Yinfu Gold Corp.’s Liquidity Challenges and Regulatory Risks Cloud Growth Outlook

The company continues to face significant financial constraints and regulatory complexities that limit its ability to leverage assets and scale operations.

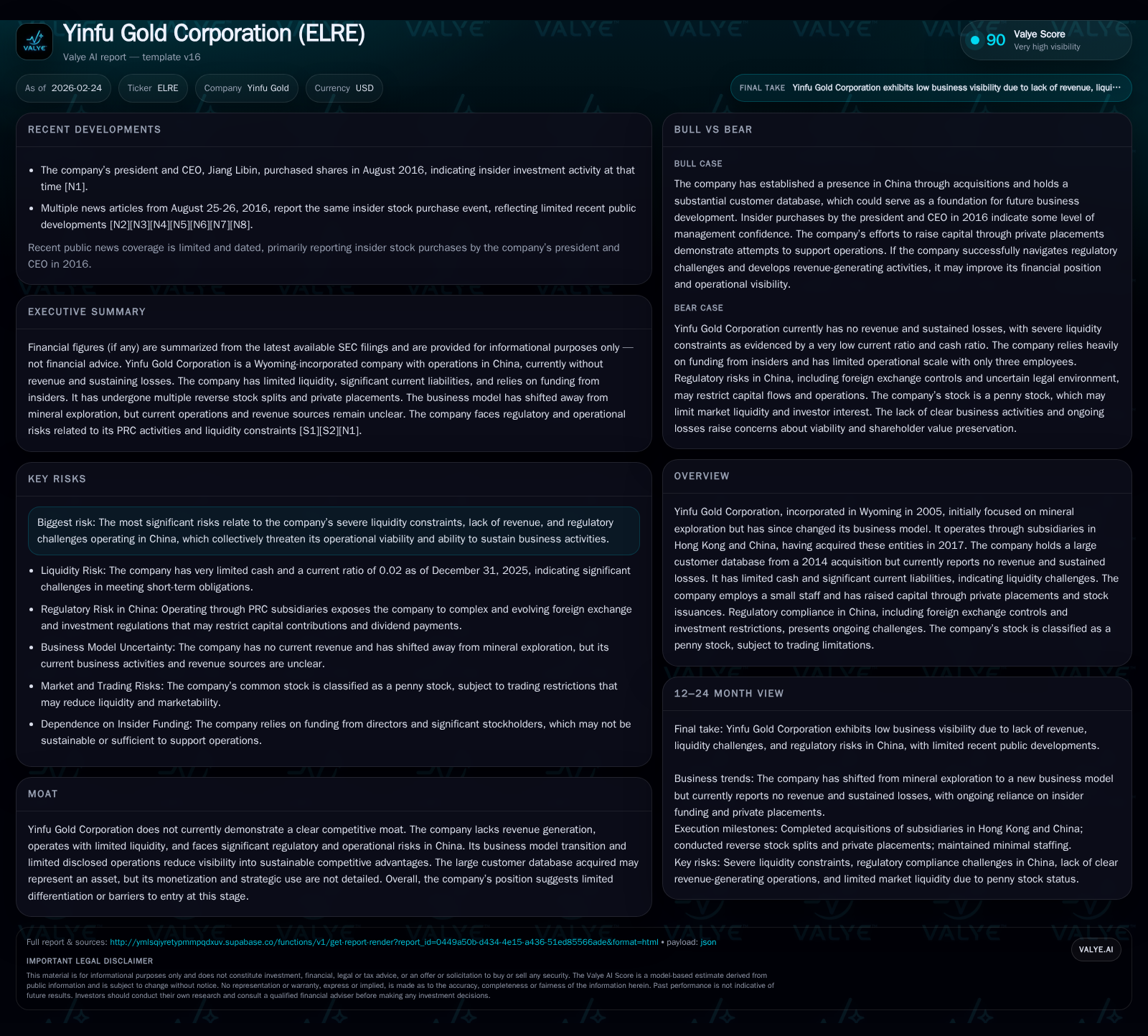

Yinfu Gold Corporation, initially a mineral exploration entity, has shifted its business focus but currently reports no revenue and ongoing losses. The company holds a large customer database acquired in 2014 yet has not realized meaningful monetization. Operating through subsidiaries in Hong Kong and China, Yinfu contends with substantial regulatory risks related to PRC foreign exchange controls and evolving cybersecurity laws. Despite modest capital raised via private placements, liquidity remains critically low with minimal cash reserves and heavy current liabilities. Key milestones remain unclear as the company has not disclosed definitive plans for asset monetization or operational expansion.

Company Overview and Historical Financials

Yinfu Gold Corporation (ELRE), incorporated in Wyoming in 2005 originally as Ace Lock & Security, Inc., transitioned away from mineral exploration by late 2010, adopting its current name to reflect a strategic pivot.[S1][S24] The company operates primarily through subsidiaries in Hong Kong and China acquired since 2017 but currently generates no meaningful revenue stream.[F1][S1]

Its principal asset is a customer database comprising approximately 31 million members obtained via acquisition of China Enterprise Overseas Investment & Finance Group Limited in 2014.[S11] Despite this sizable intangible asset, the company has yet to successfully monetize it or develop scalable operations.

Financially, Yinfu reported zero revenues for fiscal years ending March 31, 2024 (FY2024) and March 31, 2025 (FY2025), following isolated revenues of $58,395 in FY2023.[F1] Operating losses remain consistent, slightly increasing by approximately 5.5% year-over-year from -$82,877 in FY2024 to -$87,399 in FY2025. Net income turned positive at $29,444 in FY2025 compared to a loss of -$65,461 the prior year, likely reflecting non-operational gains rather than core business improvement.[F1]

Operating cash flow deteriorated further reaching -$72,114 in FY2025 versus -$33,442 previously,[F1] underscoring ongoing cash burn against limited liquidity. Stockholders’ equity remains negative but improved substantially to -$495,016 from over -$2.6 million the prior year.[F1]

Historical performance (annual)

| FY | Rev ($) | Net ($) | CFO ($) | OpInc ($) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 0 | 29444 | -72114 | -87399 | +145.0% | |

| 2024 | 0 | -65461 | -33442 | -82877 | -100.0% | +82.4% |

| 2023 | 58395 | -371084 | -71382 | -371987 | +21.6% | |

| 2022 | 0 | -473220 | -172771 | -472803 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex, Div, Buybacks, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -5.9 |

| 2024 | 2.5 |

| 2023 | 14.2 |

| 2022 | 19.4 |

Source: SEC companyfacts cache [F1].

*Note: Current assets and liabilities data are only available for the most recent fiscal year.[F1]

Business Model Shift and Asset Utilization

Though branded as a gold corporation historically engaged in exploration,[S24] Yinfu ceased mineral exploration activities years ago.[S24] Its current strategy focuses on leveraging subsidiaries established in Hong Kong and China post-2017 acquisitions,[S7] with its key asset being the large customer database linked to domain dahuacheng.com acquired from CEI.[S11]

Despite possessing this asset base potentially valuable for digital marketing or related services within China's internet economy,[S11] Yinfu has not disclosed specific milestones or initiatives aimed at monetizing this database or generating sustainable revenue streams.[F1][S11]

Further complicating growth prospects are regulatory constraints impacting capital flows between offshore parent entities and domestic Chinese subsidiaries due to PRC SAFE Circular No.37 requirements mandating foreign exchange registration for offshore investments by PRC residents.[S1][S26] Non-compliance risks blocking capital injections or profit repatriation exacerbate funding challenges given the company's reliance on cross-border financing.[S1][S26]

Additionally, stringent PRC cybersecurity laws effective since mid-2017,[S16] complemented by the Data Security Law effective September 2021,[S19] impose compliance burdens on companies managing personal data such as Yinfu’s extensive user dataset. Failure to comply could result in penalties or operational restrictions hindering future growth.

Regulatory Landscape and Legal Considerations

Operating principally within China exposes Yinfu to legal uncertainties inherent in evolving PRC regulations affecting foreign-invested enterprises.[S9][S12][S16][S27]

Key risks include:

- Limitations on U.S. regulators’ ability to conduct audit inspections under the Holding Foreign Companies Accountable Act (HFCAA), increasing scrutiny risks due to PCAOB inspection restrictions on auditors based in China/Hong Kong.[S25]

- Cross-border cooperation challenges for investigations between U.S. and PRC authorities may delay or complicate regulatory oversight.[S12][S20]

- Political and economic shifts within China could materially impact operational conditions.[S17][S27]

Currently no pending litigation or threatened legal actions have been disclosed,[S10] but ongoing regulatory developments warrant close attention.

Capital Structure and Shareholder Impact

Yinfu has implemented multiple reverse stock splits — notably a one-for-100 split effective February 2017 and a subsequent five-for-one split approved November 2021 — aimed at consolidating shares to maintain Nasdaq listing standards amidst persistent stock price pressure.[S7]

The company is classified as a penny stock under SEC rules,[S14] limiting broker-dealer participation and trading liquidity.

Capital raising efforts have included a February 2023 private placement issuing 120 million shares raising approximately $120K with an associated one-year lock-up period; proceeds were used primarily for working capital.[S7][S8] Directors and significant stockholders have also supported operations via loans historically.[F1][S7]

No dividends or share repurchases have been declared or executed given constrained cash resources.[F1][S7][S15] Cash balances remain minimal ($560 at end-2022), indicating continued dependence on external funding for survival.[F1]

Workforce and Operational Footprint

As of May 19, 2025, Yinfu employed three individuals including newly appointed President Zhang Hong with a monthly salary of $5K; previously executive roles were consolidated under one individual holding multiple offices.[S15][S21]

The company indicated plans to hire up to approximately twenty employees over the next twelve months contingent upon securing additional capital but provided no firm timelines or budgets.[S11]

There is no evidence of current research and development activity,[S21] suggesting the company operates mainly as an asset-holding entity awaiting strategic clarity.

Returns Metrics and Capital Allocation Summary

With persistent operating losses until recently turning slightly positive net income through non-operational items,[F1] key return metrics remain negative. Approximate return on equity stands near -6% based on latest annual figures reflecting accumulated deficits relative to net income gains.[F1]

Free cash flow remains deeply negative given operating cash outflows far exceed minimal capex levels historically unrelated to current periods; capex data is not available for recent years limiting further analysis.[F1]

Capital deployment focuses almost exclusively on equity financing supporting working capital needs with dilution risk present absent profitable operations or alternative funding sources.

Outlook and Monitoring Points

Growth prospects hinge critically on addressing liquidity constraints while developing concrete plans to monetize its core customer database asset within China's regulatory framework.

Key milestones investors should monitor include:

- Initiation or increase of revenue streams indicating successful asset monetization.

- Additional capital raises extending operational runway.

- Regulatory developments affecting foreign exchange controls impacting subsidiary funding.

- Management disclosures clarifying strategic direction or regulatory interactions.

- Potential mergers or acquisitions subject to complex PRC approval processes that may affect growth trajectory.[S23]

Conclusion

Yinfu Gold Corporation remains highly speculative with significant financial distress compounded by complex regulatory environments governing its Chinese operations. While owning an extensive user database may offer latent value potential, lack of disclosed commercialization initiatives combined with severe liquidity challenges impose substantial execution risk.

Investors should exercise caution and closely track quarterly filings for updates on top-line activation efforts, cash flow improvements, regulatory compliance progress, and management commentary elucidating future business model execution plans.

Disclaimer: This report is based solely on publicly available disclosures as of the dates referenced herein and does not constitute investment advice. Yinfu Gold Corporation presents heightened risks typical among small-cap Chinese entities listed offshore including financial instability and geopolitical-regulatory uncertainties. Professional consultation is strongly advised before making investment decisions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments