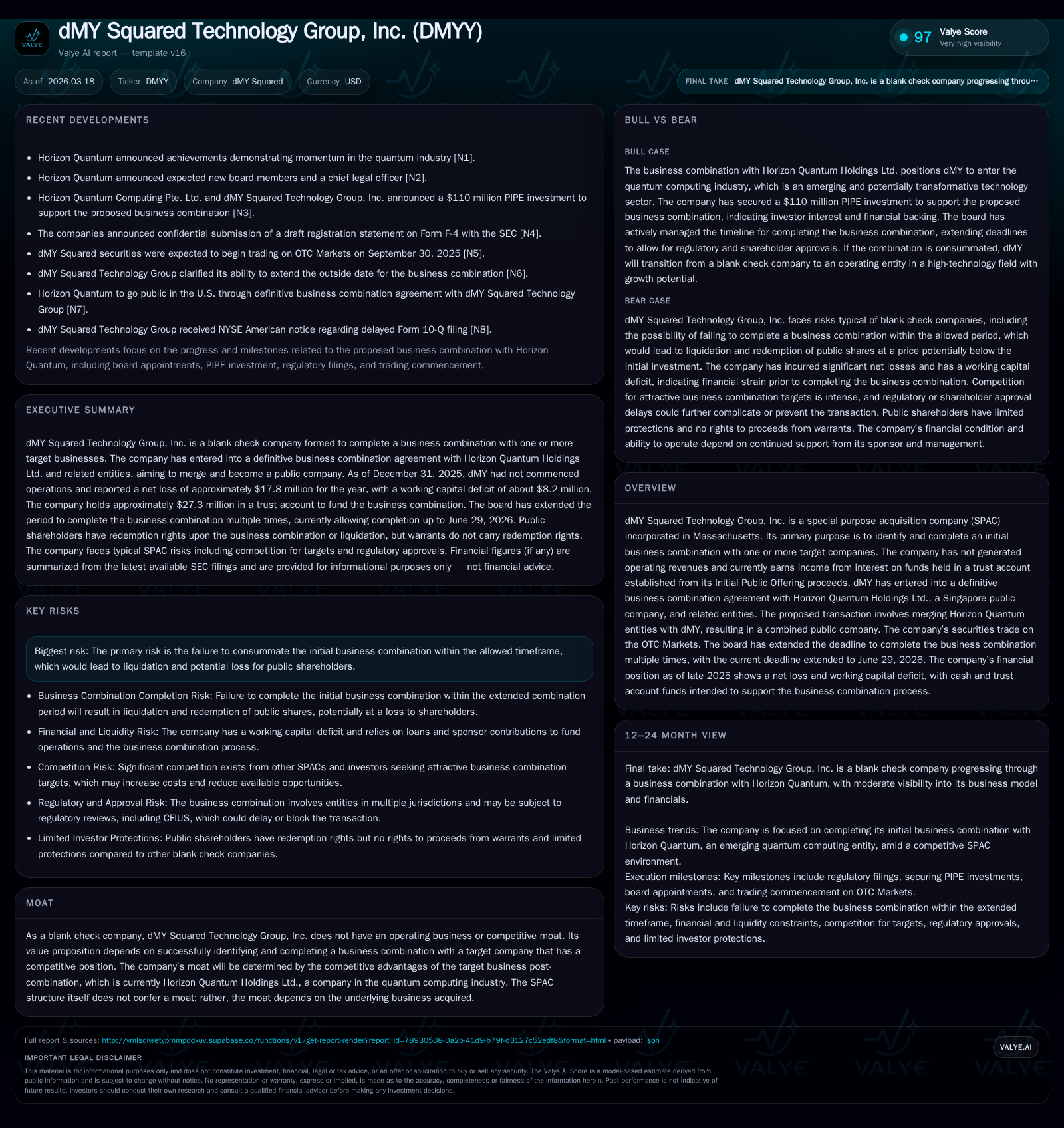

dMY Squared Technology Group: Evaluating Its Quest in Quantum Tech via Horizon Quantum Merger

dMY Squared’s SPAC transformation underscores the challenges and opportunities in merging with Horizon Quantum amid tight deadlines and liquidity pressures.

As a special purpose acquisition company, dMY Squared Technology Group has yet to generate operating revenues, relying on trust account interest income while incurring rising losses primarily due to merger expenses. The pending business combination with Horizon Quantum Holdings offers a strategic pivot into the quantum computing sector but carries substantial execution risks exacerbated by liquidity constraints and multiple deadline extensions. Financial indicators reveal worsening operating losses and a precariously low current ratio, underpinning the critical nature of forthcoming milestones for the SPAC’s viability.

From IPO Inception to Merger Milestones: dMY’s Growth and Financial Footprint

dMY Squared Technology Group was formed in February 2022 as a blank check company incorporated in Massachusetts. Its purpose is to identify and complete an initial business combination with one or more targets. Since inception through December 31, 2025, dMY has not generated operating revenues; instead, it earns non-operating income from interest on funds held in a trust account established from IPO proceeds [S1]. The Initial Public Offering closed in October 2022, generating net proceeds initially placed in this trust.

Operating losses have escalated significantly as the company has progressed toward consummating its business combination. For FY2025, operating income was negative $4.46 million versus negative $1.14 million in FY2024 — indicating rising expense levels largely related to merger activities including due diligence and administrative costs [F1][S1]. Net loss expanded sharply to $17.8 million in FY2025 compared with $819 thousand the prior year. This jump stems notably from a $14.3 million loss linked to fair value changes of derivative warrant liabilities coupled with increased general administrative and merger expenses [S1].

This expansion of spending reflects the typical SPAC financial footprint: limited operational activity offset by escalating public company compliance costs, pursuit of target diligence, legal advisory fees, and transaction-related outlays.

Historical performance (annual)

| FY | Net ($mm) | CFO ($) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -18 | -352146 | -4 | -2075.1% |

| 2024 | -1 | -1395823 | -1 | -135.7% |

| 2023 | 2 | -600342 | -2 | +196.2% |

| 2022 | -2 | -1067619 | -1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | ROE% |

|---|---|---|

| 2025 | 66.1 | |

| 2024 | 0 | 12.0 |

| 2023 | 40 | -45.2 |

| 2022 | 46.1 |

Source: SEC companyfacts cache [F1].

Table: Annual income loss trends highlight spiking net losses especially in FY2025 following increased non-cash derivative losses [F1].

SPAC Structural Dynamics and Critical Deadlines: Navigating Extension and Redemption Risks

dMY started with an initial business combination completion deadline set at January 4, 2024 – fifteen months post-IPO. Following an extension approved by shareholders on January 2, 2024 (First Extension), this deadline shifted marginally to January 29, 2024 but was followed by provisions allowing up to twenty-three incremental monthly extensions subject to Sponsor contributions totaling approximately $1.19 million delivered via a convertible note mechanism [S1]. Subsequently approved on December 15, 2025 (Second Extension), shareholders permitted extending deadlines up to June 29, 2026 without further Sponsor contributions required for these extensions [S3][S1].

Redemptions occurred during these extension votes: for example on January 4th of 2024 approximately $42 million worth of Public Shares were redeemed corresponding to almost four million shares [S1]. More recent share redemptions were proportionally smaller but demonstrate investor caution towards protracted merger timelines.

Sponsor fees include monthly payments of $10k for administrative services; these fees are expensed until either business combination completion or liquidation [S27]. The convertible note advanced by CEO/Chairman Harry You underpins incremental funding tied directly to these monthly extension decisions [S7][S12]. Failure to complete within stipulated periods triggers mandatory liquidation at approximately $10.15 per share redemption from Trust Account assets [S1]. This mechanism positions dMY’s fate tightly around successful deal closure against regulatory and market timing pressures.

Horizon Quantum: Catalyst for Future Growth or Conditional Bet?

dMY's current transformative event hinges on completing its business combination agreement with Horizon Quantum Holdings Ltd., a Singapore-based firm active in quantum computing – an emergent technology poised for disruptive applications across cryptography and complex material simulation domains [N1]. Recent Nasdaq press releases dated March 2026 noted Horizon's industrial achievements within quantum development cycles alongside appointments of new board members strengthening governance infrastructure [N2].

While these developments provide rationale for investor optimism about technological prospects post-merger, dMY itself acknowledges that its competitive moat will derive solely from Horizon Quantum's post-combination performance rather than any standalone advantage intrinsic to the SPAC structure.

Success depends on integration execution but also external factors such as regulatory approvals including possible CFIUS review given cross-border incorporation complexities potentially affecting timing or feasibility of transaction completion [S21][S5].

Financial Health Snapshot: Operating Loss Trends, Cash Burn, and Balance Sheet Pressures

Liquidity data as of December 31st of 2025 reveal severe working capital deficits approximating $8.3 million against minimal current assets near $111 thousand — yielding a critically low current ratio around 0.01 which strongly signals strained short-term financial flexibility [F1]. This figure starkly highlights difficulties in covering immediate liabilities without accessing additional funding mechanisms like sponsor advances.

Cash balances outside Trust Account stand limited relative to outstanding payables including accrued expenses scaled at over $4 million plus notes payable related party advances exceeding $3.5 million cumulatively [S17]. Key liabilities encompass deferred underwriting commissions (~$2.2 million) plus substantial derivative warrant liabilities valued near $15.7 million contributing significantly to consolidated balance sheet deficits reported at nearly negative $27 million equity position at fiscal year-end [F1][S4][S17].

Management explicitly flags going concern doubts contingent upon either timely business combination consummation or orderly liquidation taking place before or by March/June 2026 deadlines respectively [S7].

Capital Movements and Shareholder Considerations: Sponsor Fees, Convertible Notes, and Warrants

Beyond typical administrative service fees ($120k annually paid to Sponsor), dMY utilizes convertible promissory notes as tactical instruments enabling financing bridge for monthly extension contributions amounting cumulatively above $1.19 million drawn down progressively through early-to-mid-2025[S8][S12][S27].

Convertible notes lack interest expense but carry embedded conversion rights allowing holders—predominantly Sponsor-affiliates—to convert principal into warrants exercisable post-combination providing potential upside exposure mirroring Private Placement Warrants terms [S10][S26].

Warrants fair value undergo sizable quarterly remeasurement fluctuations leading to reported gains or losses affecting net income volatility; notably a marked increase from about $692k fair value at end-2024 ballooned to over $7.5 million by end-2025 manifesting substantial non-cash charges that complicate earnings quality assessments in absence of underlying revenue streams [S4][F1].

Watchpoints Ahead: Extensions, Business Combination Completion, and Market Sentiment

The newly extended deadline of June 29, 2026 represents a pivotal temporal risk point beyond which failure to consummate the Horizon transaction mandates orderly winding-up with associated public shareholder redemptions at close-to-IPO prices expected [S3]. Investor redemption patterns historically mirror deal confidence signals; thus monitoring call volumes around extension announcements remain essential.

Additionally governance reinforcements evidenced by appointing new board members and legal officers at Horizon may indicate preparedness escalation toward closing milestone but do not eliminate external risks like potential regulatory conditions or market volatility impacting valuation or deal willingness [N2].

Forward-looking analysis includes watching for disclosure updates regarding SEC filings indicating progress or impediments; management communications around alternative target considerations should transaction deadlock arise; trading patterns ahead of final extension expiration will serve as market sentiment barometer.

Final Thoughts: Interpreting dMY’s Path Amid Quantum Industry Potential and SPAC Market Realities

dMY Squared exemplifies the archetype SPAC trajectory marked by an unprofitable financial profile heavily dependent on external capital injections while pursuing complex transformational mergers within tight statutory timeframes. The company’s initial zero revenue baseline imposes notable leverage on successful tie-up execution.

Its impending combination with Horizon Quantum offers entrance into an advanced technology frontier promising theoretically significant long-term growth but inherently speculative nonetheless—this underscores why dMY holds no standalone moat until such synergy manifests post-close.

Financial health metrics raise caution flags around near-term liquidity stress despite sponsor support mechanisms leaving narrow operational runway sensitive to unforeseen delays or adverse investor reactions triggering extensive redemptions.

Ultimately for stakeholders tracking this entity—be it potential shareholders or corporate partners—ongoing attention must center around merger timeline adherence balanced against quantum industry validation progress measured both technologically (innovation milestones) and commercially (market contracts). Failure would precipitate liquidation imposing downside capital implications conforming with typical SPAC risk frameworks outlined extensively within required disclosures.

This analysis synthesizes documented data without offering investment guidance. Readers are advised to consult primary filings for comprehensive details.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments