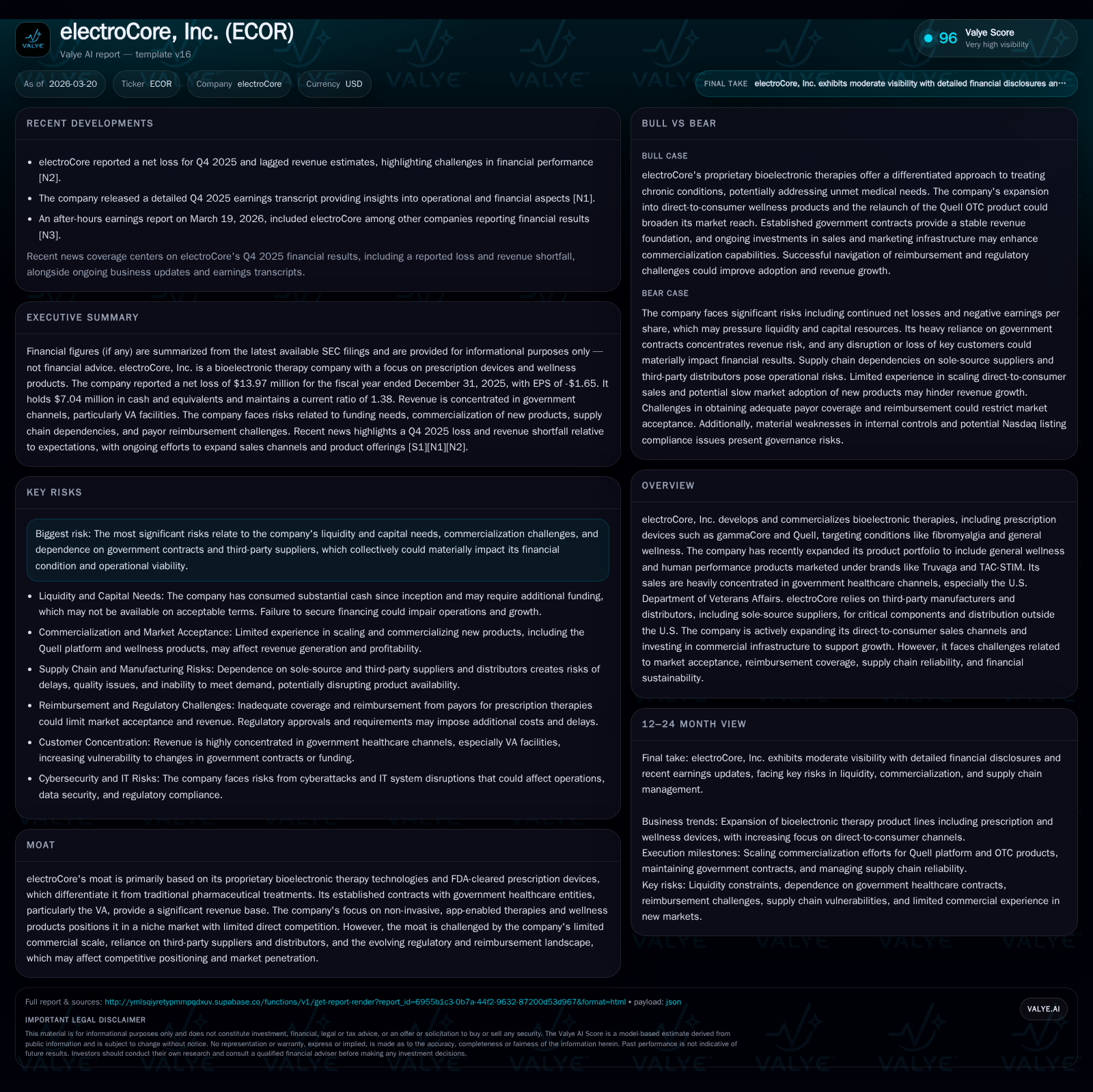

electroCore, Inc. Strives for Breakthrough Growth Amid Patent Battles and Financial Hurdles

electroCore confronts concentrated sales channels, supply chain dependencies, and costly patent litigation while pivoting toward wellness products to fuel growth.

electroCore, Inc. has transitioned from a focus on prescription bioelectronic therapies toward expanding its portfolio of general wellness and human performance products, aiming to diversify revenue beyond heavily concentrated government healthcare contracts. Despite ongoing operating losses and liquidity challenges, the company is investing in commercial infrastructure and direct-to-consumer sales channels to drive growth. A patent infringement lawsuit with UAB Pulsetto poses legal uncertainty and potential financial burden. Regulatory complexities and reimbursement hurdles further complicate market penetration, underscoring risks tied to supplier single sourcing and payor coverage. Monitoring developments in litigation outcomes, market acceptance of new wellness offerings, and execution of commercialization strategies will be critical in 2026.

Evolution of electroCore’s Revenue Streams: Prescription to Wellness

electroCore historically built its revenue base around prescription bioelectronic therapies such as the FDA-cleared gammaCore device targeting conditions like cluster headaches and migraines. Government healthcare contracts—most notably with the U.S. Department of Veterans Affairs (VA)—have been a cornerstone driver underpinning recurring sales volume [N1][S1]. Over recent years, however, the company has strategically broadened its product portfolio toward non-prescription general wellness and human performance offerings marketed under brand names like Truvaga and TAC-STIM [N1][S1].

This shift reflects an effort to diversify beyond highly concentrated government payor channels vulnerable to policy shifts or budget constraints. While no precise revenue splits are disclosed, management commentary underscores expanding direct-to-consumer initiatives as a way to tap growing market interest in non-invasive bioelectronic health products outside traditional prescription frameworks [N1].

Despite product diversification efforts, financial results through FY2025 exhibit persistent operating losses illustrating challenges in scaling commercial traction swiftly enough to offset cost structure [F1]. The company’s sustained investment in marketing, manufacturing, and distribution has not yet translated into positive operating leverage.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -14 | -8 | -13 | 66000 | -17.5% |

| 2024 | -12 | -7 | -12 | 206000 | +36.9% |

| 2023 | -19 | -15 | -19 | 206000 | +15.0% |

| 2022 | -22 | -17 | -23 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -8 | 817.2 |

| 2024 | -7 | -157.6 |

| 2023 | -15 | -253.1 |

| 2022 | -129.7 |

Source: SEC companyfacts cache [F1].

Table: electroCore Historical Financial Summary (FY2022-FY2025) [F1]

The data reveals some improvement in reducing operating losses from FY2022 levels yet continued negative net income points to ongoing unprofitability amid scaling challenges. Notably FY2025 equity turned negative reflecting accumulated deficits.

Revenue Concentration Risks and Supply Chain Dependencies

electroCore’s revenue concentration within government healthcare programs—especially via VA contracts—renders it susceptible to procurement mechanisms governed by federal budgeting cycles and policy changes [S12][N1]. These contracts provide predictable revenues but also expose the company to risks if government payors adjust coverage criteria or contracting terms.

Compounding concentration risk is the reliance on sole-source third-party manufacturers for critical device components plus distributors managing international markets outside the U.S [S1]. Supplier single sourcing elevates potential for supply disruptions that would impact product availability adversely during demand spikes or manufacturing interruptions.

Additionally, compliance with stringent federal contractor rules adds operational complexity that could affect contract renewal opportunities [S12]. Without diverse supplier relationships or alternative logistics arrangements currently in place at scale as noted by management [N1], unmitigated supply chain interruptions could materially impair sales execution.

Financial Performance Trends: Operating Losses and Liquidity Status

The company's annual operating income remained negative for four consecutive fiscal years through FY2025 [F1], only partially abating the deep losses seen earlier:

- Operating income improved from -$22.9M (FY22) to -$13.2M (FY25), signaling some cost control yet no path to profitability realized.

- Net income mirrored this trend remaining deeply negative at nearly -$14M for FY25.

- Operating cash flow continues constrained at roughly -$8.2M in FY25 after showing improvement from prior years.

- Annual capital expenditures have contracted sharply over recent years down to $66K in FY25 from $206K previously [F1].

- Importantly equity declined into negative territory (-$1.7M) in FY25 from positive $7.5M in prior years highlighting accumulated losses eroding net book value.

This evidence illustrates persistent cash burn that complicates achieving positive ROE or free cash flow generation in the near term [F1]. Minimal capital expenditure suggests prioritization of cost containment but underscores limited reinvestment capacity.

Patent Litigation Landscape and Its Strategic Implications

A key strategic challenge stems from intellectual property litigation initiated by UAB Pulsetto challenging electroCore’s core vagus nerve stimulation patents including the pivotal U.S. Patent No. 11,446,491 among others asserting infringement claims countered by electroCore’s own attacks [S1][S6].

This dispute enters an early discovery phase characterized by document exchanges and scheduled motions yet unresolved jurisdictional arguments remain pending before trial courts [S6]. The technology covered by these patents forms a critical part of electroCore’s proprietary competitive moat underpinning bioelectronic therapy differentiation.

While management expresses confidence that Pulsetto’s claims lack merit and commits to vigorous defense alongside counterclaims including trademark violations relating to gammaCore and Truvaga brands [S6], the proceeding imposes significant financial burden through legal fees plus potential reputational harm if adverse rulings limit enforcement ability or patent validity.

These uncertainties could delay expansion plans or weaken negotiating positions with payors by undermining intellectual property certainty central to product exclusivity.

Growth Drivers: Expanding Commercial Infrastructure and Direct-to-Consumer Sales

electroCore aims to amplify growth via investments building sales forces in key geographies including the U.S. and U.K., with a heightened focus on direct-to-consumer cash-pay channels aimed at non-prescription wellness consumers [N1][S1].

This strategy contemplates broader market reach beyond institutional buyers but demands escalated commercial spending contributing further short-term cash consumption [N1]. Such infrastructure expansion includes recruiting specialized sales personnel familiar with medical devices alongside digital marketing campaigns targeting health-conscious demographics receptive to non-invasive therapies.

Diversification into wellness verticals introduces new go-to-market challenges as brand recognition needs development while regulatory frameworks remain evolving [S4][S8]. Though promising as growth levers over medium term horizons this pivot increases capital deployment pressures amid ongoing operating deficits.

Regulatory and Reimbursement Challenges in Bioelectronic Therapies

electroCore operates within a complex regulatory environment encompassing FDA compliance for its prescription devices as well as adherence to federal trade commission advertising laws particularly relevant for its OTC Quell product line [S4][S5][S8].

The FDA's classification processes impose rigorous pre-market clearance obligations such as 510(k) submissions required for claims modifications or indication expansions constraining agility around labeling enhancements or new indications [S8][S26]. Moreover extrinsic factors like evolving reimbursement protocols affect coverage timing especially within government payors who exercise strict criteria impacting demand predictability [S9].

Transitioning prescription therapies into general wellness segments involves additional regulatory scrutiny including consumer protection oversight limiting promotional claims scope thereby increasing compliance costs and risks of enforcement actions as per FTC consent orders monitoring past advertising practices [S5][S23].

Furthermore any adverse FDA review outcomes or regulation changes can delay market entry or force modifications incurring operational disruptions.[S10] This multifaceted regulatory milieu demands careful navigation balancing clinical validation needs versus commercial speed-to-market targets.

Capital Allocation Review: Cash Flow Constraints and Shareholder Returns

electroCore’s capital allocation reflects prioritization of operational sustainment over shareholder distributions given negative operating results:

- No dividends or share repurchase programs have been undertaken reflecting limited discretionary cash flow availability [F1].

- Operating cash flow remains deeply negative at around -$8.2M annually exceeding nominal capital expenditures which totaled just $66K in FY2025 demonstrating minimal fixed asset reinvestment but ongoing burn through working capital needs.[F1]

- Negative equity position evidences cumulative deficit capitalization likely requiring future financing rounds if organic cash flows do not improve sufficiently.[F1]

- Management highlights dependency on external funding availability for ongoing commercialization investments including expanding sales infrastructure and R&D support of pipeline indications plus wellness product ventures.[S1]

- Litigation expenses related to patent disputes add incremental financial demands further straining liquidity.[S6]

Overall the company faces a challenging capital planning environment where growth investments risk intensifying near-term losses raising substantial financing execution risks absent improved revenue momentum.

2026 Watchlist: Milestones, Market Acceptance, and Litigation Outcomes

electroCore’s trajectory through 2026 hinges on several pivotal developments:

- Progress in payor coverage negotiations especially within government programs beyond VA contract renewals could unlock higher utilization across prescription devices mitigating concentration risks.[N1]

- Consumer adoption trends for wellness brands Truvaga and TAC-STIM must accelerate validating market expansion ambitions into direct-to-consumer models where brand awareness currently remains nascent.[N1]

- Litigation timelines remain fluid but resolution or favorable rulings on patent disputes would reduce legal uncertainties enabling more robust IP licensing or enforcement strategies.[S6]

- Execution against expanded commercial staffing plans across US & UK markets will be important performance indicators reflecting ability to scale sales productivity ahead of increased fixed costs.[N1]

- Quarterly earnings releases will provide updated visibility into operational burn rates alongside top-line growth dynamics informing sustainability perspectives.[N2]

Absent explicit quantitative guidance beyond qualitative goals announced during Q4 earnings call management narrative emphasizes cautious optimism balancing innovation aspirations against financial constraints amidst evolving competitive headwinds.[N1]

This analysis is based on publicly available SEC filings including the company's 10-K dated March 19th 2026 [S1], quarterly disclosures [S2], recent earnings transcripts [N1], news articles reporting on Q4 results [N2], as well as historical financial data extracted from companyfacts XBRL archives [F1]. It incorporates both documented facts about electroCore's strategic positioning combined with sector-informed contextual understanding of regulatory frameworks affecting bioelectronic therapy developers without extrapolating unverified forecasts or investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments