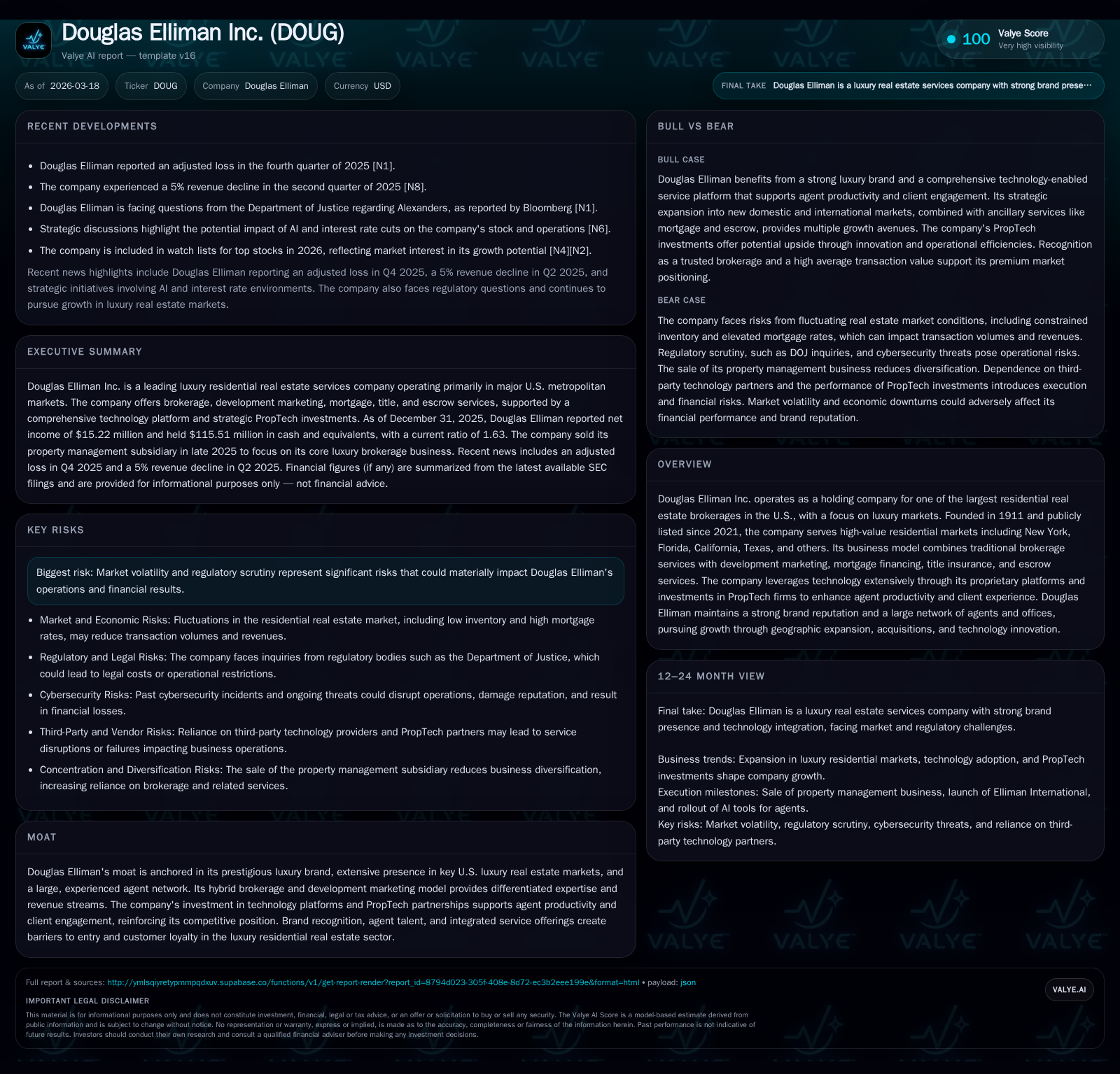

Douglas Elliman's Earnings Rebound Tests Resilience in Luxury Real Estate

Douglas Elliman reversed multi-year losses to post positive operating income and net profit in fiscal 2025, amid a challenging luxury real estate market with strategic technology investments and regulatory risks shaping its future.

Douglas Elliman Inc., one of the largest U.S. luxury residential brokerages, demonstrated a significant financial turnaround in fiscal 2025 after several years of operating losses. Despite a sharp 17.1% revenue decline from 2024 to 2025, the company posted $45.5 million in operating income and $15.2 million in net income, marking a clear rebound driven by operational efficiencies amid subdued transaction volumes. Concentrated exposure to high-priced luxury markets with elevated average sale prices (~$1.86 million) provides both stability and sensitivity to macroeconomic cycles, including interest rates and inventory scarcity. The company’s adoption of proprietary technology platforms and minority stakes in PropTech ventures underpin agent productivity and client engagement within a hybrid brokerage-development marketing model. However, ongoing antitrust litigation settlements and regulatory scrutiny around commissions pose meaningful risks. Capital allocation reflects a pause in dividends since 2024 and persistent negative free cash flow, highlighting the tradeoffs between growth investments and shareholder returns. The evolution of industry practices, regulatory outcomes, and geographic expansion efforts remain key milestones to watch going forward.

From Losses to Positive Operating Income: Tracing Douglas Elliman’s Financial Turnaround

Douglas Elliman’s fiscal results in 2025 represent a clear financial pivot from several years of operating deficits. After reporting operating losses of -$68.8 million in FY2024 and -$64.5 million in FY2023, the company posted positive operating income of $45.5 million in FY2025—a swing exceeding $110 million year-over-year [F1]. Net income followed suit with a recovery from -$76.3 million loss to a positive $15.2 million profit in the same period [F1]. This reversal occurred despite a significant revenue decline of 17.1%, from roughly $1.154 billion in FY2024 down to $955.6 million in FY2025 [F1], aligning with broader industry sales softness.

Operating cash flows remained negative but improved by 46.5%, registering $(13.9) million compared to $(26.0) million in FY2024 [F1]. Capital expenditures were pared back by nearly 40%, falling to $3.35 million on a more conservative investment posture amid uncertain market conditions [F1]. Overall equity contracted compared to prior years but stood at $184 million as of December 31, 2025—supporting an approximate return on equity of 8.3% based on reported net income—a modest but meaningful sign of profitability stabilization [F1].

The company’s improved margins highlight successful expense control measures alongside lower revenues possibly reflecting reduced transaction counts rather than commission rate erosion.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 15 | -14 | 45 | +119.9% | ||

| 2024 | -76 | -26 | -69 | -79.3% | ||

| 2023 | 956 | -43 | -30 | -64 | -17.1% | -656.9% |

| 2022 | 1153 | -6 | -15 | -5 | -14.8% |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 0 | -17 | 8.3 |

| 2024 | 0 | -31 | -47.1 |

| 2023 | 4 | -37 | -18.2 |

| 2022 | 16 | -23 | -2.1 |

Source: SEC companyfacts cache [F1].

This table encapsulates critical financial trends revealing how Douglas Elliman weathered extended market challenges before returning to profitability.

Luxury Market Dynamics and Geographic Footprint: Key Growth Drivers and Headwinds

Douglas Elliman uniquely concentrates on prime U.S. luxury markets characterized by high entry barriers and dense population centers including Greater New York City metro (New York City proper through Connecticut and New Jersey suburbs), select Florida destinations such as Miami/Biscayne area where headquarters lie,[S23][S8] California coastal hubs,[S8] Texas urban cores,[S8] plus coverage extending toward Colorado and Massachusetts.

The company’s strategy leverages these international finance hubs supplying inventory at premium price points—reflected in its elevated average sales price of approximately $1.86 million during calendar year 2025—well beyond mainline industry peers’ median sale prices [S24]. This pricing power underpins commission revenue stability even when overall transaction volumes soften.

Nevertheless,the real estate landscape exhibits cyclical swings strongly influenced by broader macroeconomic variables including short- and long-term interest rates which govern mortgage affordability; consumer confidence levels; availability of credit; changes in taxation or government housing policies; inflation pressures; as well as inventory scarcity or abundance—all factors Douglas Elliman explicitly flags as material risk drivers[S1] . Falling transaction velocity alongside historically tight supply conditions persistently challenge revenue growth momentum.

Commission rate pressure also arises from competitive brokers discounting fees[S1], though Douglas Elliman’s brand cachet partially insulates it against aggressive commoditization thanks to its luxury positioning.[S12] Agent network density approximates roughly 5,800 agents spread over more than one hundred offices—favoring deep local expertise advantageous for sustaining referral streams.[S23]

Overall mix shifts toward new developments via its Development Marketing arm (DEDM)—a hybrid brokerage-new development marketing platform pairing seasoned professionals—offer avenues for incremental upside given long-term growth potential tied to project volume spikes.[S18][S24]

Technology and PropTech Investments Powering Agent Productivity

Douglas Elliman has embraced technology as a core pillar to uplift agent productivity and modernize client interactions[S9][S13]. Its proprietary MyDouglas portal offers agents a sophisticated cloud-based SaaS platform integrating CRM capabilities; marketing campaign automation; transaction management; AI-powered analytics; virtual tours; video creation tools; comparative market analysis; predictive analytics; digital ad campaigns; open house scheduling; plus streamlined commission processing via StudioPro – another platform launched recently.[S9][S13]

The hybrid brokerage model synergizes innovation with traditional strengths: tech-enabled agents benefit from integrated best-of-breed applications sourced externally while proprietary platforms retain agility for rapid enhancements across changing technologies.[S25] This approach keeps operations asset-light while minimizing vendor lock-in risks.

Its DOUG Ventures subsidiary invests strategically across emerging PropTech firms generating modest current returns but promising optionality value: holdings include Rechat (mobile lead-to-close workflow software customized for brokerages); Purlin Enterprises merged with Final Offer offering AI-powered negotiation marketplaces and end-to-end residential real estate software stack integration touching mortgage/title processes; Fyxify automating home repairs scheduling; Persefoni AI enabling carbon footprint measurement SaaS promoting ESG analytics; Guest House specializing in staged home presenting; Infinite Creator empowering DIY video content creation—all leveraged directly or indirectly through agreements benefiting Douglas Elliman agents.[S10][S11][S12]

These minority stakes totalled about $11.4 million at carrying value at end-2025 representing ~3% of the firm’s total assets ($444 million), underscoring measured exposure balanced against core brokerage revenues.[S11] While no material revenue contributions are recognized yet from these investments,[S10] gains from selective monetizations occurred: e.g., gains recorded on Bilt Technologies divestitures totaling approx $2.2 million over two years ending FY25.[S10]

This tech-first orientation augments agent recruitment & retention by equipping talent with competitive digital sales & service tools aligned with evolving client expectations throughout buying cycles.[S13][S25]

Legal Landscape and Antitrust Litigation: Implications for Brokerage Commissions

Notwithstanding operational advances,Douglas Elliman contends with heightened regulatory scrutiny emanating from legal challenges targeting residential real estate industry commission practices.[S4][S7] In particular, of great significance is the class-action litigation related to the National Association of Realtors’ MLS commission-sharing mandates found anticompetitive in the landmark federal jury decision in Oct 2023 involving multi-billion dollar damages awarded against NAR itself but not directly implicating Douglas Elliman[S4].

Subsequent similar claims were filed naming Douglas Elliman among other brokerages across multiple states concerning alleged anti-competitive conduct violating federal/state laws related to buyer-agent commissions.[S4][S7] In April 26 2024 settlement agreements resolved cases nationwide spanning similar claims leading Douglas Elliman to disburse cumulative escrow deposits exceeding $12 million through end-December 2025 with an additional contingent payment up to $5 million planned through Dec-31-27 subject to financial triggers.[S4][S7]

However, the settlement faces ongoing appellate challenges creating uncertainty whether this resolution will hold or further liabilities may arise via persistent litigation or regulatory reforms aimed at reshaping standard brokerage commissions models nationally.[S7] Potential operational disruptions or mandated concession adjustments could emerge if appeals succeed or if state/federal agencies enact further rules limiting commissions or requiring greater transparency/disclosure.[S16][S20]

Given commissions fuel a substantial portion of revenue streams derived from completed sales transactions,this looming legal/regulatory risk remains material.[S7][S20] The company's robust brand reputation may mitigate some reputational damage risk but cannot insulate entirely against protracted costly legal battles or evolving regulations.[S15]

Capital Allocation Snapshot: Cash Flows, Dividends, and Balancing Growth Priorities

Douglas Elliman's capital deployment reflects careful navigation between investment needs amidst cyclical market pressures versus shareholder return expectations.[F1][S6] Negative operating cash flows persisted at $(13.9)M for FY25 albeit improved versus $(26)M loss the prior year while capex expenditures moderated sharply demonstrating disciplined expenditure cuts essential during periods of slower transactional volume.[F1]

Dividend distributions ceased post-FY23 dividend payment totaling approximately $4.2M after elevated payouts of $16M+ in prior years indicating prudence driven by liquidity considerations alongside uncertain near-term revenue trajectories.[F1] Equity declined gradually over recent years reflective partly of accumulated earnings volatility offsetting historical goodwill/intangible assets balances though no impairments noted as per filings.[F1][S21]

The company maintains solid liquidity positions with current ratios exceeding approximately 1.6x driven by adequate cash balances ($115M) relative to current liabilities (~$98M).[F1][S19] Conservative balance sheet management provides some buffer against adverse market shifts or unforeseen contingencies including legal reserves related to pending matters.[S6][S19]

Future capital allocation decisions might trade off further technology investments versus reinstating dividends/buybacks subject to sustained operational recovery visibility together with regulatory clarity regarding brokerage business model transformations.[F1][S6]

What to Watch Next: Market Conditions, Regulatory Outcomes, and Strategic Milestones

Key indicators will crystallize Douglas Elliman's trajectory moving forward including shifts in nationwide real estate transaction velocities particularly within its luxury core markets where commission percentages have outsized impact on revenues.[N1][S3] Ongoing resolution of pending appeals against antitrust settlements could decisively alter commission structures thereby influencing operating margins substantially either through mandated rate reductions or altered customary practices.[S4][S7]

Expansion efforts remain focal points: newly formed "Market Growth" unit targets deepening presence within existing territories while the "New Markets" team pursues footholds internationally across France/Monaco/St Barth licensing arrangements as well as potentially complementary U.S regions leveraging brand strength as stated internally.[S13] The success of such initiatives hinges on continued ability to recruit top-performing agents despite intensifying competition amplified by tightened compensation frameworks linked partly to the industry's transformation under regulatory/legal pressure.[S29]

Ancillary services expansion such as mortgage financing through alliances (e.g., Associated Mortgage Bankers), title insurance offerings,and escrow contribute potential diversification benefits augmenting fee-based revenues less correlated with housing sales cycles.[S24] These complements align well with technology-driven distribution channels embedding differentiated client experiences enhancing loyalty yet execution risk persists given market headwinds.

In sum,Douglas Elliman stands at an inflection point balancing legacy luxury brokerage strengths bolstered by strategic tech innovation against evolving legal-regulatory environments that could reshape fundamental economics integral to its business model. Monitoring these developments constitutes prudent diligence for stakeholders assessing durability within an uncertain luxury residential real estate landscape.

This analysis synthesizes publicly filed financial statements along with contemporaneous disclosures without projecting speculative performance insights beyond documented evidentiary basis.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments